Oven Market Size

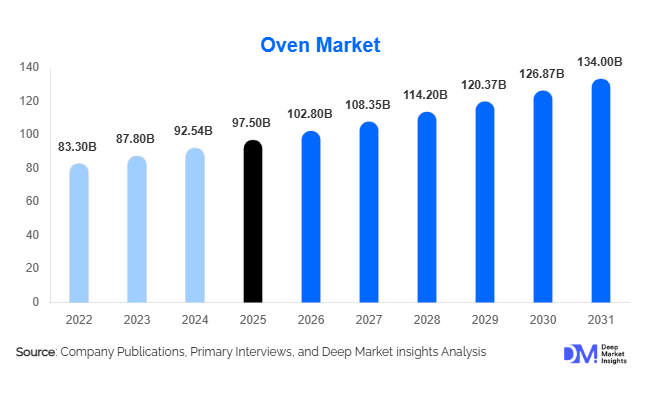

According to Deep Market Insights, the global oven market size was valued at USD 97.5 billion in 2025 and is projected to grow from USD 102.8 billion in 2026 to reach USD 134 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The oven market growth is primarily driven by rising demand for convenience foods, expansion of commercial foodservice establishments, and increasing adoption of energy-efficient and smart cooking appliances. Rapid urbanization, evolving dietary habits, and the proliferation of quick-service restaurants (QSRs) and cloud kitchens are further accelerating market expansion across both developed and emerging economies.

Key Market Insights

- Electric ovens dominate the market, accounting for nearly 58% share due to energy efficiency and compatibility with smart technologies.

- The residential segment leads demand, contributing approximately 46% of the global market in 2025.

- Asia-Pacific is the largest regional market, holding around 38% share, driven by China and India.

- Smart ovens are the fastest-growing segment, with increasing adoption in developed markets and urban households.

- Commercial foodservice expansion, particularly QSRs and bakery chains, is driving high demand for advanced ovens.

- E-commerce channels are rapidly growing, reshaping distribution dynamics for residential ovens.

What are the latest trends in the oven market?

Smart and Connected Cooking Appliances

The integration of IoT and AI technologies is transforming the oven market. Smart ovens equipped with remote control, automated cooking presets, and voice assistant compatibility are gaining popularity among tech-savvy consumers. These appliances enable users to monitor and control cooking processes via mobile applications, enhancing convenience and precision. Manufacturers are increasingly focusing on connectivity features that integrate ovens into broader smart home ecosystems. This trend is particularly strong in North America and Europe, where consumers are willing to pay a premium for advanced functionalities. Additionally, AI-based cooking recommendations and energy optimization features are further enhancing product differentiation.

Shift Toward Energy-Efficient and Sustainable Ovens

Sustainability has become a key focus area, with manufacturers developing ovens that consume less energy and reduce carbon emissions. Regulatory frameworks in Europe and North America are pushing for stricter energy efficiency standards, encouraging innovation in eco-friendly designs. Features such as improved insulation, heat recovery systems, and low-energy electric heating elements are being incorporated into modern ovens. Consumers are also showing a growing preference for sustainable appliances, influencing purchasing decisions. This trend is expected to drive replacement demand in mature markets while shaping product development strategies globally.

What are the key drivers in the oven market?

Rising Demand for Convenience and Processed Foods

The increasing consumption of ready-to-eat meals, frozen foods, and bakery products is a major driver of the oven market growth. Urban lifestyles and busy work schedules are encouraging consumers to opt for convenient food options that require minimal preparation. This trend is particularly prominent in emerging economies, where Western dietary habits are gaining traction. Industrial food processing units are also expanding their capacity, driving demand for high-performance ovens in large-scale production environments.

Expansion of the Commercial Foodservice Industry

The rapid growth of restaurants, QSR chains, and cloud kitchens is significantly boosting demand for commercial ovens. These establishments require reliable and efficient cooking equipment to handle high volumes and ensure consistent food quality. The increasing penetration of global food chains into emerging markets is further accelerating this trend. Commercial ovens, particularly convection and combi ovens, are witnessing strong adoption due to their versatility and efficiency.

What are the restraints for the global market?

High Initial Cost of Advanced Ovens

Advanced ovens, especially smart and industrial-grade models, involve high upfront costs. This can limit adoption among small businesses and price-sensitive consumers, particularly in developing regions. The cost factor also affects replacement cycles, as users may delay upgrading to newer models despite technological benefits.

Volatility in Raw Material Prices

Fluctuations in the prices of key raw materials such as stainless steel and aluminum can impact manufacturing costs and profit margins. This creates pricing challenges for manufacturers and may lead to increased product prices, affecting demand in competitive markets.

What are the key opportunities in the oven industry?

Growth of Smart Kitchen Ecosystems

The increasing adoption of smart homes presents a significant opportunity for oven manufacturers. Integrating ovens with smart kitchen ecosystems allows for enhanced user experiences and opens avenues for premium product offerings. Companies investing in IoT-enabled appliances and AI-driven cooking solutions can gain a competitive edge and capture high-value customer segments.

Emerging Market Expansion

Rapid urbanization and rising disposable incomes in regions such as Asia-Pacific, Latin America, and Africa are creating strong demand for ovens. The expansion of the middle class and changing food consumption patterns are driving residential and commercial adoption. Manufacturers can tap into these markets by offering affordable and durable products tailored to local needs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 97.5 Billion |

| Market Size in 2026 | USD 102.8 Billion |

| Market Size in 2031 | USD 134 Billion |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Microwave ovens continue to lead the product segment, accounting for approximately 32% of the global market in 2025. This dominance is primarily driven by their affordability, compact footprint, and multifunctionality, making them highly suitable for urban households with space constraints. Increasing demand for quick meal preparation and reheating solutions has further strengthened adoption, particularly among working professionals and nuclear families. Additionally, continuous product innovation, such as inverter technology, grill-microwave combinations, and smart connectivity, has enhanced their utility beyond basic heating functions.

Convection and combination ovens are emerging as high-growth segments, particularly in commercial kitchens and premium residential applications. Their ability to provide uniform heat distribution, faster cooking times, and multi-mode functionality (baking, roasting, steaming) makes them ideal for bakery chains, QSRs, and gourmet cooking. Meanwhile, industrial ovens, including conveyor and batch ovens, are witnessing steady demand growth due to increasing automation in food processing and manufacturing industries. Rising production volumes in packaged foods, along with the need for consistency and scalability, are key drivers for industrial oven adoption globally.

Application Insights

The residential segment dominates oven applications, supported by rising household penetration, increasing disposable incomes, and changing cooking habits favoring convenience and experimentation. Growth in urban housing, especially in emerging markets, has significantly boosted demand for compact and multifunctional ovens. Additionally, the growing influence of digital cooking content and home baking trends has further accelerated adoption.

The commercial segment is witnessing the fastest expansion, driven by the rapid growth of restaurants, hotels, bakery chains, and cloud kitchens. Increasing consumer preference for dining out and online food delivery has led to higher demand for efficient, high-capacity ovens capable of maintaining consistency and speed. Industrial applications are also gaining momentum across the food processing, automotive, and electronics industries. These sectors require precision-controlled heating systems for large-scale production and specialized processes, thereby expanding the application scope of ovens beyond traditional cooking uses. This diversification is strengthening overall market resilience and reducing dependency on any single end-use segment.

Distribution Channel Insights

Retail stores and e-commerce platforms collectively account for over 55% of global oven sales, with e-commerce emerging as the fastest-growing distribution channel. The rapid growth of online platforms is driven by increasing internet penetration, the availability of product comparisons, competitive pricing, and the convenience of doorstep delivery. Consumers are increasingly relying on online reviews, digital demonstrations, and influencer recommendations to make purchasing decisions.

Direct sales channels remain highly significant in the commercial and industrial segments, where bulk procurement, long-term contracts, and customized solutions are required. Manufacturers often engage directly with foodservice operators and industrial clients to provide tailored products and after-sales services. Additionally, specialty kitchen equipment dealers play a crucial role in catering to professional users such as chefs and bakery operators, offering expert guidance and premium product portfolios. The evolving omnichannel strategy is enabling manufacturers to reach diverse customer segments effectively.

End-Use Insights

The residential segment remains the largest end-use category, with a market size exceeding USD 44,000 million in 2025. This dominance is driven by increasing household adoption, rising middle-class populations, and growing preference for convenient and time-saving cooking appliances. However, the commercial foodservice segment is the fastest-growing, expanding at a CAGR of over 6.5%, fueled by the rapid proliferation of QSRs, cafes, and bakery chains globally.

Industrial food processing represents another critical growth area, supported by increasing global demand for packaged, frozen, and ready-to-eat foods. Large-scale manufacturers are investing in advanced ovens to improve efficiency, consistency, and production capacity. Furthermore, emerging applications in non-food industries such as electronics, automotive, and pharmaceuticals are contributing to demand for specialized industrial ovens. Export-driven manufacturing hubs, particularly in China and Germany, are also generating strong demand for industrial ovens, as these countries continue to dominate global production and supply chains.

Explore more data points, trends and opportunities Download Free Sample Report

Oven Market Segmentations

By Product Type

- Conventional Ovens

- Convection Ovens

- Microwave Ovens

- Steam Ovens

- Combination Ovens

- Industrial Batch Ovens

- Conveyor Ovens

By Application

- Residential Cooking

- Commercial Foodservice

- Industrial Food Processing

- Non-Food Industrial Applications

By Distribution Channel

- Online Retail / E-commerce

- Retail Stores

- Direct Sales (B2B)

- Specialty Kitchen Equipment Dealers

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global oven market, accounting for approximately 38% share in 2025. China leads the region due to its extensive manufacturing base, strong export capabilities, and large consumer market. India is the fastest-growing country, with a CAGR exceeding 7%, driven by rapid urbanization, rising disposable incomes, and increasing adoption of modern kitchen appliances. Additionally, the expansion of QSR chains and food delivery platforms is significantly boosting commercial oven demand. Japan and South Korea contribute through high adoption of technologically advanced and premium appliances, supported by strong consumer purchasing power and innovation-driven markets.

North America

North America holds around 26% of the global market share, with the United States accounting for nearly 80% of the regional demand. The region is characterized by high penetration of advanced kitchen appliances and strong replacement demand. Consumers in this region are early adopters of smart ovens integrated with IoT and AI technologies. Key growth drivers include: strong demand for premium and smart appliances, a well-established foodservice industry, high disposable incomes, and frequent product upgrades driven by technological advancements.

Europe

Europe accounts for approximately 22% of the global oven market, led by countries such as Germany, France, and the UK. The region is highly regulated, with strict energy efficiency and environmental standards shaping product innovation. Consumers exhibit a strong preference for sustainable, energy-efficient, and premium appliances. Key growth drivers include: stringent energy regulations, high adoption of eco-friendly appliances, strong demand for built-in kitchen solutions, and well-developed commercial foodservice infrastructure.

Latin America

Latin America represents around 7% of the global market, with Brazil and Mexico as the primary contributors. The region is witnessing gradual growth supported by increasing urbanization and expansion of the foodservice sector. Key growth drivers include: rising middle-class population, growing restaurant and bakery industry, increasing adoption of modern cooking appliances, and improving retail and e-commerce penetration.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the global market, with growth concentrated in GCC countries such as the UAE and Saudi Arabia. The region is benefiting from increasing investments in hospitality and tourism infrastructure. Key growth drivers include: expansion of the hospitality sector, rising tourism, increasing disposable incomes, and growing demand for premium kitchen appliances in urban centers. Additionally, government-led infrastructure development projects are supporting commercial oven demand across hotels and restaurants.

Key Players in the Oven Market

- Whirlpool Corporation

- Electrolux AB

- Samsung Electronics

- LG Electronics

- BSH Hausgeräte (Bosch)

- Panasonic Corporation

- Sharp Corporation

- Haier Group

- Midea Group

- Middleby Corporation

- Rational AG

- Alto-Shaam Inc.

- Turbochef Technologies

- ITW Food Equipment Group

- GEA Group