Monitor Stand Market Size

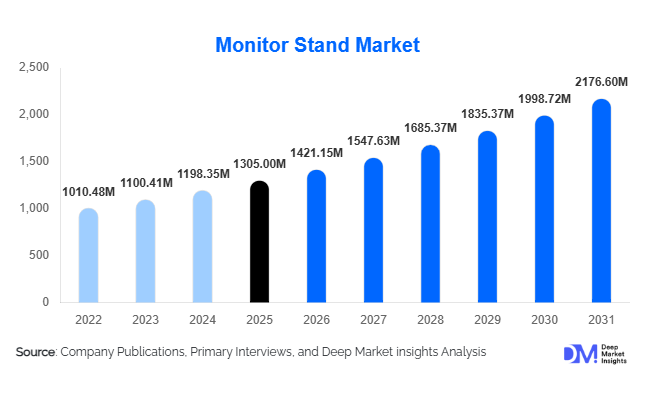

According to Deep Market Insights, the global monitor stand market size was valued at USD 1,305 million in 2025 and is projected to grow from USD 1,421.15 million in 2026 to reach USD 2,176.60 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). Market growth is primarily driven by rising adoption of ergonomic workplace solutions, expansion of hybrid work environments, and increasing deployment of multi-monitor workstations across corporate, gaming, and professional applications. As organizations prioritize employee productivity, posture improvement, and workspace optimization, monitor stands are transitioning from optional accessories into essential workstation infrastructure.

Key Market Insights

- Ergonomic workplace adoption is accelerating globally, encouraging enterprises to standardize adjustable monitor stands across offices and home workspaces.

- Monitor arms and adjustable mounting systems dominate demand due to flexibility, space optimization, and multi-screen compatibility.

- Asia-Pacific leads global production and consumption, supported by expanding IT infrastructure and manufacturing capabilities.

- Corporate offices remain the largest end-use segment, while gaming and home-office users represent the fastest-growing consumer base.

- E-commerce channels are transforming distribution, enabling direct-to-consumer ergonomic product adoption worldwide.

- Technological innovation, including gas-spring arms, modular mounting ecosystems, and integrated cable management, is reshaping product differentiation.

What are the latest trends in the monitor stand market?

Shift Toward Ergonomic and Adjustable Workstations

Organizations worldwide are prioritizing ergonomic workplace investments to improve employee comfort and productivity. Adjustable monitor stands allowing height, tilt, and rotation customization are replacing fixed desktop risers. Employers increasingly integrate ergonomic accessories into workplace design standards, particularly in IT services, finance, and creative industries where prolonged screen exposure is common. Regulatory focus on occupational health and workplace wellness programs further accelerates adoption. Adjustable monitor arms also support sit-stand desk environments, enabling flexible workspace arrangements aligned with modern office design philosophies.

Growth of Hybrid Work and Home Office Setups

The expansion of hybrid and remote work models has significantly increased demand for compact, aesthetically designed monitor stands suitable for residential environments. Employees are investing in professional-grade home workstations, often supported by employer reimbursement programs. Manufacturers are responding with foldable, lightweight, and multi-device compatible stands that balance functionality with interior aesthetics. This trend is also encouraging premium product adoption, as consumers prioritize durability, ergonomic comfort, and workspace organization within limited home office spaces.

What are the key drivers in the monitor stand market?

Expansion of Multi-Monitor Work Environments

Modern professional workflows increasingly require dual or multi-monitor configurations to enhance productivity and multitasking efficiency. Industries such as software development, financial trading, gaming, and media production rely heavily on flexible display positioning. Monitor arms enabling dynamic adjustments and desk space optimization are becoming standard equipment, significantly boosting global demand.

Rising Awareness of Workplace Health and Productivity

Employers recognize the economic benefits of ergonomic investments, including reduced employee fatigue, improved posture, and enhanced productivity outcomes. Occupational safety guidelines in developed markets encourage ergonomic workstation adoption, driving large-scale procurement of adjustable monitor stands across enterprises. Educational institutions and healthcare facilities are also adopting ergonomic equipment to improve user comfort during extended screen usage.

What are the restraints for the global market?

Price Sensitivity in Emerging Economies

Despite growing awareness, adoption in price-sensitive markets remains constrained by the availability of low-cost unbranded alternatives. Premium ergonomic solutions often face resistance among small businesses and individual consumers due to upfront costs. This pricing pressure intensifies competition and limits margin expansion for established brands.

Compatibility and Workspace Limitations

Older office furniture and compact desks may not support clamp-based or adjustable mounting systems, requiring additional infrastructure upgrades. Organizations reluctant to redesign workspaces may delay adoption, creating temporary barriers to market expansion despite long-term ergonomic benefits.

What are the key opportunities in the monitor stand industry?

Smart Workspace Integration

Monitor stands are evolving into integrated workstation hubs featuring USB docking, cable management, wireless charging platforms, and modular mounting ecosystems. As smart offices gain traction, manufacturers integrating connectivity features and IoT-enabled posture monitoring capabilities can capture premium market segments. Partnerships between ergonomic equipment companies and office technology providers are expected to accelerate innovation and revenue diversification.

Emerging Market Corporate Expansion

Rapid office infrastructure growth across India, Southeast Asia, Eastern Europe, and Latin America presents substantial opportunities. Expanding outsourcing industries, startup ecosystems, and government-led digitalization initiatives are driving workstation installations at scale. Localized manufacturing and cost-efficient distribution networks allow new entrants to serve growing SME and shared workspace segments effectively.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1305 Million |

| Market Size in 2026 | USD 1421.15 Million |

| Market Size in 2031 | USD 2176.60 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global monitor stand market is primarily driven by the increasing need for ergonomic workspace optimization and flexible display configurations across corporate, residential, and institutional environments. Monitor arms and mounting systems dominate the product landscape, accounting for nearly 38% of global revenue, supported by their superior flexibility, height adjustability, and compatibility with multi-monitor setups. Organizations increasingly deploy articulated monitor arms to improve posture alignment, reduce workplace fatigue, and enhance productivity, particularly in hybrid and high-performance work environments. The leading segment growth is further supported by rising adoption of dual- and triple-monitor workstations in IT, financial trading, and creative industries where screen accessibility directly impacts workflow efficiency.

Adjustable monitor stands are witnessing strong growth momentum as enterprises prioritize ergonomic compliance and employee wellness initiatives. These products offer cost-effective ergonomic upgrades without requiring permanent installation, making them attractive for both corporate and home office users. Fixed monitor stands continue to address entry-level demand, particularly in educational institutions, government offices, and budget-sensitive markets where functionality outweighs advanced adjustability features. Meanwhile, portable and foldable stands are gaining traction among hybrid workers and mobile professionals seeking lightweight, adaptable workspace solutions. The broader industry trend reflects a gradual shift from static risers toward premium adjustable and modular mounting ecosystems that enhance workspace efficiency while supporting evolving flexible work models.

Material Insights

Material innovation remains a key factor shaping product performance, durability, and aesthetic appeal within the monitor stand market. Metal-based monitor stands, particularly aluminum and steel constructions, hold approximately 46% market share due to their superior load-bearing capacity, structural stability, and premium finish. The leading segment driver is the growing demand for durable ergonomic solutions capable of supporting larger ultrawide and curved monitors, which require stronger mounting structures and enhanced safety reliability in professional environments.

Plastic and polymer-based stands continue to cater to cost-sensitive consumers and lightweight applications, particularly within home offices and educational settings. These materials offer affordability and ease of transportation while maintaining adequate functionality for smaller displays. Wood and engineered material designs are increasingly adopted in modern office environments emphasizing sustainability, interior aesthetics, and biophilic workplace design principles. Additionally, composite materials that combine metal strength with lightweight construction are emerging as a preferred choice for premium ergonomic products, reflecting ongoing advancements in materials engineering aimed at balancing durability, portability, and environmental considerations.

Mounting Type Insights

Mounting configuration plays a critical role in determining workspace efficiency and installation flexibility. Clamp-based mounting systems represent the leading segment, accounting for nearly 34% of market share, primarily driven by their ability to maximize desk space without permanent modification. The leading segment driver is the rising adoption of modular office furniture and shared workstations, where easy installation, repositioning capability, and desk preservation are essential requirements. Clamp mounts enable quick deployment in corporate environments transitioning toward agile workspace layouts.

Freestanding desktop stands remain widely used in traditional office setups and educational environments where mobility and simplicity are prioritized. Wall-mounted systems are expanding steadily, particularly in healthcare facilities, command centers, and compact workspaces where desk space optimization is critical. Pole-based multi-monitor systems are increasingly deployed in trading floors, surveillance centers, and broadcasting environments requiring complex display arrangements and centralized viewing structures. The growing diversity of mounting types reflects the expanding range of professional applications demanding customized display positioning solutions.

End-Use Insights

Corporate offices account for approximately 44% of total market demand, supported by enterprise procurement programs, workplace modernization initiatives, and growing awareness of occupational health standards. The leading segment driver is the global transition toward hybrid work models, encouraging organizations to invest in ergonomic infrastructure that enhances employee comfort and productivity across both centralized offices and remote setups.

Gaming and home users represent the fastest-growing end-use segment, driven by increasing esports participation, content creation activities, and rising investments in personalized home workstations. Gamers increasingly require adjustable monitor positioning to support immersive viewing angles and extended usage hours. Educational institutions are expanding adoption of monitor stands to support digital learning infrastructure and computer-based classrooms, while healthcare facilities deploy adjustable mounts in diagnostic stations, nursing workspaces, and telemedicine environments to improve workflow ergonomics. Industrial control rooms, engineering facilities, and creative studios are emerging application areas requiring advanced multi-display configurations to manage data-intensive operations efficiently.

Distribution Channel Insights

Distribution dynamics within the monitor stand market are evolving alongside digital commerce expansion and enterprise procurement transformation. Online retail channels dominate global sales, contributing nearly 37% of market revenue as consumers increasingly purchase ergonomic accessories through e-commerce platforms offering wider product selection, competitive pricing, and direct-to-consumer availability. The leading growth driver for online channels is the rapid expansion of home office setups and individual consumer purchasing behavior following remote work adoption.

Offline retail stores continue to play an important role in enterprise purchasing decisions and experiential product evaluation, particularly for premium ergonomic solutions where physical testing influences buying behavior. Direct B2B sales channels and office furniture integrators remain essential for large-scale corporate deployments, frequently bundling monitor stands within complete workstation and ergonomic furniture solutions. Strategic partnerships between manufacturers and workspace solution providers are further strengthening institutional distribution networks globally.

Explore more data points, trends and opportunities Download Free Sample Report

Monitor Stand Market Segmentations

By Product Type

- Fixed Monitor Stands

- Adjustable Monitor Stands

- Monitor Arms & Mount Stands

- Portable/Foldable Monitor Stands

By Material Type

- Metal

- Plastic & Polymer-Based

- Wood & Engineered Wood

- Glass & Composite Materials

By Mounting Type

- Freestanding Desktop Stands

- Clamp-Based Mounts

- Wall-Mounted Systems

- Pole-Based Multi-Monitor Systems

By End Use

- Corporate Offices

- Gaming & Home Users

- Educational Institutions

- Healthcare Facilities

- Industrial & Control Rooms

- Media & Creative Studios

By Distribution Channel

- Online Retail

- Offline Retail Stores

- B2B Direct Sales

- Office Furniture Integrators

Regional Insights

North America

North America accounted for approximately 32% of global market share in 2025, led by the United States, where ergonomic compliance standards and hybrid work adoption remain highly advanced. Regional growth is driven by strong corporate investment in employee wellness programs, increasing replacement demand for ergonomic office accessories, and widespread adoption of multi-monitor workstations across technology, finance, and creative industries. The expansion of remote and hybrid work policies continues to stimulate residential demand for ergonomic equipment. Canada demonstrates steady adoption supported by digital education initiatives and government-backed workplace safety regulations, contributing to consistent regional growth.

Europe

Europe holds nearly 24% market share, with Germany, the United Kingdom, and France serving as key demand centers supported by stringent workplace safety regulations and a mature office furniture ecosystem. Regional growth is driven by strong regulatory emphasis on occupational ergonomics, rising corporate sustainability commitments, and increasing adoption of premium office infrastructure. Scandinavian countries exhibit particularly high ergonomic adoption rates due to advanced workplace wellness policies and environmentally conscious procurement practices. The region’s focus on sustainable materials and long product lifecycles further supports demand for high-quality adjustable monitor stands.

Asia-Pacific

Asia-Pacific represents the largest regional market with approximately 35% share and is also the fastest-growing region, expanding at over 10% CAGR. Growth is primarily driven by rapid urbanization, expanding IT and business process outsourcing industries, and increasing office infrastructure development across emerging economies. China dominates both manufacturing output and domestic consumption, benefiting from strong electronics ecosystems and competitive production capabilities. India is experiencing accelerated growth due to expanding IT services, startup ecosystem development, and rising adoption of home office setups among young professionals. Japan and South Korea continue to drive demand for technologically advanced and premium ergonomic solutions within highly digitalized workplaces and gaming communities.

Latin America

Latin America accounts for roughly 9% of global demand, led by Brazil and Mexico. Regional market expansion is supported by increasing outsourcing activities, gradual modernization of corporate office environments, and rising awareness of ergonomic workplace practices. Growth is further driven by expanding technology sectors and improving internet penetration, which supports both enterprise digital transformation and e-commerce adoption. Although economic volatility influences purchasing cycles, steady investments in professional workspace infrastructure continue to support long-term market development.

Middle East & Africa

The Middle East and Africa region is witnessing emerging demand driven by large-scale smart city initiatives, commercial real estate expansion, and workplace digitalization programs. Countries such as the United Arab Emirates and Saudi Arabia are investing heavily in modern office infrastructure as part of economic diversification strategies, creating opportunities for ergonomic workstation solutions. Government-led digital transformation initiatives and corporate expansion across finance, healthcare, and technology sectors are supporting market adoption. In Africa, South Africa leads regional demand, supported by growing enterprise modernization and increasing awareness of employee productivity and workplace health standards.

Key Players in the Monitor Stand Market

- Ergotron, Inc.

- Humanscale Corporation

- Fellowes Brands

- Loctek Ergonomic Technology Corp.

- Herman Miller Inc.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Ltd.

- Atdec Pty Ltd

- Vogel’s Products BV

- AVLT

- Mount-It!

- 3M Company

- Vari (Varidesk LLC)

- Kensington (ACCO Brands)