Organic Apparel Market Size

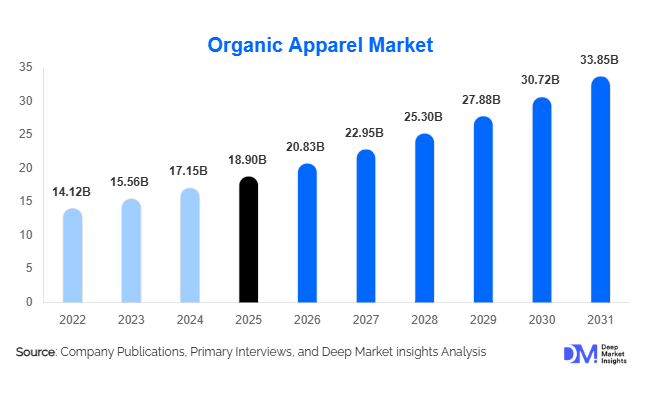

According to Deep Market Insights, the global organic apparel market size was valued at USD 18.9 billion in 2025 and is projected to grow from USD 20.83 billion in 2026 to reach USD 33.85 billion by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). The organic apparel market growth is primarily driven by increasing consumer awareness regarding sustainable fashion, rising adoption of eco-friendly textiles, and growing demand for ethically sourced clothing products across premium and mainstream retail channels.

Key Market Insights

- Organic cotton continues to dominate the market, accounting for the majority of raw material consumption due to its lower environmental impact and established supply chain ecosystem.

- Online retail and direct-to-consumer channels are rapidly transforming the industry, enabling sustainable brands to expand globally with transparent product traceability and certification visibility.

- North America leads the global organic apparel market, supported by high consumer awareness, premium spending behavior, and strong adoption of sustainable fashion trends.

- Asia-Pacific is the fastest-growing regional market, driven by rising organic textile manufacturing capacity in India, China, Bangladesh, and Vietnam.

- Women’s apparel remains the leading consumer category, fueled by higher spending on sustainable fashion, athleisure, and wellness-oriented clothing products.

- Technological advancements in sustainable textile production, including low-water dyeing, blockchain traceability, and bio-based fabrics, are improving operational efficiency and brand competitiveness.

What are the latest trends in the organic apparel market?

Rise of Circular and Regenerative Fashion

The organic apparel industry is increasingly shifting toward circular fashion models and regenerative textile ecosystems. Fashion brands are adopting closed-loop manufacturing systems, biodegradable fabrics, garment recycling programs, and resale platforms to reduce textile waste and improve sustainability performance. Regenerative organic cotton farming practices are gaining traction due to their ability to restore soil health, improve biodiversity, and reduce carbon emissions. Several global apparel companies are investing in regenerative agriculture partnerships to secure long-term, sustainable raw material supply while meeting ESG targets and environmental compliance requirements.

Technology-Enabled Supply Chain Transparency

Technology adoption is reshaping the organic apparel industry through improved supply chain transparency and traceability solutions. Blockchain-enabled textile tracking systems, QR-code product verification, and AI-powered inventory optimization are becoming increasingly common among sustainable fashion brands. Consumers are demanding greater visibility regarding sourcing, manufacturing, labor practices, and environmental impact before making purchasing decisions. Digital product passports and sustainability scoring systems are also helping brands differentiate themselves in highly competitive retail markets. These innovations are particularly appealing to younger consumers seeking transparency, authenticity, and ethical accountability from apparel companies.

What are the key drivers in the organic apparel market?

Growing Consumer Awareness Toward Sustainable Fashion

Rising environmental awareness and growing concern regarding textile industry pollution are major drivers supporting the organic apparel market growth. Consumers are increasingly avoiding chemically treated fabrics and fast-fashion products associated with excessive water consumption, pesticide usage, and carbon emissions. Organic apparel products manufactured using sustainable farming methods and certified ethical supply chains are gaining strong acceptance across developed economies. Millennials and Gen Z consumers, in particular, are prioritizing eco-conscious purchasing behavior and supporting brands with strong sustainability credentials.

Expansion of Organic Textile Manufacturing Infrastructure

Global investments in sustainable textile manufacturing facilities and organic cotton farming are accelerating market expansion. Countries such as India, Bangladesh, Vietnam, and Turkey are strengthening organic textile production capabilities to support rising export demand from Europe and North America. Advancements in eco-friendly dyeing technologies, renewable energy-powered textile factories, and water recycling systems are improving scalability and cost efficiency within the industry. Large fashion retailers are also increasing long-term procurement agreements with certified organic textile suppliers to meet sustainability commitments.

What are the restraints for the global market?

High Production and Certification Costs

Organic apparel production remains more expensive than conventional textile manufacturing due to lower agricultural yields, higher labor requirements, and certification compliance costs. Certifications such as GOTS, OEKO-TEX, and Fair Trade require continuous monitoring and operational investments, increasing production expenses for manufacturers. These cost pressures result in premium product pricing, limiting adoption among price-sensitive consumers and restricting market penetration in developing economies.

Limited Availability of Certified Organic Raw Materials

The global supply of certified organic cotton and sustainable textile fibers remains limited compared to conventional raw materials. Supply chain fragmentation, fluctuating agricultural output, and climate-related disruptions contribute to raw material price volatility and sourcing challenges. Maintaining traceability and certification compliance across international supply chains also creates operational complexities for apparel brands seeking rapid expansion in global markets.

What are the key opportunities in the organic apparel industry?

Growth of Organic Activewear and Wellness Apparel

The rising global focus on health, wellness, and fitness is creating significant opportunities for organic activewear and athleisure brands. Consumers increasingly prefer breathable, skin-friendly, and chemical-free fabrics for yoga, gym wear, and lifestyle apparel. Organic cotton and bamboo-based activewear products are witnessing strong demand among health-conscious urban consumers. Premium sportswear brands integrating sustainability with high-performance fabrics are expected to gain substantial market share during the forecast period.

Expansion of Corporate and Institutional Sustainable Procurement

Corporate sustainability initiatives and ESG-focused procurement policies are generating new opportunities for organic apparel manufacturers. Businesses across hospitality, healthcare, education, and corporate sectors are increasingly adopting sustainable uniforms and ethically sourced textile products. Governments and institutions are also implementing green procurement frameworks, encouraging the use of environmentally responsible apparel products. This trend is expected to create long-term demand for certified organic workwear, hospitality clothing, and institutional uniforms globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.9 Billion |

| Market Size in 2026 | USD 20.83 Billion |

| Market Size in 2031 | USD 33.85 Billion |

| CAGR | 10.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

T-shirts and tops represent the leading product category within the organic apparel market, accounting for a significant share of global revenue due to high replacement frequency and widespread casualwear adoption. Organic casual T-shirts are increasingly preferred by younger consumers seeking sustainable everyday clothing options. Activewear and athleisure apparel are emerging as some of the fastest-growing product categories, driven by rising fitness participation and demand for wellness-oriented clothing. Organic dresses, outerwear, and children’s apparel are also witnessing robust growth as premium fashion brands expand sustainable product portfolios across multiple lifestyle categories.

Material Type Insights

Organic cotton dominates the market with the largest share of global revenue due to its scalability, softness, durability, and widespread acceptance across fashion and lifestyle applications. Hemp-based fabrics are gaining traction due to their low water consumption and durability advantages, particularly in premium sustainable fashion collections. Bamboo-based organic textiles are expanding rapidly within activewear and wellness apparel segments because of their antimicrobial and moisture-wicking properties. Recycled organic blends and plant-based bio-fabric materials are also attracting investment as brands seek next-generation sustainable textile solutions with improved environmental performance.

Distribution Channel Insights

Online retail channels dominate the organic apparel market as consumers increasingly prefer digital platforms offering transparent sustainability information, product traceability, and direct brand engagement. Brand-owned e-commerce platforms and online marketplaces are expanding rapidly due to increasing global internet penetration and digital shopping behavior. Direct-to-consumer sustainable fashion brands are leveraging social media, influencer marketing, and AI-driven personalization to accelerate customer acquisition. Offline retail remains important within premium sustainable fashion stores and department stores, particularly in North America and Europe, where eco-conscious consumer segments are highly developed.

Consumer Category Insights

Women’s organic apparel remains the dominant consumer segment, accounting for the largest market share due to higher engagement with sustainable fashion trends and premium apparel spending. Female consumers are driving strong demand for eco-friendly athleisure, maternity wear, wellness apparel, and ethical fashion collections. Men’s organic apparel is witnessing steady growth as sustainable menswear gains popularity across casualwear and activewear categories. Children’s and infant apparel segments are expanding rapidly due to growing parental concerns regarding skin safety and exposure to chemically treated textiles.

End-Use Industry Insights

Fashion and lifestyle retail remains the largest end-use industry for organic apparel products, supported by growing integration of sustainable collections within mainstream fashion retail. Sportswear and fitness industries are among the fastest-growing application areas due to increasing demand for breathable, non-toxic, and performance-oriented fabrics. The hospitality and corporate uniform sector is also emerging as a high-growth segment as businesses adopt ESG-driven procurement strategies and environmentally responsible branding initiatives. Healthcare and wellness apparel applications are expanding steadily as consumers seek hypoallergenic and skin-friendly textile products.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Apparel Market Segmentations

By Product Type

- T-Shirts & Tops

- Shirts & Blouses

- Bottom Wear

- Dresses & Skirts

- Activewear & Sportswear

- Innerwear & Loungewear

- Kids & Baby Apparel

- Outerwear

- Workwear & Uniforms

By Material Type

- Organic Cotton

- Organic Hemp

- Organic Linen

- Organic Wool

- Organic Silk

- Bamboo-based Organic Fabrics

- Recycled Organic Blends

- Plant-based Bio-fabric Materials

By Consumer Category

- Men

- Women

- Children

- Infants & Toddlers

- Gender-neutral / Unisex Consumers

By Distribution Channel

- Online Retail

- Brand-owned E-commerce

- Online Marketplaces

- Specialty Sustainable Fashion Stores

- Department Stores

- Hypermarkets & Supermarkets

- Brand-exclusive Outlets

- Boutique Retailers

By End Use

- Fashion & Lifestyle Retail

- Sports & Fitness Industry

- Baby Care & Infant Products

- Hospitality & Corporate Uniforms

- Healthcare & Wellness Apparel

- Institutional & Educational Uniforms

- E-commerce Direct-to-Consumer Brands

Regional Insights

North America

North America accounted for approximately 34% of the global organic apparel market revenue in 2025, making it the leading regional market globally. The United States dominates regional demand due to strong consumer awareness regarding sustainability, high disposable income levels, and increasing adoption of ethical fashion products. Major retailers and fashion brands in the U.S. are rapidly expanding sustainable product portfolios to meet ESG commitments and shifting customer preferences. Canada is also experiencing rising demand for premium organic activewear and environmentally responsible outdoor clothing products.

Europe

Europe held nearly 31% share of the global market in 2025 and remains one of the most sustainability-focused apparel markets worldwide. Germany leads regional demand due to strong environmental awareness, favorable regulatory support, and widespread consumer adoption of sustainable fashion products. The United Kingdom and France are major contributors to regional growth, supported by expanding online retail penetration and premium ethical fashion demand. Nordic countries are also emerging as high-growth markets due to advanced circular economy initiatives and strong consumer preference for low-carbon apparel products.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 12% through 2031. India remains one of the world’s largest organic cotton producers and a key supplier of certified organic garments for global exports. China continues to strengthen sustainable textile manufacturing investments while also experiencing rising domestic demand for premium organic apparel. Japan and South Korea are witnessing increasing adoption of eco-friendly fashion products among urban consumers, while Southeast Asia is becoming an important low-cost sustainable textile manufacturing hub.

Latin America

Latin America represents a steadily growing market led by Brazil, Mexico, and Chile. Increasing environmental awareness, rising premium fashion demand, and growing investments in organic cotton farming are supporting market expansion across the region. Brazil is emerging as an important producer of sustainable textile materials and organic cotton exports. Regional fashion brands are also incorporating sustainable product lines to attract younger, environmentally conscious consumers.

Middle East & Africa

The Middle East and Africa region is gradually expanding due to rising premium retail penetration and sustainability-focused consumer trends. Gulf countries such as the UAE and Saudi Arabia are witnessing growing demand for luxury sustainable fashion products driven by affluent consumers and expanding international retail presence. South Africa remains a key market within Africa due to increasing awareness regarding ethical sourcing and environmentally responsible fashion products. Textile manufacturing investments in parts of Africa are also creating long-term opportunities for sustainable apparel production and exports.

Key Players in the Organic Apparel Market

- Patagonia

- Eileen Fisher

- Pact

- People Tree

- Organic Basics

- Thought Clothing

- Outerknown

- Tentree

- Amour Vert

- Beaumont Organic

- Everlane

- Finisterre

- Kotn

- Indigenous Designs

- Wear Pact LLC