Modular Fitness Furniture Market Size

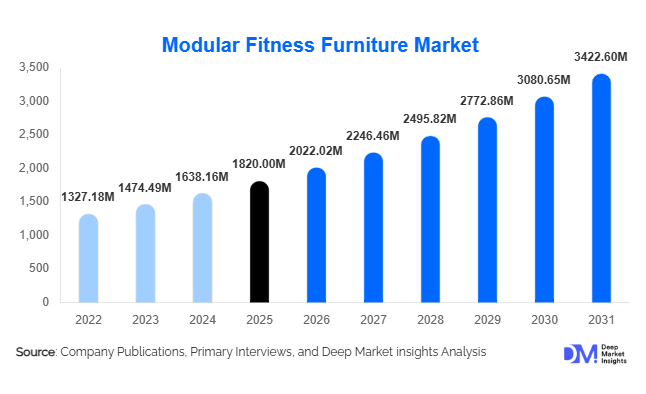

According to Deep Market Insights, the global modular fitness furniture market size was valued at USD 1,820 million in 2025 and is projected to grow from USD 2,022.02 million in 2026 to reach USD 3,422.60 million by 2031, expanding at a CAGR of 11.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing urbanization, shrinking residential spaces, rising home fitness adoption, and the convergence of smart furniture with connected workout ecosystems. Growing consumer demand for space-efficient, aesthetic, and multifunctional furniture solutions is reshaping home fitness infrastructure globally.

Key Market Insights

- Residential applications account for over 52% of global demand, driven by compact urban housing and remote work culture.

- Wall-mounted modular systems dominate installation types, contributing nearly 41% of 2025 revenue due to space optimization benefits.

- North America leads the global market with 34% share, supported by strong consumer spending and home gym penetration.

- Asia-Pacific is the fastest-growing region, expanding at approximately 13% CAGR, fueled by urban apartment demand in China, Japan, and India.

- Direct-to-consumer (D2C) online channels represent 36% of sales, highlighting the shift toward customization and digital-first purchasing.

- Integration of smart sensors, AI coaching, and connected fitness ecosystems is transforming product differentiation and pricing strategies.

What are the latest trends in the modular fitness furniture market?

Smart-Integrated Modular Systems

Manufacturers are embedding IoT sensors, AI-powered performance tracking, and connected training platforms into modular units. Companies such as Tonal Systems and Tempo Fitness are integrating digital coaching with compact wall-mounted strength systems, enabling subscription-based revenue models. Consumers increasingly seek seamless integration between hardware and fitness apps, enhancing engagement and recurring monetization. The trend is particularly strong in North America and Europe, where connected fitness adoption remains high.

Minimalist & Interior-Integrated Designs

Modern consumers demand fitness furniture that blends with interior aesthetics. Convertible gym walls, foldable benches with concealed storage, and bed-to-gym hybrid units are gaining traction. Design-focused brands are collaborating with interior architects to ensure seamless integration into smart homes. Sustainable materials such as engineered wood composites and recycled metals are increasingly used to align with eco-conscious buyer preferences.

What are the key drivers in the modular fitness furniture market?

Growth in Home Fitness Culture

The shift toward home-based workouts remains a major growth catalyst. Consumers value privacy, flexibility, and long-term cost savings compared to gym memberships. Modular solutions provide space-efficient alternatives to bulky gym equipment, making them particularly attractive in metropolitan apartments.

Urban Space Constraints

Declining apartment sizes in cities such as New York, Tokyo, and London have accelerated demand for multifunctional furniture. Modular fitness units allow living rooms or bedrooms to transform into temporary workout areas, addressing spatial limitations without permanent infrastructure changes.

What are the restraints for the global market?

High Initial Investment

Premium modular systems often cost significantly more than standalone fitness equipment, limiting adoption in price-sensitive regions. Customization and installation services further increase upfront expenditure.

Installation & Customization Complexity

Wall-mounted and built-in systems require professional installation and structural compatibility, creating logistical challenges. Extended lead times for customized units may restrict mass-market scalability.

What are the key opportunities in the modular fitness furniture industry?

Corporate Wellness Infrastructure

Hybrid work models are encouraging companies to invest in compact in-office wellness solutions. Modular fitness pods and collapsible gym stations are being deployed in corporate offices and co-working spaces, representing one of the fastest-growing end-use segments with a CAGR exceeding 13%.

Real Estate Developer Partnerships

Collaboration with smart housing developers presents long-term growth potential. Embedding modular gym walls into new residential projects can create recurring bulk demand. Urban redevelopment initiatives in the Asia-Pacific and the Middle East further strengthen this opportunity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1820 Million |

| Market Size in 2026 | USD 2022.02 Million |

| Market Size in 2031 | USD 3422.60 Million |

| CAGR | 11.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Modular strength training furniture leads the global modular fitness furniture market, accounting for approximately 38% of total revenue in 2025. The segment’s leadership is primarily driven by the growing global preference for strength and resistance training as a core component of home fitness routines. Wall-integrated squat racks, foldable power cages, adjustable weight benches with concealed storage, and resistance-based smart systems command higher average selling prices (ASPs) compared to cardio-focused alternatives, significantly contributing to revenue dominance. In addition, strength-focused modular units offer multifunctionality, supporting compound exercises, suspension training, and bodyweight workouts, making them more versatile within limited spaces.

Cardio-integrated modular furniture, including foldable treadmill desks and concealed rowing units, is expanding steadily, particularly in premium urban apartments where users prefer low-noise and low-impact solutions. Meanwhile, hybrid all-in-one gym walls that combine storage, resistance training, and digital coaching are gaining traction in smart homes. Senior-friendly and rehabilitation-focused modular systems are emerging as a niche growth area, driven by aging populations in North America, Europe, and Japan, where demand for safe, low-impact, home-based exercise solutions is rising.

Material Insights

Powder-coated steel and alloy frames dominate the material segment, holding nearly 44% of the global market share in 2025. The leading position of this segment is supported by its superior load-bearing capacity, structural durability, and long product lifespan, critical factors for strength-training modules. Steel-based modular systems are preferred in both residential and commercial installations due to enhanced safety and compliance with weight resistance standards. Additionally, manufacturers benefit from predictable fabrication processes and scalable industrial production of steel frames, supporting margin stability.

Engineered wood and composite panels are widely adopted in residential-centric designs where aesthetics and interior harmony are prioritized. These materials allow modular units to blend seamlessly with cabinetry and contemporary décor. Aluminum systems are gaining traction in portable and foldable units due to their corrosion resistance and lightweight characteristics, especially in humid climates and export-driven markets.

Distribution Channel Insights

Direct-to-consumer (D2C) online platforms contribute approximately 36% of global sales, making them the leading distribution channel. The segment’s dominance is fueled by growing consumer preference for product customization, 3D room visualization tools, augmented reality previews, and bundled subscription-based digital fitness services. Online channels also enable manufacturers to maintain higher margins by bypassing intermediaries while collecting consumer usage data for product optimization.

Specialty fitness retailers and premium furniture chains continue to play an important role in experiential purchases, particularly for high-value installations where consumers prefer physical inspection before committing to premium investments. B2B contracts are expanding rapidly through hospitality chains, corporate wellness programs, and residential developers, providing recurring bulk-order opportunities for manufacturers.

End-Use Insights

The residential segment dominates with 52% share of the 2025 market (approximately USD 946 million), driven by increasing urbanization, remote work trends, and rising health consciousness. Compact city apartments in metropolitan hubs are creating strong demand for multifunctional furniture that optimizes limited square footage. The leading driver for this segment is the continued preference for home-based workouts combined with interior-integrated design solutions.

Corporate offices represent the fastest-growing end-use segment, supported by workplace wellness initiatives and hybrid work infrastructure investments. Companies are installing modular fitness pods to enhance employee productivity and retention. The hospitality sector is integrating in-room modular gym systems within luxury hotels to differentiate guest experiences. Rehabilitation centers and physiotherapy clinics are increasingly adopting modular systems tailored for senior and post-injury patients, expanding application scope beyond mainstream fitness. Export-driven demand is also rising, particularly from Europe to the Middle East, where luxury real estate and mixed-use developments are expanding rapidly.

Explore more data points, trends and opportunities Download Free Sample Report

Modular Fitness Furniture Market Segmentations

By Product Type

- Modular Strength Training Furniture

- Modular Cardio-Integrated Furniture

- Multi-Functional Hybrid Gym Units

- Senior & Rehabilitation Modular Systems

By Material

- Powder-Coated Steel & Alloy Frames

- Engineered Wood & Composite Panels

- Aluminum Modular Systems

- Sustainable & Recycled Materials

By Distribution Channel

- Direct-to-Consumer (Online)

- Specialty Fitness Retail Stores

- Furniture & Home Improvement Chains

- B2B/Commercial Contracts

By End-Use

- Residential

- Commercial Fitness Centers

- Corporate Offices & Co-Working Spaces

- Hospitality (Hotels & Serviced Apartments)

- Healthcare & Rehabilitation Centers

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025 (around USD 620 million), making it the largest regional market. The United States accounts for nearly 80% of regional demand, driven by high disposable income, strong smart home penetration, and widespread adoption of connected fitness platforms. The mature home fitness culture, combined with a strong e-commerce ecosystem, supports high D2C sales penetration. Canada contributes stable growth, particularly in urban centers such as Toronto and Vancouver, where condominium living and wellness awareness are expanding. The primary regional growth driver is the sustained consumer preference for premium home gym ecosystems integrated with digital coaching.

Europe

Europe accounts for approximately 27% of global revenue, led by Germany, the United Kingdom, and France. Growth in this region is driven by compact urban housing structures, sustainability-conscious consumers, and strong demand for aesthetically integrated furniture. Western European consumers prioritize durable, eco-certified materials, encouraging the adoption of engineered wood and recyclable metal frames. Government-backed energy-efficient housing projects and rising renovation activity further support regional demand. The leading growth driver in Europe is the intersection of minimalist interior design trends and space-saving multifunctional furniture adoption.

Asia-Pacific

Asia-Pacific represents roughly 24% of the global market and is the fastest-growing region, expanding at nearly 13% CAGR. China and Japan dominate regional revenue due to dense urban populations and smaller average apartment sizes. Rising middle-class income levels in China and India are accelerating the adoption of premium home wellness solutions. In Japan, aging demographics are driving demand for rehabilitation-focused modular systems. India is emerging as a high-growth market due to expanding urban housing projects and increasing health awareness among younger populations. The primary driver across APAC is rapid urbanization combined with shrinking residential floor space.

Middle East & Africa

This region accounts for approximately 8% of global demand, led by the UAE and Saudi Arabia. Growth is primarily driven by luxury residential developments, smart city projects, and large-scale hospitality investments. High-income consumer segments in the Gulf Cooperation Council (GCC) countries are increasingly investing in premium home interiors that incorporate wellness features. Government-led infrastructure initiatives and tourism diversification strategies are indirectly boosting modular fitness installations in residential and hospitality projects.

Latin America

Latin America contributes around 7% of global revenue, with Brazil and Mexico as leading markets. Urban upper-middle-class consumers are driving demand, particularly in high-rise residential developments. Increasing health awareness and the gradual growth of e-commerce channels are supporting regional expansion. However, price sensitivity remains relatively higher compared to North America and Europe, leading to stronger demand for mid-range modular systems. The key regional growth driver is the expansion of urban housing combined with rising interest in home-based fitness solutions.

Key Players in the Modular Fitness Furniture Market

- Peloton Interactive

- Tonal Systems

- Technogym

- Johnson Health Tech

- Life Fitness

- NordicTrack

- BowFlex

- PRX Performance

- Tempo Fitness

- Rogue Fitness

- Precor

- Hydrow

- Echelon Fitness

- IKEA

- Lululemon