Palm Kernel Oil Market Size

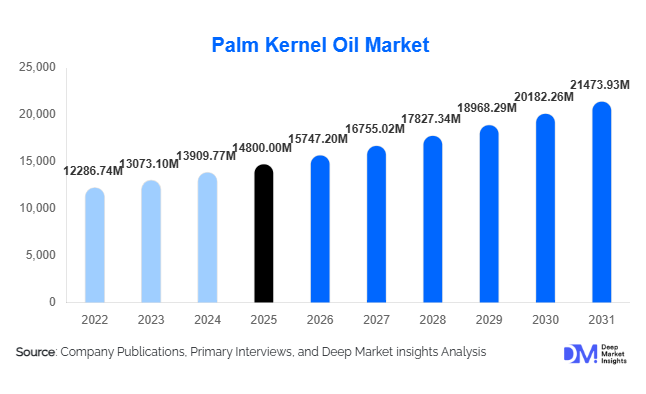

According to Deep Market Insights, the global palm kernel oil market size was valued at USD 14,800 million in 2025 and is projected to grow from USD 15,747.20 million in 2026 to reach USD 21,473.93 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The palm kernel oil market growth is primarily driven by increasing demand across oleochemicals, personal care, and food processing industries, along with rising adoption of bio-based raw materials as alternatives to petrochemicals.

Key Market Insights

- Oleochemical applications dominate demand, driven by the global shift toward renewable and biodegradable chemical feedstocks.

- Asia-Pacific leads both production and consumption, with Indonesia and Malaysia accounting for the majority of the global supply.

- The personal care and cosmetics industry remains a major growth driver, fueled by increasing global hygiene awareness and skincare consumption.

- Europe is witnessing a rising demand for certified sustainable palm kernel oil, supported by strict environmental regulations.

- Emerging economies such as India and African nations are boosting consumption due to urbanization and expanding middle-class populations.

- Technological advancements in refining and fractionation are enabling higher-value derivatives and improved processing efficiency.

What are the latest trends in the palm kernel oil market?

Shift Toward Sustainable and Certified Production

Sustainability has become a defining trend in the palm kernel oil market, with increasing demand for RSPO-certified and traceable products. Governments and multinational corporations are imposing stricter environmental and social standards, pushing producers to adopt sustainable farming practices. This trend is particularly strong in Europe and North America, where buyers are prioritizing ethically sourced inputs. Companies are investing in supply chain transparency, blockchain tracking, and deforestation-free sourcing commitments, reshaping procurement strategies across industries.

Expansion of Oleochemical Applications

The growing adoption of palm kernel oil in oleochemical production is transforming the market landscape. Fatty acids and fatty alcohols derived from PKO are increasingly used in detergents, surfactants, lubricants, and industrial chemicals. This shift is driven by environmental concerns and regulatory pressures to reduce dependence on petroleum-based products. As green chemistry gains traction, PKO is emerging as a critical feedstock, particularly in Asia and Europe, where industrial demand for bio-based materials is accelerating.

What are the key drivers in the palm kernel oil market?

Rising Demand from the Personal Care Industry

The global personal care and cosmetics industry continues to expand steadily, driving strong demand for palm kernel oil. Its high lauric acid content makes it ideal for soap production, skincare formulations, and haircare products. Increasing consumer focus on hygiene and beauty products, particularly in emerging economies, is boosting consumption. The expansion of premium and organic personal care products is further strengthening demand for high-quality refined PKO.

Growth of Bio-Based Oleochemicals

The transition toward sustainable and renewable chemicals is a major growth driver. Palm kernel oil serves as a key raw material for producing fatty alcohols and glycerin, widely used in industrial and consumer applications. With governments promoting green alternatives and industries seeking to reduce carbon footprints, the demand for PKO-derived oleochemicals is rising rapidly, particularly in developed markets.

What are the restraints for the global market?

Environmental and Sustainability Concerns

The palm kernel oil industry faces significant scrutiny due to deforestation, biodiversity loss, and land-use issues associated with palm cultivation. Increasing regulatory pressure and consumer awareness are forcing companies to adopt sustainable practices, which can increase operational costs and limit expansion.

Price Volatility and Supply Chain Risks

Fluctuations in raw material prices, influenced by weather conditions, geopolitical factors, and export restrictions, pose challenges to market stability. Supply disruptions in major producing countries such as Indonesia can lead to pricing volatility, affecting profitability for manufacturers and end users.

What are the key opportunities in the palm kernel oil industry?

Expansion in Emerging Markets

Rapid urbanization and rising disposable incomes in regions such as Africa and South Asia are creating significant growth opportunities. Increasing consumption of processed foods, personal care products, and cleaning agents is driving demand for palm kernel oil. Investments in local refining and processing capacities are further supporting market expansion in these regions.

Advancements in Processing Technologies

Technological innovations in fractionation and refining processes are enabling producers to create high-value derivatives with improved quality and efficiency. These advancements allow companies to enhance product portfolios, improve margins, and cater to specialized industrial applications, particularly in cosmetics and chemicals.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14800 Million |

| Market Size in 2026 | USD 15747.20 Million |

| Market Size in 2031 | USD 21473.93 Million |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Refined palm kernel oil (RPKO) dominates the global market, accounting for approximately 42% of the total market share in 2025. This leadership position is primarily driven by its superior stability, neutral odor, and extended shelf life, making it highly suitable for large-scale applications in food processing and personal care formulations. Manufacturers prefer RPKO due to its consistent quality, which is critical for standardized industrial production, especially in confectionery fats, bakery shortenings, and soap manufacturing. Additionally, the growing demand for processed and packaged foods in emerging economies has further strengthened RPKO consumption globally.

Fractionated palm kernel oil is gaining strong momentum as a high-value segment, particularly due to its specialized applications in premium confectionery fats, cocoa butter substitutes, and industrial formulations. The ability to separate olein and stearin fractions enables manufacturers to tailor product functionality, which is driving adoption in both the food and oleochemical industries. Meanwhile, hydrogenated palm kernel oil, although a smaller segment, continues to serve niche applications requiring enhanced oxidative stability and longer shelf life, particularly in industrial and bakery applications where durability is essential.

Application Insights

The oleochemicals segment leads the palm kernel oil market with an estimated 38% share in 2025, making it the most dominant application area. This leadership is largely attributed to the global transition toward bio-based and sustainable chemicals, where palm kernel oil serves as a key feedstock for fatty acids, fatty alcohols, and glycerin. Increasing regulatory pressure to reduce carbon emissions and dependence on petrochemicals has significantly accelerated demand in this segment, particularly across Europe and Asia.

The food and beverage segment remains a strong contributor, supported by rising consumption of confectionery products, baked goods, and processed foods. Palm kernel oil is valued for its functional properties, such as texture enhancement and oxidation resistance. Meanwhile, the personal care and cosmetics segment is witnessing consistent growth, driven by increasing demand for soaps, detergents, and skincare products. The multifunctional properties of PKO, including its foaming and moisturizing characteristics, continue to make it indispensable in this segment, particularly in emerging markets with rising hygiene awareness.

Distribution Channel Insights

Direct B2B sales dominate the distribution landscape, accounting for nearly 70% of the global market in 2025. This dominance is primarily driven by the bulk nature of palm kernel oil transactions and the preference of large industrial buyers for long-term supply agreements. Such contracts ensure price stability, consistent quality, and secure supply chains, which are critical for industries such as oleochemicals and food processing.

Distributors and traders play a significant but secondary role, particularly in fragmented and regional markets where smaller manufacturers rely on intermediaries for sourcing. These channels are crucial in bridging supply-demand gaps in regions with limited direct producer access. Additionally, online bulk commodity platforms are emerging as a niche yet growing channel, offering transparency in pricing and facilitating global trade. Digitalization of commodity trading is expected to gradually enhance efficiency and accessibility in the distribution ecosystem.

End-Use Industry Insights

The cosmetics and personal care industry holds the largest share in the palm kernel oil market, contributing approximately 34% of the total demand in 2025. This dominance is driven by the widespread use of PKO in soap manufacturing, skincare formulations, and haircare products. Increasing global awareness of hygiene, coupled with rising disposable incomes in developing regions, continues to fuel growth in this segment. The expansion of premium and organic personal care products is further strengthening demand for high-quality refined palm kernel oil.

The oleochemical industry is the fastest-growing end-use segment, supported by strong demand for renewable chemical feedstocks across industrial applications. This growth is closely linked to sustainability trends and regulatory mandates promoting bio-based alternatives. The food processing industry also remains a key contributor, particularly in bakery and confectionery applications. Emerging uses in biofuels, industrial lubricants, and specialty chemicals are opening new growth avenues, diversifying the end-use landscape and enhancing long-term market potential.

Explore more data points, trends and opportunities Download Free Sample Report

Palm Kernel Oil Market Segmentations

By Product Type

- Crude Palm Kernel Oil (CPKO)

- Refined Palm Kernel Oil (RPKO)

- Fractionated Palm Kernel Oil

- Hydrogenated Palm Kernel Oil

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Oleochemicals

- Industrial Applications

By Distribution Channel

- Direct/B2B Sales

- Distributors & Traders

- Online Bulk Commodity Platforms

By End-Use Industry

- Food Processing Industry

- Cosmetics & Personal Care Industry

- Oleochemical Industry

- Pharmaceutical Industry

- Energy & Biofuel Industry

Regional Insights

Asia-Pacific

Asia-Pacific dominates the palm kernel oil market, accounting for approximately 58% of the global market share in 2025. Indonesia and Malaysia remain the backbone of global supply, supported by favorable tropical climates, large-scale plantations, and well-established processing infrastructure. The region’s leadership is further strengthened by government support for downstream processing and export-oriented policies. On the demand side, China and India are major consumption hubs, driven by expanding food processing industries, rising demand for personal care products, and increasing industrial use of oleochemicals. Rapid urbanization, population growth, and cost advantages in production continue to drive regional dominance.

Europe

Europe holds approximately 18% of the global market share, with key countries including Germany, the Netherlands, and France. The region’s growth is primarily driven by stringent environmental regulations and a strong shift toward sustainable sourcing. European industries are increasingly adopting RSPO-certified palm kernel oil to meet regulatory and consumer expectations. Additionally, the region’s advanced chemical and personal care industries are driving demand for high-quality oleochemical derivatives. The emphasis on green chemistry and circular economy practices further accelerates market growth in Europe.

North America

North America accounts for around 10% of the global market, with the United States as the primary consumer. Growth in this region is driven by increasing adoption of bio-based chemicals and strong demand from the food and personal care sectors. The presence of established consumer goods manufacturers and a growing preference for sustainable ingredients are key drivers. Additionally, regulatory support for renewable products and rising investments in green chemistry are contributing to steady market expansion.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, supported by rising urbanization, population expansion, and increasing industrialization. Countries such as Nigeria and South Africa are key markets, with growing investments in palm oil refining and processing infrastructure. The region’s growth is also driven by increasing demand for affordable edible oils and personal care products. Additionally, efforts to develop local palm cultivation and reduce import dependency are contributing to long-term market potential.

Latin America

Latin America, led by Brazil and Colombia, is both a producer and consumer of palm kernel oil and represents one of the fastest-growing regions, with a CAGR exceeding 7%. Growth in this region is driven by expanding agricultural activities, favorable government policies supporting palm cultivation, and increasing industrial demand for oleochemicals. Rising domestic consumption of processed foods and personal care products is also contributing to market expansion. Furthermore, investments in sustainable palm production and export capabilities are positioning Latin America as an emerging global supplier.

Key Players in the Palm Kernel Oil Market

- Wilmar International

- Golden Agri-Resources

- Sime Darby Plantation

- Musim Mas Group

- IOI Corporation

- Kuala Lumpur Kepong Berhad

- Cargill Incorporated

- Astra Agro Lestari

- Apical Group

- Olam International

- PT Smart Tbk

- Bunge Limited

- Fuji Oil Holdings

- Godrej Agrovet

- AAK AB