Online Pet Food and Supplies Market Size

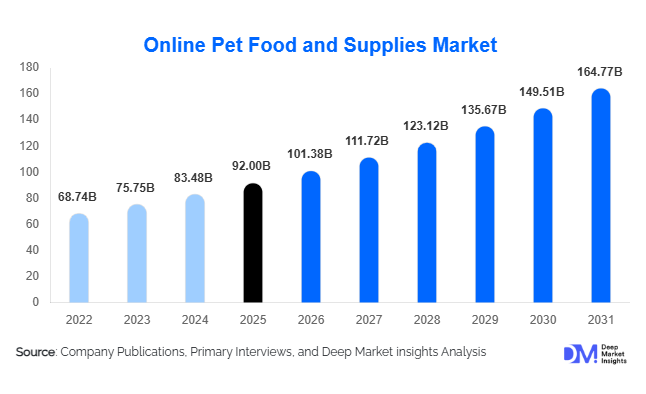

According to Deep Market Insights, the global online pet food and supplies market size was valued at USD 92 billion in 2025 and is projected to grow from USD 101.38 billion in 2026 to reach USD 164.77 billion by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). The market growth is primarily driven by rising pet ownership, increasing humanization of pets, and the rapid expansion of e-commerce platforms offering convenience, personalization, and subscription-based purchasing models.

Key Market Insights

- Pet food dominates online sales, accounting for nearly 68% of total market revenue due to recurring purchase behavior.

- Premium and functional pet nutrition is gaining traction, driven by increasing awareness of pet health and wellness.

- North America leads the global market, supported by high e-commerce penetration and strong consumer spending on pets.

- Asia-Pacific is the fastest-growing region, fueled by rising pet adoption and digital commerce expansion in China and India.

- Subscription-based purchasing models are rapidly expanding, improving customer retention and predictable revenue streams.

- AI-driven personalization and digital engagement tools are reshaping online pet retail experiences globally.

What are the latest trends in the online pet food and supplies market?

Rise of Subscription and Auto-Replenishment Models

Subscription-based purchasing is becoming a defining trend in the online pet food and supplies market. Consumers increasingly prefer automated delivery services for essentials such as pet food, litter, and supplements. These models enhance convenience while ensuring consistent product availability. Companies are leveraging predictive analytics to optimize delivery cycles and reduce churn rates. Subscription penetration is particularly strong in North America and Europe, while emerging markets are witnessing rapid adoption due to improving digital infrastructure and payment ecosystems.

Personalized and Health-Focused Pet Nutrition

The demand for personalized pet nutrition is reshaping product offerings. Online platforms are integrating AI-driven tools that recommend customized diets based on pet breed, age, weight, and health conditions. Functional foods, including grain-free, organic, and nutraceutical products, are gaining popularity. Additionally, integration of tele-veterinary consultations and digital health tracking is enabling platforms to offer comprehensive pet wellness ecosystems, enhancing customer engagement and driving premium product sales.

What are the key drivers in the online pet food and supplies market?

Growing Pet Humanization Trends

Pets are increasingly considered family members, leading to higher spending on premium food, accessories, and healthcare products. Consumers are prioritizing quality, safety, and nutrition, driving demand for organic and specialized pet products. This trend is particularly strong in developed markets, where disposable income levels support premiumization.

Expansion of E-commerce and Digital Infrastructure

The rapid growth of e-commerce platforms and mobile commerce has significantly boosted online pet product sales. Consumers benefit from convenience, wider product selection, competitive pricing, and doorstep delivery. Improved logistics networks, including same-day delivery services, have further enhanced customer satisfaction and accelerated market growth.

What are the restraints for the global market?

High Logistics and Delivery Costs

Shipping bulky products such as pet food leads to high logistics costs, impacting profit margins for online retailers. Free delivery expectations and rising fuel costs further exacerbate this challenge, particularly for smaller players lacking economies of scale.

Concerns Over Product Authenticity and Quality

Consumers remain cautious about counterfeit or substandard products sold online. Ensuring product authenticity, quality certifications, and transparent sourcing increases operational complexity and costs for companies, posing a restraint to market expansion.

What are the key opportunities in the online pet food and supplies industry?

Expansion into Emerging Markets

Emerging economies such as India, Brazil, and Indonesia present significant growth opportunities due to rising pet adoption and increasing internet penetration. Localized product offerings, digital payment integration, and improved logistics infrastructure can help companies capture these high-growth markets.

Integration of Health-Tech and Digital Services

The convergence of pet care and digital health presents new opportunities. Platforms offering tele-veterinary services, diagnostic tools, and personalized nutrition plans can differentiate themselves and command premium pricing. This integration enhances customer loyalty and expands revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 92 Billion |

| Market Size in 2026 | USD 101.38 Billion |

| Market Size in 2031 | USD 164.77 Billion |

| CAGR | 10.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pet food continues to dominate the online pet food and supplies market, accounting for approximately 68% of total market revenue in 2025. The segment’s leadership is primarily driven by its high purchase frequency and essential nature, as pet owners regularly replenish food supplies compared to discretionary purchases such as toys or accessories. Within this category, premium, organic, and functional pet foods are the fastest-growing sub-segments, supported by increasing awareness of pet nutrition, rising incidences of pet health issues, and a growing preference for veterinarian-recommended diets. Consumers are increasingly opting for grain-free, high-protein, and breed-specific formulations, further boosting value growth. Meanwhile, the pet supplies segment, including grooming products, accessories, toys, and hygiene items, accounts for the remaining share, with growth driven by pet humanization trends and demand for enrichment products that enhance pet well-being and engagement.

Pet Type Insights

Dogs represent the largest segment in the online pet food and supplies market, contributing approximately 52% of total revenue in 2025. This dominance is driven by higher global dog ownership rates, greater per-pet spending, and a broader range of product requirements, including specialized diets, grooming products, and accessories. Dog owners also exhibit stronger adoption of premium and subscription-based purchasing models, further strengthening segment growth. Cats form the second-largest segment, benefiting from increasing urban pet adoption due to their lower maintenance requirements. Additionally, segments such as birds, fish, and exotic pets are gradually expanding, supported by diversification in pet ownership and niche product innovation, although their contribution remains comparatively smaller.

Distribution Model Insights

Third-party marketplaces dominate the distribution landscape, accounting for approximately 55% of the market share in 2025. Their leadership is driven by extensive product assortments, competitive pricing, integrated logistics networks, and strong consumer trust. These platforms enable consumers to compare multiple brands and access reviews, which enhances purchase confidence. However, direct-to-consumer (D2C) channels are rapidly gaining traction, driven by brands seeking greater control over customer relationships, higher margins, and personalized engagement. D2C platforms are increasingly leveraging data analytics, subscription models, and customized offerings to build long-term customer loyalty, making them one of the fastest-growing distribution channels globally.

Delivery Model Insights

Subscription-based delivery models account for nearly 28% of the market and represent one of the fastest-growing segments. Their growth is primarily driven by convenience, cost savings, and automated replenishment for recurring purchases such as pet food and litter. These models enhance customer retention and provide predictable revenue streams for companies. While one-time purchases still dominate transaction volumes, quick commerce and same-day delivery services are emerging as key differentiators, particularly in urban markets where consumers demand speed and reliability. Investments in last-mile logistics and warehouse automation are further accelerating the adoption of these delivery models.

End-Use Insights

Household pet owners constitute the primary end-use segment, accounting for over 85% of total demand in 2025. This dominance is driven by the rising global pet population and increasing consumer spending on pet care. The veterinary and pet healthcare segment is the fastest-growing end-use category, supported by growing awareness of preventive healthcare, specialized diets, and supplements. Additionally, institutional buyers such as pet boarding facilities, grooming centers, and breeders are emerging as significant contributors to market demand. These businesses increasingly rely on online platforms for bulk procurement, benefiting from competitive pricing and efficient supply chain management.

Explore more data points, trends and opportunities Download Free Sample Report

Online Pet Food and Supplies Market Segmentations

By Product Type

- Pet Food

- Pet Supplies

By Pet Type

- Dogs

- Cats

- Birds

- Fish & Aquatics

- Small Mammals

- Reptiles & Exotic Pets

By Distribution Model

- Third-Party Marketplaces

- Brand-Owned Websites (D2C)

- Subscription-Based Platforms

- Omni-channel Retailers

By Delivery Model

- One-Time Purchase

- Subscription/Auto-Replenishment

- Same-Day/Quick Commerce Delivery

- Scheduled Delivery

By Customer Type

- Individual Consumers (B2C)

- Institutional Buyers

Regional Insights

North America

North America holds the largest share of the online pet food and supplies market, accounting for approximately 38% in 2025. The United States dominates the region with nearly 85% of regional demand. Growth in this region is driven by high pet ownership rates, high disposable incomes, and advanced e-commerce infrastructure. Additionally, widespread adoption of subscription-based purchasing, high awareness of premium pet nutrition, and the presence of major market players contribute to sustained growth. Technological advancements such as AI-driven personalization and fast delivery networks further strengthen regional dominance.

Europe

Europe accounts for around 27% of the global market, with key countries including the UK, Germany, and France. Regional growth is driven by strong consumer preference for sustainable, organic, and ethically sourced pet products. Well-established online retail ecosystems, coupled with stringent regulations ensuring product quality and safety, enhance consumer trust. Additionally, increasing pet humanization and rising adoption of premium products are key drivers supporting steady market expansion across Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 12%. China leads the regional market, contributing nearly 45% of demand, followed by India and Japan. Growth in this region is fueled by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing internet penetration. The growing popularity of pet ownership among younger demographics and the expansion of digital payment systems further accelerate online purchases. Additionally, local e-commerce giants and government initiatives supporting digital economies are key enablers of regional growth.

Latin America

Latin America is witnessing steady growth, led by Brazil and Mexico, with Brazil accounting for over 50% of regional demand. Growth drivers include increasing middle-class income levels, rising pet adoption rates, and improving e-commerce infrastructure. The region is also benefiting from growing awareness of pet health and nutrition, leading to increased demand for premium products. Expansion of logistics networks and cross-border trade is further supporting market development.

Middle East & Africa

The Middle East and Africa region is emerging as a promising market, with key countries including the UAE and South Africa. Growth is driven by rising disposable incomes, urbanization, and increasing awareness of pet care and wellness. The expansion of e-commerce platforms, coupled with improvements in logistics and digital payment systems, is enabling greater accessibility to pet products. Additionally, the growing expatriate population in the Middle East and rising pet adoption trends are contributing to increased demand across the region.

Key Players in the Online Pet Food and Supplies Market

- Mars Petcare

- Nestlé Purina PetCare

- Chewy Inc.

- Amazon

- Walmart

- Zooplus

- Petco Health and Wellness

- JD.com

- Alibaba Group

- Freshpet

- Blue Buffalo (General Mills)

- Spectrum Brands

- PetSmart

- Hill’s Pet Nutrition

- Colgate-Palmolive