Music Streaming Watches Market Size

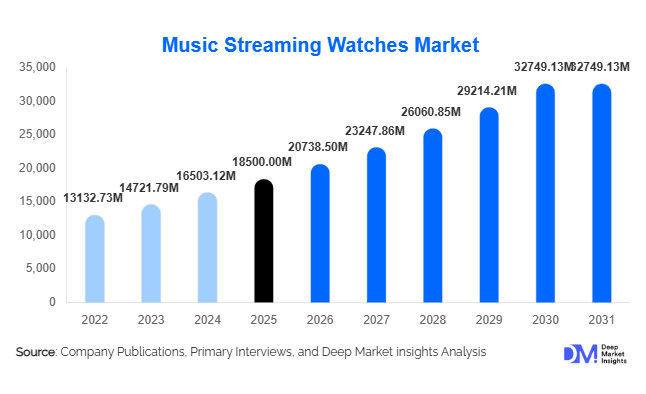

According to Deep Market Insights, the global music streaming watches market size was valued at USD 18,500 million in 2025 and is projected to grow from USD 20,738.50 million in 2026 to reach USD 32,749.13 million by 2031, expanding at a CAGR of 12.1% during the forecast period (2026–2031). The market growth is primarily driven by the increasing adoption of smartwatches with standalone connectivity, rising consumer preference for on-the-go music consumption, and growing integration between wearable devices and digital streaming platforms. The convergence of fitness tracking and entertainment features has significantly enhanced the value proposition of smartwatches, positioning music streaming as a key differentiator in premium and mid-range devices.

Key Market Insights

- Standalone LTE-enabled smartwatches are gaining traction, enabling users to stream music without relying on smartphones, especially during fitness and outdoor activities.

- Premium devices dominate revenue contribution, driven by advanced features such as offline playback, voice assistants, and seamless streaming app integration.

- North America dominates the market, supported by strong ecosystem integration and high adoption of subscription-based streaming services.

- Asia-Pacific is the fastest-growing region, driven by rising disposable incomes, urbanization, and expanding middle-class populations.

- Fitness and sports enthusiasts represent the largest user segment, highlighting the strong link between music consumption and workout routines.

- Technological advancements, including AI-driven personalization and improved battery efficiency, are enhancing user experience and driving adoption.

What are the latest trends in the music streaming watches market?

Shift Toward Standalone and Cellular Connectivity

The market is witnessing a strong transition toward standalone smartwatches equipped with LTE and emerging 5G connectivity. These devices allow users to stream music independently, eliminating the need for smartphone pairing. This trend is particularly prominent among fitness enthusiasts and urban consumers who prioritize convenience and mobility. Telecom operators are increasingly offering bundled data plans for wearables, further accelerating adoption. As connectivity improves and battery optimization advances, standalone streaming is expected to become the standard feature across mid-range and premium devices.

AI-Driven Personalization and Fitness Integration

Artificial intelligence is playing a growing role in enhancing music streaming experiences on wearable devices. Smartwatches are now capable of recommending playlists based on user activity, heart rate, and workout intensity, creating a highly personalized experience. Integration with fitness ecosystems is also expanding, allowing seamless synchronization between workout data and music preferences. This trend not only increases user engagement but also opens new monetization opportunities through premium subscriptions and app integrations, strengthening the overall value proposition of music streaming watches.

What are the key drivers in the music streaming watches market?

Rising Adoption of Wearable Technology

The rapid growth of the global wearable technology market is a primary driver for music streaming watches. Consumers are increasingly opting for multifunctional devices that combine health monitoring, communication, and entertainment. Music streaming capabilities enhance device utility, making smartwatches more appealing across diverse consumer segments. Continuous innovation in sensors, processors, and user interfaces has further strengthened adoption globally.

Growing Fitness and Wellness Awareness

Increasing awareness of health and fitness is significantly driving demand for music-enabled smartwatches. Music serves as a key motivator during workouts, and users prefer devices that provide seamless access to playlists without the need for smartphones. The integration of music streaming with fitness tracking features has created a compelling use case, particularly among younger and active demographics, contributing to sustained market growth.

What are the restraints for the global market?

Battery Consumption Challenges

Music streaming, particularly over cellular networks, places significant strain on smartwatch batteries. Despite advancements in power efficiency, limited battery life remains a key concern for users, especially during extended usage. This challenge affects user satisfaction and restricts the full potential of standalone streaming devices, making battery optimization a critical area for innovation.

High Device and Subscription Costs

The high cost of premium smartwatches, combined with subscription fees for music streaming services, can limit adoption in price-sensitive markets. While mid-range devices are becoming more affordable, they often lack advanced features such as LTE connectivity or extensive storage, creating a trade-off for consumers. Addressing affordability without compromising functionality remains a key challenge for market participants.

What are the key opportunities in the music streaming watches industry?

Expansion in Emerging Markets

Emerging markets such as India, Southeast Asia, and Latin America present significant growth opportunities due to rising disposable incomes and increasing smartphone penetration. Manufacturers can leverage localized pricing strategies and partnerships with regional streaming platforms to capture untapped demand. Government initiatives supporting local manufacturing further enhance market accessibility and competitiveness in these regions.

Integration with Enterprise Wellness Programs

Corporate wellness initiatives are creating new opportunities for music streaming watches. Organizations are increasingly adopting wearable devices to promote employee health and productivity. Integrating music streaming features into these programs enhances user engagement and satisfaction, making smartwatches a valuable tool in enterprise environments. This segment is expected to grow steadily, particularly in developed markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18500 Million |

| Market Size in 2026 | USD 20738.50 Million |

| Market Size in 2031 | USD 32749.13 Million |

| CAGR | 12.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Smartwatches with native music streaming capabilities dominate the market, accounting for approximately 48% of total revenue in 2025. These devices are leading primarily due to their standalone functionality enabled by LTE/eSIM connectivity, allowing users to stream music without smartphone dependency. This capability is particularly valuable for fitness users, commuters, and outdoor consumers who prioritize mobility and convenience. The segment’s growth is further driven by increasing integration with major streaming platforms, enhanced onboard storage (8GB–32GB), and AI-powered personalization features. Additionally, advancements in battery optimization and chip efficiency are reducing earlier limitations, strengthening adoption across premium and upper mid-range segments.

Fitness bands with music playback features are gaining traction in the budget category, especially in emerging markets, due to their affordability and basic offline playback functionality. However, their limited connectivity restricts full streaming capabilities. Hybrid watches remain a niche segment, as their focus on design and traditional watch aesthetics limits their technological integration. Overall, the market is clearly shifting toward fully connected, standalone smartwatches, making native streaming devices the primary revenue driver globally.

Application Insights

Fitness and sports applications represent the largest segment, contributing around 38% of the market share in 2025, and are the leading driver of demand. The dominance of this segment is attributed to the strong correlation between music consumption and workout performance, where users rely on music for motivation, endurance, and engagement. The increasing adoption of health tracking features such as heart rate monitoring, calorie tracking, and workout analytics—combined with personalized music recommendations—has significantly enhanced the value proposition of music streaming watches in this segment.

General consumer applications also hold a substantial share, driven by the convenience of accessing entertainment on the go without smartphones. Urban consumers increasingly prefer wearable devices that combine lifestyle and entertainment functionalities. Emerging applications in corporate wellness programs and lifestyle management are expanding market scope, as organizations invest in wearable devices to improve employee productivity and health engagement. This diversification of applications is expected to further accelerate market penetration across both developed and emerging economies.

Distribution Channel Insights

Online retail channels dominate the distribution landscape, accounting for approximately 55% of total sales in 2025. This segment leads due to price transparency, extensive product availability, direct-to-consumer (D2C) strategies, and the ability to compare features and reviews in real time. The rapid growth of e-commerce platforms, coupled with promotional pricing and easy financing options, has significantly boosted online sales, particularly in Asia-Pacific and North America.

Offline retail channels, including brand stores and electronics outlets, continue to play a critical role in premium device sales, where consumers value hands-on experience, brand trust, and personalized consultation. This channel remains important for high-value purchases and first-time buyers. Meanwhile, telecom bundling is emerging as a high-growth distribution channel, particularly for LTE-enabled smartwatches, where operators offer bundled data plans and device financing. This model is gaining traction in developed markets and is expected to expand further with 5G adoption.

Explore more data points, trends and opportunities Download Free Sample Report

Music Streaming Watches Market Segmentations

By Product Type

- Smartwatches with Native Streaming

- Smartwatches with Paired Streaming

- Hybrid Watches with Limited Streaming

- Fitness Bands with Music Playback

By Application

- Fitness and Sports

- General Consumer/Lifestyle

- Professional Athletes

- Corporate Wellness Programs

By Distribution Channel

- Online Retail

- Brand Stores & Electronics Retailers

- Department Stores

- Telecom Provider Stores

- Third-Party Distributors

By Connectivity Type

- Cellular (4G/LTE/5G)

- Wi-Fi Enabled

- Bluetooth Only

By Price Range

- Budget (< $150)

- Mid-Range ($150–$400)

- Premium (> $400)

Regional Insights

North America

North America holds the largest market share at approximately 35% in 2025, with the United States accounting for nearly 75% of regional demand. Growth in this region is primarily driven by high disposable income, strong penetration of premium smartwatches, and widespread adoption of subscription-based music streaming services. Additionally, the presence of leading technology companies and well-established ecosystems enhances seamless integration between devices and services. The region also benefits from advanced telecom infrastructure, high LTE/5G penetration, and strong consumer preference for standalone wearable devices, making it the most mature market globally.

Europe

Europe accounts for around 25% of the global market, with key countries including Germany, the United Kingdom, and France driving demand. Regional growth is supported by a strong fitness culture, increasing health awareness, and rising adoption of wearable technology. Consumers in Europe prioritize sustainability and functionality, leading to increased demand for durable, high-performance devices. Additionally, expanding digital ecosystems, growing adoption of premium subscription services, and favorable regulatory support for digital innovation are key drivers. Urbanization and high smartphone penetration further contribute to the steady growth of music streaming watches in this region.

Asia-Pacific

Asia-Pacific represents approximately 28% of the market and is the fastest-growing region, with a CAGR exceeding 14%. China and India are the primary growth engines, driven by rapid urbanization, rising disposable incomes, and expanding middle-class populations. China’s dominance in manufacturing and exports ensures strong supply chain advantages and cost competitiveness, while India is witnessing significant demand growth due to increasing affordability, government initiatives such as local manufacturing programs, and rising digital consumption. Additionally, the region benefits from high smartphone penetration, growing e-commerce adoption, and a young, tech-savvy population. Japan and South Korea contribute through advanced technology adoption and premium device demand, further strengthening regional growth.

Latin America

Latin America holds approximately 6% of the global market, with Brazil and Mexico leading demand. Growth in this region is driven by increasing smartphone penetration, expanding internet connectivity, and the rapid growth of e-commerce platforms. Consumers are gradually shifting toward mid-range smartwatches that offer music streaming capabilities at affordable prices. Additionally, improving digital payment infrastructure and rising awareness of fitness and lifestyle products are supporting adoption. While economic fluctuations remain a challenge, the region presents strong long-term growth potential due to its expanding urban population and digital transformation.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of the market, with growth driven by rising urbanization, increasing disposable incomes, and growing interest in fitness and lifestyle technologies. The UAE and Saudi Arabia are key markets, supported by high consumer spending power, strong demand for premium products, and rapid adoption of advanced digital services. In Africa, the market is gradually emerging due to improving telecom infrastructure, increasing smartphone adoption, and expanding access to digital services. Government investments in digital transformation and smart city initiatives are further expected to support long-term growth in the region.

Key Players in the Music Streaming Watches Market

- Apple Inc.

- Samsung Electronics

- Garmin Ltd.

- Fitbit (Google)

- Huawei Technologies

- Xiaomi Corporation

- Fossil Group

- Amazfit (Zepp Health)

- Sony Corporation

- LG Electronics

- Polar Electro

- Suunto

- Oppo

- Realme

- Noise (Nexxbase)