Paintless Dent Repair Service Market Size

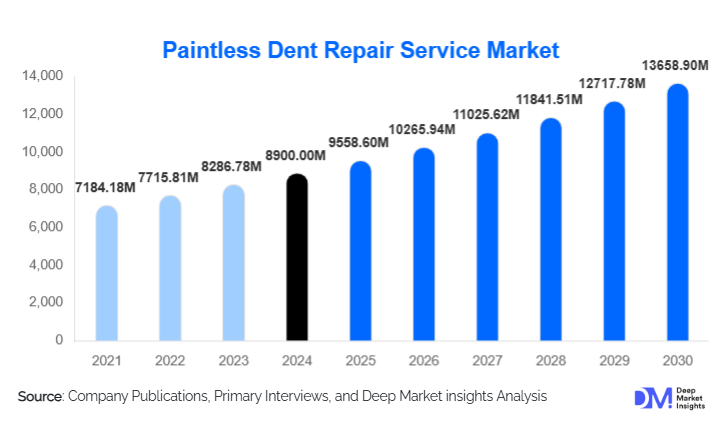

According to Deep Market Insights, the global paintless dent repair (PDR) service market size was valued at USD 8,900 million in 2025 and is projected to grow from USD 9,558.60 million in 2026 to reach USD 13,658.90 million by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). Market growth is primarily driven by the rising frequency of automotive hail damage, insurance-backed dent repair services, expansion of mobile PDR franchise networks, and increased usage of AI-powered dent detection tools for precision and cost-efficiency.

Key Market Insights

- Hail damage repair is the leading revenue-generating segment, supported by increasing climate change-driven hail events in North America, Europe, and Australia.

- AI-integrated dent detection and automated estimation are revolutionizing PDR operations, enhancing accuracy and enabling digital insurance partnerships.

- Passenger cars dominate PDR service demand, particularly in urban markets and high-density vehicle ownership regions.

- Insurance-linked repair networks are expanding rapidly, accounting for nearly one-third of total PDR service revenues.

- Asia-Pacific is the fastest-growing regional market, driven by rising vehicle sales, increasing insurance penetration, and expanding fleet leasing sectors.

- Mobile and on-demand PDR franchises are transforming service accessibility, attracting both individual car owners and corporate fleets.

Paintless Dent Repair Service Market Trends

AI-Powered Dent Detection and Repair Automation

Artificial intelligence is transforming PDR services by enabling high-precision dent detection, automated repair cost estimation, digital damage classification, and real-time repair feasibility analysis. AI-driven imaging platforms can analyze vehicle surface contours and detect dents as small as 1–2 mm with high accuracy, significantly reducing manual inspection errors. These platforms integrate with AI-estimation software to suggest repair methods based on dent size, depth, metal elasticity, and paint condition. Real-time diagnostics, coupled with mobile app integration, allow customers to upload images for instant repair cost estimation, reducing service turnaround time by 30–40%. Additionally, cloud-based systems support automatic claim submission to insurers, helping expedite insurance approvals. The technology is being actively deployed in key markets such as the U.S., Germany, Japan, UAE, and South Korea to enhance service efficiency and profitability.

Rise of Mobile and Franchise-Based PDR Service Models

Mobile PDR services are increasingly being adopted in urban locations due to customer demand for convenience, lower service center dependency, and reduced operational costs. Equipped with portable dent removal tools, technicians can perform repairs at homes, offices, car dealerships, and fleet parking facilities. This trend has accelerated in commercial fleet management, where logistics, rental, and leasing companies prefer on-site service to reduce downtime. Franchise-based PDR businesses are gaining momentum, offering standardized service protocols, centralized customer support, certified technician training, and nationwide insurance partnerships. North America, Europe, and Australia are witnessing rapid franchise expansion due to favorable regulations, high automotive density, and rising independent technician conversions into branded franchise operators.

Paintless Dent Repair Service Market Drivers

Growing Insurance Partnerships and Claim-Based Repairs

Insurance providers are increasingly adopting PDR as a preferred dent repair method due to lower costs, faster claim processing, and vehicle value preservation. Conventional body shop repairs often require repainting and part replacements, whereas PDR restores dents without altering factory paint, reducing average claim costs by 50–65%. In countries like the U.S., Germany, and Canada, up to 70% of hail-related automotive insurance claims are repaired through PDR-certified centers. Insurance firms are establishing exclusive repair contracts with PDR service networks, further boosting market penetration and service standardization.

Increasing Demand from EVs and Premium Automotive Segments

PDR is increasingly used for luxury vehicles and electric cars due to its ability to retain original paint, preserve vehicle resale value, and prevent warranty breaches. Premium automotive brands such as Tesla, BMW, Mercedes-Benz, Audi, and Lexus prioritize PDR-compatible repair methods because repainting or panel replacement can disrupt factory paint alignment and sensor calibrations. The rising share of electric and premium vehicles globally is creating specialized demand for high-precision, non-invasive dent removal using advanced PDR tools and technician certification programs.

Paintless Dent Repair Service Market Restraints

Shortage of Certified Technicians

PDR is a skill-intensive profession requiring manual dexterity, specialized training, and tool handling expertise. Emerging markets such as India, Brazil, and Malaysia lack sufficient certified technicians, affecting service quality and scalability. Training costs for advanced techniques such as glue-pull repair, body crease correction, and aluminum panel restoration are high, discouraging new entrants. The shortage of qualified PDR professionals especially impacts large-scale corporate repair networks and insurance-linked partnerships.

Limited Repair Scope for Structural and Deep Paint-Damaged Dents

PDR is effective only for non-paint-damaged, shallow, and surface-level dents caused by hail, door impact, and minor collisions. It is not suitable for deep dents, cracked paint, metal stretching, or structural body damage, limiting its applicability to approximately 60% of dent cases. Severe crash repairs still require conventional bodywork, welding, repainting, or panel replacement, which restricts full market conversion toward PDR-only repair solutions.

Paintless Dent Repair Service Market Opportunities

AI and IoT-Integrated Smart Repair Platforms

The integration of AI-based dent imaging, IoT-enabled inspection tools, and smart repair management platforms presents major business expansion opportunities. These technologies assist in autoscanning vehicle panels, identifying dent severity, predicting repair duration, tracking technician performance, and generating automated quotations. IoT-enabled PDR tools can digitally monitor pressure, rod angles, and force applied during repairs, helping technicians maintain consistency and precision. These platforms also support remote diagnostics, making them suitable for fleet operators, rental services, and insurance contract repairs.

Climate Change-Driven Hail Damage Restoration Services

Increasing frequency of hailstorms, windstorms, and weather-related vehicle damage is significantly boosting PDR demand across the U.S., Australia, Germany, France, and Japan. Severe hailstorms can damage hundreds of vehicles in a single region, creating bulk repair demand from insurance companies and fleet owners. PDR is widely adopted in hail-affected zones due to its ability to repair multiple dents without repainting or replacing panels. Service providers specializing in mass hail restoration projects are establishing partnerships with insurance firms and corporate fleets, creating high-revenue opportunities from weather-driven repair contracts.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8900 Million |

| Market Size in 2026 | USD 9558.60 Million |

| Market Size in 2031 | USD 13658.90 Million |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

Hail damage repair services lead the market with a 36% share due to large-scale repair demand driven by climate-related weather events. Insurance-supported hail restoration projects allow PDR specialists to handle hundreds of vehicles simultaneously, making this segment the most commercially profitable. The growth is further supported by rapid claim approvals, automated dent detection, and bulk repair contracts with rental, corporate, and dealership fleets.

Technology Insights

LED reflection systems and AI-backed dent mapping tools hold a 28% share, making them the leading technology segment due to their ability to precisely detect dent locations, monitor repair progress, and improve technician accuracy. These tools help reduce manual guesswork, support remote estimates for insurance claims, and enable consistent repair quality for EVs, luxury vehicles, and metallic surfaces.

Vehicle Type Insights

Passenger cars account for 53% of total PDR demand, primarily due to accelerating urban vehicle ownership, frequent parking-related dents, and the high importance of visual aesthetics for resale value. Passenger car owners often prefer PDR due to its lower cost, no-paint recovery, and same-day service capabilities, making it the dominant vehicle segment.

Business Model Insights

Insurance-linked repair networks hold 32% market share, making them the dominant business model. These networks provide assured repair volumes from insurance companies, faster claim processing, pre-negotiated contracts, and stable revenue for PDR providers. This model is especially prevalent in North America, Australia, Western Europe, and select markets in the Asia-Pacific.

End-User Insights

Individual vehicle owners account for 41% of total demand due to regular car maintenance, resale value preservation, and rising interest in cosmetic repair services. Corporate fleets, leasing companies, and insurance partners follow closely, with fleet-based demand expected to grow at 8.5% CAGR due to increasing adoption of on-site mobile PDR services.

Explore more data points, trends and opportunities Download Free Sample Report

Paintless Dent Repair Service Market Segmentations

By Service Type

- Hail Damage Repair Services

- Minor Dent & Ding Repair

- Large Dent & Body Crease Repair

- Paint Protection & PDR Combo Services

- Mobile / On-site PDR Services

By Vehicle Type

- Passenger Cars (Sedans, SUVs, Hatchbacks)

- Light Commercial Vehicles (Vans, Pickups)

- Heavy-Duty Vehicles (Buses, Trucks)

- Electric Vehicles (BEVs, PHEVs)

- Luxury & Classic Vehicles

By Business Model

- Independent PDR Service Centers

- OEM-Authorized Repair Centers

- Insurance-Linked Repair Networks

- Mobile PDR Service Providers

- Franchise-Based PDR Networks

By End User

- Individual Vehicle Owners

- Insurance Companies

- Car Dealerships & Showrooms

- Fleet Owners (Leasing, Taxi, Logistics)

- Auto Body Workshops & Service Chains

By Technology

- LED Lighting & Reflection Board Systems

- Glue-Pulling Systems

- PDR Rods & Lever Tool Systems

- Heat-Assisted PDR Techniques

- AI-Based Dent Detection & Estimation Software

Regional Insights

North America

North America leads the market with a 34% share in 2025, driven by high vehicle ownership rates, frequent hailstorms in Texas, Colorado, Oklahoma, and Alberta, and enhanced insurance penetration. The U.S. alone accounts for 28% of global market demand, supported by well-established franchise networks, advanced repair facilities, and significant AI and digital claim processing adoption. The region is a major hub for insurance-linked PDR operations and corporate fleet maintenance programs.

Europe

Europe holds 26% market share, with Germany, the U.K., and France as primary contributors. Germany leads due to high automotive density, EV adoption rates, and strong OEM collaboration for dent repair protocols. The European market is characterized by advanced AI dent estimation systems, strict repair quality standards, and growing demand from fleet leasing and luxury vehicle owners.

Asia-Pacific

Asia-Pacific is the fastest-growing region at 9.1% CAGR, fueled by expanding automotive sales in China and India, rising insurance adoption, and the growth of dealership-integrated PDR service networks. Japan and South Korea contribute through advanced EV manufacturing ecosystems and specialized repair-certified centers. The region is also witnessing rapid franchise and mobile PDR deployment in urban centers.

Latin America

Latin America shows emerging growth, led by Brazil and Mexico, where rising insurance coverage, growing vehicle leasing operations, and increasing import of PDR tools are supporting market expansion. Economic recovery and fleet mobility services are driving service adoption.

Middle East & Africa

MEA displays strong demand in the UAE, Saudi Arabia, and South Africa, largely driven by luxury car ownership, high-end vehicle rentals, and on-site mobile repair services. Car rental operators, dealerships, and premium service centers are major demand contributors, especially in urban hubs like Dubai, Riyadh, and Johannesburg.

Key Players in the Paintless Dent Repair Service Market

- Dent Wizard

- Caliber Collision

- Service King

- PDR Nation

- Ding King Training Institute

- Fix Auto

- Hail Experts

- Dent Concepts

- Rapid Hail Repair

- Elite Dent Removal

- Mobile Dent Repair Co.

- DentMagic

- LTT PDR Tools

- Dentco

- Hail Specialists Inc.

Recent Developments

- In February 2025, Dent Wizard expanded its AI-based dent detection platform to support automated insurance claim processing for hail damage repairs across North America.

- In April 2025, Service King introduced mobile PDR repair vans with integrated advanced tooling systems for rapid fleet servicing in urban areas.

- In May 2025, Caliber Collision formed a strategic partnership with Tesla-approved repair networks to provide specialized paintless EV dent repair services.