Nonwoven Baby Diaper Market Size

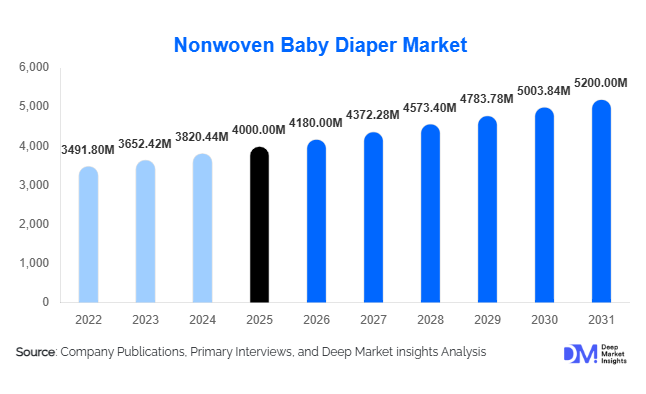

According to Deep Market Insights, the global nonwoven baby diaper market size was valued at USD 4,000 million in 2025 and is projected to grow from USD 4,180 million in 2026 to reach USD 5,200 million by 2031, expanding at a CAGR of 4.6% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for convenient infant hygiene solutions, rapid urbanization in emerging economies, and the widespread adoption of disposable baby care products. Nonwoven materials such as spunbond polypropylene, meltblown fabrics, and spunlace fibers are widely used in diapers due to their softness, breathability, high absorbency, and cost efficiency.

The rising number of working parents, increasing awareness about infant hygiene, and the expansion of modern retail and e-commerce channels are accelerating the adoption of disposable diapers globally. Emerging economies across Asia-Pacific, Latin America, and Africa are experiencing significant growth as disposable income rises and traditional cloth diapers are gradually replaced with technologically advanced disposable alternatives. Additionally, manufacturers are focusing on innovative diaper designs featuring thinner absorbent cores, breathable back sheets, and skin-friendly materials to improve comfort and performance.

Sustainability is also becoming an important factor shaping product innovation in the market. Manufacturers are investing in biodegradable fibers, plant-based nonwoven materials, and eco-friendly diaper designs to address environmental concerns associated with disposable hygiene products. As consumer preferences evolve toward high-performance and sustainable baby care products, the nonwoven baby diaper market is expected to witness steady growth over the forecast period.

Key Market Insights

- Disposable diapers dominate the market, accounting for nearly 78% of global revenue due to their convenience and superior hygiene benefits.

- Asia-Pacific leads global demand, supported by high birth rates and expanding middle-class populations in countries such as China and India.

- Pant-style diapers are increasingly popular, particularly among toddlers, due to ease of use and improved leakage protection.

- Eco-friendly and biodegradable diapers are gaining traction, driven by growing environmental awareness and regulatory pressure.

- E-commerce is emerging as a major distribution channel, enabling parents to purchase diapers through subscription-based and bulk purchase models.

- Advancements in nonwoven technology, including breathable multilayer fabrics and improved absorbent cores, are enhancing diaper performance and comfort.

What are the latest trends in the nonwoven baby diaper market?

Growing Demand for Sustainable and Biodegradable Diapers

Environmental sustainability is emerging as one of the most important trends shaping the nonwoven baby diaper market. Traditional disposable diapers contain synthetic materials that take decades to decompose in landfills. As environmental concerns increase, manufacturers are investing in biodegradable nonwoven fabrics made from bamboo fiber, viscose, and polylactic acid (PLA). Several diaper brands are also introducing compostable or partially biodegradable diapers designed to reduce environmental impact.

Governments and environmental organizations are encouraging the adoption of sustainable hygiene products through waste reduction policies and eco-label certifications. Consumers, particularly in Europe and North America, are increasingly willing to pay a premium for environmentally friendly baby products. As a result, biodegradable diapers and plant-based nonwoven materials are expected to become an important product segment in the coming years.

Technological Innovation in High-Performance Diapers

Technological advancements in nonwoven materials and diaper design are significantly improving product performance. Manufacturers are developing thinner diapers with higher absorbency by integrating advanced absorbent polymers and multilayer nonwoven structures such as SMS (spunbond–meltblown–spunbond). These fabrics provide improved moisture management, breathability, and skin comfort.

Premium diapers are also incorporating additional features such as wetness indicators, odor control layers, hypoallergenic topsheets, and advanced leakage protection systems. Smart diaper technologies equipped with moisture sensors are being developed to alert caregivers when a diaper needs to be changed. These innovations are enhancing convenience for parents while improving baby comfort, which is contributing to the growth of the premium diaper segment.

What are the key drivers in the nonwoven baby diaper market?

Rising Urbanization and Changing Lifestyles

Rapid urbanization and changing consumer lifestyles are major drivers of the nonwoven baby diaper market. Urban families increasingly prefer disposable diapers due to their convenience and time-saving benefits compared with traditional cloth nappies. The rising number of dual-income households has further accelerated this shift, as working parents seek practical childcare solutions that reduce household workload.

Urbanization is particularly strong in developing economies across Asia and Latin America, where disposable diaper penetration is still growing. Improved retail infrastructure and modern distribution channels are making diapers more accessible to a wider population, thereby supporting market expansion.

Increasing Awareness of Infant Hygiene

Parents are becoming more aware of the importance of maintaining proper hygiene for infants, especially in the early stages of development. Disposable diapers made with soft nonwoven fabrics provide better moisture management and reduce the risk of diaper rash and skin irritation. Healthcare professionals and maternity hospitals also recommend the use of high-quality disposable diapers for newborn care.

This increasing awareness of infant hygiene, combined with aggressive marketing by leading baby care brands, is driving consistent demand for nonwoven baby diapers across both developed and developing markets.

What are the restraints for the global market?

Environmental Concerns Related to Disposable Waste

One of the most significant restraints for the nonwoven baby diaper market is the environmental impact of disposable diaper waste. Millions of diapers are discarded daily worldwide, contributing significantly to landfill volumes. The plastic components used in traditional diapers take many years to degrade, raising concerns among environmental organizations and regulatory authorities.

These concerns are prompting governments to introduce stricter waste management regulations and encouraging manufacturers to adopt recyclable or biodegradable materials. However, transitioning to eco-friendly materials can increase production costs, which may limit adoption in price-sensitive markets.

Declining Birth Rates in Developed Economies

Another challenge affecting market growth is the declining birth rate in several developed countries. Nations such as Japan, South Korea, and parts of Europe are experiencing aging populations and lower fertility rates. This demographic shift reduces the potential customer base for baby diapers in these markets, leading manufacturers to focus more on emerging economies where birth rates remain relatively high.

What are the key opportunities in the nonwoven baby diaper industry?

Expansion in Emerging Markets

Emerging economies present one of the most promising opportunities for the nonwoven baby diaper market. Countries such as India, Indonesia, Brazil, and Nigeria have large infant populations and relatively low disposable diaper penetration rates. As household incomes increase and urbanization accelerates, more families are shifting from reusable cloth diapers to disposable alternatives.

Local manufacturers are also entering the market with affordable diaper products designed specifically for price-sensitive consumers. International brands are expanding their presence through localized manufacturing and partnerships with regional distributors, enabling them to tap into the growing demand in emerging markets.

Integration of Smart Diaper Technologies

Another opportunity lies in the development of smart diapers equipped with moisture sensors and connectivity features. These diapers can alert caregivers through mobile applications when a diaper is wet, improving baby care and convenience. Such technologies are particularly attractive to tech-savvy parents and premium consumers seeking advanced childcare solutions.

In addition to smart sensors, manufacturers are exploring new absorbent materials, antimicrobial coatings, and breathable fabric structures that enhance diaper performance. Continuous innovation in nonwoven materials and digital integration is expected to create new growth opportunities for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4000 Million |

| Market Size in 2026 | USD 4180 Million |

| Market Size in 2031 | USD 5200 Million |

| CAGR | 4.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Disposable nonwoven baby diapers dominate the market, accounting for approximately 78% of global revenue in 2025. These diapers are widely preferred due to their convenience, high absorbency, and hygienic design. Reusable or hybrid diapers, although smaller in market share, are gaining attention among environmentally conscious consumers who seek sustainable alternatives to traditional disposable products. Manufacturers are increasingly developing reusable diaper systems that incorporate removable absorbent layers made from nonwoven fabrics. The growing availability of biodegradable disposable diapers is also influencing product development within the disposable segment.

Application Insights

High-absorbency diapers represent the largest application segment, accounting for nearly 58% of the global market. These diapers are designed to provide extended protection during nighttime use and long travel periods, reducing the frequency of diaper changes. Medium-absorbency diapers are widely used for daytime applications and remain a staple product for infants and toddlers. Low-absorbency diapers are typically used for newborns or short-duration wear. The increasing demand for overnight protection and leak-proof diaper designs is driving innovation in absorbent materials and multilayer nonwoven structures.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape for nonwoven baby diapers, accounting for approximately 40% of global sales. These retail outlets provide consumers with easy access to a wide range of diaper brands and offer bulk purchasing options that reduce unit costs. Pharmacies and specialty baby care stores also play an important role in product distribution, particularly for premium and medical-grade diaper products. E-commerce platforms are rapidly gaining traction as parents increasingly prefer the convenience of online ordering and subscription-based diaper delivery services. Online channels also enable brands to reach consumers in remote regions where traditional retail infrastructure may be limited.

Explore more data points, trends and opportunities Download Free Sample Report

Nonwoven Baby Diaper Market Segmentations

By Product Type

- Disposable Nonwoven Baby Diapers

- Reusable / Hybrid Nonwoven Baby Diapers

By Diaper Format

- Tape-Style (Open Diapers)

- Pant-Style (Pull-Up Diapers)

- Training Pants

By Absorbency Level

- Low Absorbency Diapers

- Medium Absorbency Diapers

- High Absorbency / Overnight Diapers

By Diaper Size / Infant Age Group

- Newborn (0–3 Months)

- Small (3–8 kg Babies)

- Medium (6–11 kg Babies)

- Large (9–14 kg Babies)

- Extra Large (12 kg and Above)

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Online Retail & E-commerce Platforms

- Specialty Baby Care Stores

- Wholesale / Institutional Supply

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global nonwoven baby diaper market, accounting for nearly 45% of total revenue in 2025. Countries such as China, India, Indonesia, and Vietnam are major contributors to regional demand due to their large infant populations and rising disposable incomes. China alone represents approximately 22% of global demand, supported by strong domestic manufacturing capacity and a well-developed baby care industry. India is one of the fastest-growing markets in the region, driven by increasing urbanization, improving retail infrastructure, and rising awareness of infant hygiene.

North America

North America accounts for approximately 22% of the global nonwoven baby diaper market. The United States dominates regional demand due to high per-capita diaper consumption and the widespread adoption of premium baby care products. Consumers in this region prioritize high-performance diapers that offer superior comfort, breathability, and skin protection. Canada also contributes to market growth, supported by a strong retail network and increasing demand for eco-friendly baby products.

Europe

Europe represents nearly 20% of the global market, with Germany, the United Kingdom, France, and Italy leading regional demand. European consumers are highly conscious of sustainability, which is driving demand for biodegradable diapers and eco-friendly nonwoven materials. Strict environmental regulations in the region are encouraging manufacturers to develop recyclable diaper components and reduce plastic usage.

Latin America

Latin America accounts for roughly 7% of global demand. Brazil and Mexico are the largest markets in the region, supported by growing middle-class populations and improving retail distribution networks. Increasing awareness of infant hygiene and the availability of affordable diaper products are supporting market growth across the region.

Middle East & Africa

The Middle East and Africa region represents approximately 6% of the global market but is one of the fastest-growing regions. Countries such as Saudi Arabia, the United Arab Emirates, Nigeria, and South Africa are experiencing increasing diaper consumption due to high birth rates and improving economic conditions. Expanding retail infrastructure and growing awareness of baby hygiene products are also contributing to market growth.

Key Players in the Nonwoven Baby Diaper Market

- Procter & Gamble

- Kimberly-Clark

- Unicharm Corporation

- Essity

- Ontex Group

- Kao Corporation

- Hengan International Group

- Daio Paper Corporation

- First Quality Enterprises

- Domtar Corporation

- DSG International

- Nobel Hygiene

- Drylock Technologies

- Chiaus (Fujian) Industrial Development

- Fujian Shuangheng Group