Office Space Market Size

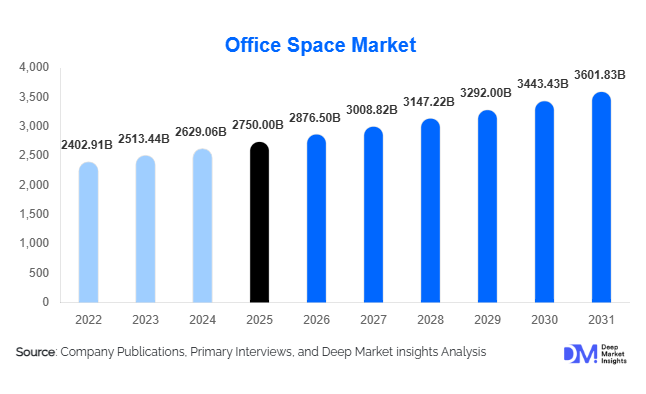

According to Deep Market Insights, the global office space market size was valued at USD 2,750 billion in 2025 and is projected to grow from USD 2,876.50 billion in 2026 to reach USD 3,601.83 billion by 2031, expanding at a CAGR of 4.6% during the forecast period (2026–2031). The office space market growth is primarily driven by the increasing adoption of hybrid work models, rising demand for flexible and managed workspaces, and growing investments in premium Grade A commercial real estate across major global cities.

Key Market Insights

- Flexible workspaces are rapidly gaining market share, driven by enterprises seeking agility and cost optimization in real estate portfolios.

- Grade A office spaces dominate globally, supported by demand for sustainability-certified, technology-enabled buildings.

- Asia-Pacific leads market growth, fueled by urbanization, outsourcing expansion, and strong demand in India and China.

- North America remains a mature yet innovation-driven market, with hybrid work reshaping leasing patterns.

- Suburban and secondary business districts are emerging as key demand centers due to decentralization trends.

- Smart building technologies and ESG compliance are becoming critical differentiators in leasing decisions.

What are the latest trends in the office space market?

Shift Toward Flexible and Hybrid Workspaces

The global office space market is witnessing a fundamental shift toward flexible workspace models, including co-working, serviced offices, and managed spaces. Enterprises are increasingly moving away from long-term leases toward short-term, scalable solutions that align with hybrid work strategies. This trend is particularly strong among startups, SMEs, and multinational corporations seeking to optimize operational costs and enhance workforce flexibility. Flexible workspace providers are expanding aggressively across Tier 2 and Tier 3 cities, offering plug-and-play solutions with minimal capital investment. This evolution is transforming office space from a static asset into a dynamic service-oriented offering.

Rise of Smart and Sustainable Buildings

Technology integration and sustainability are redefining modern office spaces. Developers are investing in IoT-enabled infrastructure, energy-efficient systems, and green building certifications to meet corporate ESG goals. Features such as smart access control, occupancy sensors, and AI-driven energy management systems are becoming standard in premium office buildings. Sustainability-focused designs not only reduce operational costs but also enhance tenant appeal, allowing landlords to command higher rental premiums. Governments worldwide are enforcing stricter environmental regulations, further accelerating the adoption of green office infrastructure.

What are the key drivers in the office space market?

Growth of Hybrid Work Models

The widespread adoption of hybrid work models is a major driver of the office space market. Companies are redesigning office layouts to focus on collaboration, innovation, and employee engagement rather than traditional desk-based work. This has led to increased demand for flexible layouts, shared spaces, and high-quality amenities. Hybrid work strategies are also encouraging the development of satellite offices and decentralized work hubs, expanding demand beyond central business districts.

Urbanization and Expansion in Emerging Markets

Rapid urbanization and economic growth in emerging markets, particularly in Asia-Pacific and the Middle East, are driving office space demand. Cities such as Bangalore, Shanghai, Dubai, and Riyadh are experiencing significant commercial real estate development. The expansion of IT, outsourcing, and financial services industries in these regions is fueling leasing activity and boosting occupancy rates. Government initiatives promoting foreign investment and infrastructure development further support market growth.

What are the restraints for the global market?

Oversupply in Mature Markets

Several developed markets, particularly in North America and parts of Europe, are facing an oversupply of office space. Elevated vacancy rates following the pandemic have led to downward pressure on rental prices and slower absorption of new developments. This imbalance between supply and demand poses challenges for developers and investors, impacting profitability and delaying new projects.

Uncertainty in Long-Term Workspace Strategies

Organizations are still experimenting with hybrid work models, leading to uncertainty in long-term office space requirements. This cautious approach has resulted in shorter lease durations and delayed expansion decisions. The lack of clarity around future workspace needs is affecting investment planning and limiting large-scale commitments in the office space market.

What are the key opportunities in the office space industry?

Expansion of Flexible Workspace Solutions

The growing demand for flexible work environments presents significant opportunities for operators and developers. Co-working and managed office providers can expand into emerging cities and underserved markets, leveraging asset-light models to scale rapidly. Enterprises are increasingly outsourcing workspace management, creating opportunities for service-oriented office space providers to capture market share.

Integration of ESG and Smart Technologies

Sustainability and digital transformation are creating new investment avenues in the office space market. Retrofitting existing buildings with energy-efficient systems and smart technologies can significantly enhance asset value and tenant retention. Developers focusing on green certifications and smart infrastructure are likely to benefit from premium pricing and higher occupancy rates.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2750 Billion |

| Market Size in 2026 | USD 2876.50 Billion |

| Market Size in 2031 | USD 3601.83 Billion |

| CAGR | 4.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Space Type Insights

Flexible workspaces account for approximately 28% of the global market in 2025, making them one of the fastest-growing segments globally. This growth is primarily driven by the increasing adoption of hybrid work models and the need for operational agility among enterprises. SMEs, startups, and even large corporations are shifting toward flexible workspace solutions such as co-working, serviced offices, and managed spaces to reduce capital expenditure and optimize real estate costs. The ability to scale space requirements dynamically, combined with plug-and-play infrastructure, is a major driver behind this segment’s expansion. Additionally, enterprises are increasingly outsourcing workplace management to flexible workspace providers, further accelerating growth.

Traditional office spaces continue to hold a significant share, particularly among large corporations with stable, long-term operational requirements and centralized workforce strategies. However, hybrid office models are rapidly emerging as a strategic middle ground, allowing organizations to combine headquarters with distributed satellite offices, thereby enhancing employee productivity and reducing commute-related inefficiencies.

Building Grade Insights

Grade A office spaces dominate the market with around 52% share in 2025, supported by strong demand for premium infrastructure, sustainability certifications, and technologically advanced facilities. The primary growth driver for this segment is the increasing corporate focus on employee experience, ESG compliance, and brand positioning. Multinational corporations and high-growth industries prefer Grade A buildings due to their superior amenities, energy efficiency, and compliance with global standards.

Additionally, Grade A buildings are benefiting from higher occupancy rates and rental premiums due to features such as smart building systems, wellness-oriented designs, and enhanced safety measures. In contrast, Grade B and C spaces are witnessing slower growth, as tenants increasingly migrate toward modern, high-performance office environments. This shift is also driving redevelopment and retrofitting activities in older buildings to meet evolving tenant expectations.

Ownership Model Insights

Leased office spaces account for nearly 70% of the global market, reflecting a strong preference for operational flexibility over ownership. The key driver for this segment is the need for businesses to maintain financial agility and avoid long-term capital commitments associated with property ownership. Leasing allows companies to adapt quickly to changing workforce dynamics, particularly in the context of hybrid work and uncertain economic conditions.

Long-term leases remain prevalent among large enterprises that require stable and secure office environments, while short-term leases are gaining traction among startups, SMEs, and project-based organizations. The growing popularity of flexible lease structures, including revenue-sharing and managed lease agreements, is further transforming the ownership landscape and enabling landlords to attract a broader tenant base.

Industry Vertical Insights

The IT & ITES sector leads the office space market with approximately 30% market share, driven by global outsourcing trends, digital transformation initiatives, and the expansion of technology hubs across emerging markets. The sector’s continuous need for scalable and high-quality office infrastructure is a major growth driver, particularly in countries such as India and the Philippines.

The BFSI sector is another significant contributor, driven by the modernization of financial services and the need for technologically advanced office environments to support digital banking operations. Consulting and professional services firms also contribute substantially, as they require strategically located office spaces in central business districts to maintain client accessibility. Emerging sectors such as life sciences, fintech, and media are further diversifying demand by requiring specialized office formats, including labs and innovation hubs.

Location Insights

Central Business Districts (CBDs) account for around 48% of the global market, driven by their strategic importance, superior connectivity, and proximity to key business ecosystems. The primary driver for CBD dominance is the concentration of corporate headquarters, financial institutions, and premium office developments in these areas, which enhances business visibility and operational efficiency.

However, suburban and emerging business hubs are witnessing faster growth due to lower rental costs, reduced congestion, and improved infrastructure. The rise of decentralized work models and satellite offices is encouraging companies to establish a presence in peripheral locations, enabling them to access a wider talent pool while optimizing costs. This trend is particularly prominent in large metropolitan regions where commute times and real estate costs are significant concerns.

End-Use Industry Insights

The IT & ITES industry remains the largest consumer of office space, supported by its global market size exceeding USD 1 trillion and continued expansion in outsourcing and digital services. The sector’s demand is driven by large-scale employment generation and the need for collaborative work environments. The BFSI sector, valued at over USD 25 trillion globally, is undergoing digital transformation, leading to increased demand for modern office spaces equipped with advanced technological infrastructure.

Life sciences, technology startups, and creative industries are emerging as high-growth end-use segments. These industries require specialized office environments, including research labs, innovation centers, and collaborative spaces, which are driving demand for customized real estate solutions. Export-driven demand is particularly strong in countries such as India and the Philippines, where service exports necessitate large-scale office infrastructure development. Additionally, the rise of remote-first companies establishing regional hubs is further contributing to diversified demand patterns.

Explore more data points, trends and opportunities Download Free Sample Report

Office Space Market Segmentations

By Space Type

- Traditional Office Space

- Co-working Spaces

- Managed Offices

- Serviced Offices

- Hybrid Office Models

By Building Grade

- Grade A Office Space

- Grade B Office Space

- Grade C Office Space

By Ownership Model

- Owner-Occupied Office Space

- Long-Term Lease

- Short-Term Lease

By Industry Vertical

- IT & ITES

- BFSI

- Consulting & Professional Services

- Healthcare & Life Sciences

- Manufacturing & Engineering

- Media & Entertainment

Regional Insights

North America

North America holds approximately 32% of the global office space market in 2025, with the United States accounting for the majority share. Key cities such as New York, San Francisco, Chicago, and Austin continue to drive demand due to their strong economic base and concentration of technology and financial services companies. The primary drivers for regional growth include high corporate spending on premium office infrastructure, rapid adoption of smart building technologies, and the presence of leading global enterprises.

Despite challenges related to hybrid work and elevated vacancy rates, demand for high-quality, flexible, and ESG-compliant office spaces remains strong. The region is also witnessing increased investment in retrofitting older buildings to meet modern standards, further supporting market stability.

Asia-Pacific

Asia-Pacific accounts for around 35% of the global market, making it the largest and fastest-growing region. China and India are the primary growth engines, with cities such as Shanghai, Beijing, Bangalore, Hyderabad, and Mumbai experiencing robust leasing activity. The key drivers for regional growth include rapid urbanization, expansion of the IT and outsourcing sectors, and increasing foreign direct investment.

Government initiatives such as smart city development and favorable business policies are further accelerating office space demand. India, in particular, is witnessing strong growth with a CAGR exceeding 7%, driven by its position as a global outsourcing hub and the rapid expansion of startup ecosystems.

Europe

Europe holds approximately 22% of the global office space market, with major contributions from the UK, Germany, and France. The region’s growth is primarily driven by stringent sustainability regulations and a strong focus on ESG compliance. Cities such as London, Berlin, and Paris are leading demand due to their status as financial and business hubs.

The increasing adoption of green building standards and energy-efficient infrastructure is a key driver, as companies seek to align with regulatory requirements and corporate sustainability goals. Additionally, the rise of flexible workspaces and co-working models is supporting growth across major European cities.

Middle East & Africa

The Middle East and Africa region is experiencing rapid growth, particularly in the UAE and Saudi Arabia. Cities such as Dubai, Abu Dhabi, and Riyadh are emerging as major commercial hubs. The primary drivers for regional growth include economic diversification initiatives, large-scale infrastructure investments, and government-led development programs such as Saudi Vision 2031.

Increased foreign investments, the establishment of free economic zones, and the expansion of multinational corporations in the region are further boosting office space demand. Africa is also witnessing gradual growth, supported by urbanization and the development of business districts in countries such as South Africa and Kenya.

Latin America

Latin America accounts for approximately 6–8% of the global market, with Brazil and Mexico leading regional demand. The primary growth drivers include urbanization, economic recovery, and increasing investments in commercial real estate. Cities such as São Paulo, Mexico City, and Santiago are key office space markets in the region.

The adoption of flexible workspaces and the gradual expansion of multinational corporations are supporting demand growth. However, economic volatility and political uncertainties remain challenges. Despite this, improving infrastructure and rising demand for modern office environments are expected to drive steady growth in the coming years.