Mobile Phone Holder Market Size

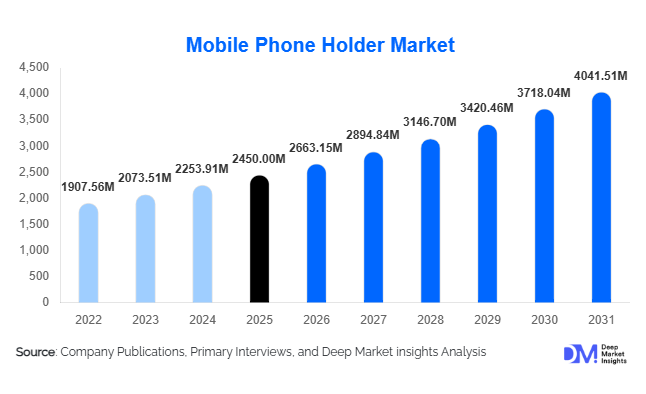

According to Deep Market Insights, the global mobile phone holder market size was valued at USD 2,450 million in 2025 and is projected to grow from USD 2,663.15 million in 2026 to reach USD 4,041.51 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The market growth is primarily driven by the increasing adoption of smartphones, rising demand for hands-free device usage, and expanding applications across automotive, residential, and commercial sectors. Additionally, growing safety regulations regarding mobile usage while driving and the integration of advanced features such as wireless charging and magnetic mounting systems are further accelerating demand.

Key Market Insights

- Car mount holders dominate the market, driven by rising navigation usage and strict hands-free driving regulations globally.

- Online retail channels account for over half of total sales, supported by strong e-commerce penetration and competitive pricing strategies.

- Asia-Pacific leads the global market, supported by high smartphone penetration and large-scale manufacturing ecosystems.

- Mid-range products are the most preferred, offering a balance between affordability and durability.

- Wireless charging-enabled holders are gaining traction, especially in premium automotive and desk applications.

- Growing demand from gig economy workers, including ride-hailing and delivery drivers, is driving consistent volume growth.

What are the latest trends in the mobile phone holder market?

Integration of Wireless Charging and Smart Features

The integration of wireless charging technology into mobile phone holders is emerging as a key trend. Consumers increasingly prefer multi-functional products that combine device mounting with charging capabilities, particularly in automotive environments. Qi-enabled holders, fast-charging compatibility, and intelligent alignment systems are enhancing product appeal. Manufacturers are focusing on heat management, safety certifications, and compatibility with a wide range of devices. This trend is particularly prominent in developed markets, where consumers are willing to pay a premium for convenience and advanced functionality.

Shift Toward Premium and Aesthetic Designs

There is a growing shift toward premiumization, with consumers seeking aesthetically appealing and durable products. Metal-based and hybrid material holders are gaining popularity over traditional plastic variants. Sleek designs, foldable structures, and compact portability are becoming important differentiators. Brands are investing in ergonomic designs that complement modern interiors, particularly in automotive and workspace settings. This trend is also supported by rising disposable incomes and increased consumer awareness of product quality.

What are the key drivers in the mobile phone holder market?

Rising Smartphone Penetration and Usage

The exponential growth in smartphone adoption globally is a primary driver of the mobile phone holder market. With billions of users relying on smartphones for navigation, communication, and entertainment, the need for convenient and secure device placement solutions has increased significantly. This demand is particularly strong in urban areas where mobile usage is integral to daily activities.

Stringent Road Safety Regulations

Governments across multiple regions have implemented strict regulations to limit handheld phone usage while driving. These regulations have significantly boosted demand for car-mounted phone holders as a compliance solution. The enforcement of such laws in North America, Europe, and parts of Asia continues to drive consistent growth in this segment.

Expansion of the Gig Economy and Logistics Services

The rapid growth of ride-hailing, food delivery, and logistics services has created sustained demand for durable and reliable phone holders. Drivers depend on navigation and communication tools, making holders an essential accessory. Bulk procurement by fleet operators further contributes to market expansion.

What are the restraints for the global market?

High Price Sensitivity in Emerging Markets

In price-sensitive regions, consumers often opt for low-cost alternatives, limiting the adoption of premium products. This restricts revenue growth and creates challenges for manufacturers aiming to introduce advanced features.

Market Fragmentation and Intense Competition

The presence of numerous small and unorganized manufacturers leads to intense price competition and reduced brand differentiation. Low-quality and counterfeit products further impact consumer trust and overall market value.

What are the key opportunities in the mobile phone holder industry?

Expansion in Emerging Economies

Emerging markets such as India, Indonesia, and Brazil present significant growth opportunities due to rising smartphone adoption and increasing disposable incomes. Government initiatives supporting local manufacturing are further enabling market expansion.

Growth of Multi-Functional and Smart Holders

The demand for holders integrated with wireless charging, magnetic alignment, and smart connectivity features is growing rapidly. Companies investing in such innovations can tap into high-margin segments and differentiate their offerings.

Rising Demand from Commercial and Fleet Applications

The increasing adoption of mobile holders in commercial applications, including logistics and transportation, presents strong growth potential. Customized solutions for fleet operators and heavy-duty applications are expected to drive future demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2450 Million |

| Market Size in 2026 | USD 2663.15 Million |

| Market Size in 2031 | USD 4041.51 Million |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Car mount holders continue to dominate the mobile phone holder market, accounting for approximately 38% of the total market share in 2025. This leadership is primarily driven by the rapid increase in global vehicle ownership, coupled with the growing reliance on smartphones for navigation, ride-hailing, and real-time communication. Regulatory mandates across key markets that restrict handheld phone usage while driving have further accelerated adoption, making car mounts a necessity rather than an optional accessory. Within this category, air vent and dashboard mounts are particularly popular due to ease of installation and compatibility with various vehicle types.

Desk and tabletop holders are witnessing steady growth, supported by the proliferation of remote work, online education, and digital content consumption. These holders are increasingly used for video conferencing, streaming, and multitasking, especially in home-office environments. Meanwhile, magnetic holders are gaining traction due to their minimalist design, ease of use, and quick mounting capabilities, appealing to urban consumers seeking convenience. Additionally, wireless charging holders are emerging as a high-growth premium segment, driven by increasing adoption of Qi-enabled smartphones and consumer preference for clutter-free charging solutions. This segment is expected to see above-average growth due to continuous innovation in fast-charging and smart alignment technologies.

Application Insights

The automotive segment remains the largest end-use category, contributing approximately 48% of the total market share in 2025. Its dominance is driven by a combination of regulatory enforcement, increased commuting times, and the widespread use of navigation and ride-hailing applications. The expansion of the gig economy, particularly in food delivery and logistics services, has further strengthened demand for durable and reliable holders designed for long hours of usage.

Residential applications are expanding steadily, fueled by lifestyle shifts toward remote working, online meetings, and content streaming. Consumers are increasingly adopting holders for ergonomic convenience and improved productivity. The commercial segment is among the fastest-growing, with logistics companies, fleet operators, and service providers integrating phone holders into daily operations to enhance efficiency and safety. Additionally, outdoor and sports applications, including cycling and motorcycling, are emerging as niche yet high-potential segments. These applications demand rugged, vibration-resistant designs, creating opportunities for specialized product innovation and premium pricing.

Distribution Channel Insights

Online retail channels dominate the market, accounting for approximately 52% of total sales in 2025. This dominance is driven by the rapid growth of e-commerce platforms, increasing smartphone-based shopping, and the availability of a wide range of products at competitive prices. Consumers benefit from easy price comparisons, product reviews, and direct-to-consumer (D2C) purchasing options, which have significantly improved transparency and accessibility.

Offline channels, including electronics stores, automotive accessory outlets, and large-format retail stores, continue to play an important role, particularly in emerging markets where consumers prefer physical product evaluation before purchase. These channels also benefit from impulse buying and localized distribution networks. The growing influence of digital marketing, influencer endorsements, and user-generated reviews is further strengthening online sales, while omnichannel strategies are being adopted by leading brands to maximize market reach.

Price Range Insights

Mid-range products priced between USD 10 and 25 account for approximately 41% of the global market share, making them the leading price segment. This dominance is driven by their ability to offer a balance between affordability, durability, and functionality. Consumers in both developed and emerging markets increasingly prefer products that deliver reliable performance without entering premium price brackets.

Low-cost products dominate volume sales in price-sensitive regions such as Asia-Pacific, Latin America, and parts of Africa, where affordability is a key purchasing factor. However, these products often face challenges related to durability and brand trust. On the other hand, premium products are gaining traction in developed markets, supported by rising disposable incomes and demand for advanced features such as wireless charging, premium materials, and enhanced aesthetics. The gradual shift toward premiumization is expected to improve overall market value despite price competition in lower segments.

Explore more data points, trends and opportunities Download Free Sample Report

Mobile Phone Holder Market Segmentations

By Product Type

- Car Mount Holders

- Bike & Motorcycle Mounts

- Desk/Tabletop Holders

- Magnetic Holders

- Wireless Charging Holders

- Ring Holders & Grip Stands

- Tripod & Professional Mounts

By Application

- Automotive

- Residential/Personal Use

- Commercial

- Outdoor & Sports

By Distribution Channel

- Online Retail

- Electronics & Specialty Stores

- Automotive Accessory Shops

- Supermarkets/Hypermarkets

By Price Range

- Low (Below USD 10)

- Mid-Range (USD 10–25)

- Premium (Above USD 25)

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global mobile phone holder market, accounting for approximately 42% in 2025. The region’s dominance is driven by high smartphone penetration, a strong manufacturing ecosystem, and the presence of cost-effective production hubs, particularly in China. China leads both in terms of production and consumption, benefiting from well-established supply chains and export capabilities. India represents the fastest-growing market within the region, supported by rising middle-class income, increasing vehicle ownership, and government initiatives such as “Make in India,” which encourage local manufacturing. Additionally, the rapid expansion of e-commerce platforms and the gig economy across Southeast Asia is further accelerating demand for mobile phone holders.

North America

North America accounts for approximately 25% of the global market share, with the United States being the primary contributor. Growth in this region is driven by stringent road safety regulations that mandate hands-free device usage, along with high consumer awareness and adoption of premium products. The region also benefits from strong purchasing power, advanced retail infrastructure, and high penetration of wireless charging-enabled smartphones. Furthermore, the widespread use of ride-hailing and delivery services has created sustained demand for high-quality, durable holders. The presence of leading brands and continuous product innovation also contributes to regional growth.

Europe

Europe holds around 20% of the global market share, with key markets including Germany, the UK, and France. Growth in this region is driven by strict regulatory frameworks promoting road safety, along with a strong automotive culture. European consumers tend to prioritize product quality, durability, and sustainability, leading to higher demand for premium and eco-friendly mobile phone holders. Additionally, the region’s well-developed automotive industry and increasing adoption of electric vehicles are creating new opportunities for integrated and advanced mounting solutions.

Latin America

Latin America is an emerging market, led by Brazil and Mexico, with increasing demand driven by rising smartphone adoption and expanding automotive sectors. Growth in the region is supported by urbanization, improving internet connectivity, and the gradual expansion of e-commerce platforms. However, price sensitivity remains a key challenge, influencing consumer preference toward low-cost products. Despite this, the growing gig economy and increasing awareness of road safety are expected to drive steady market expansion over the forecast period.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, with key markets including the UAE and South Africa. Rising urbanization, increasing vehicle ownership, and improving retail infrastructure are major drivers of demand. In the Middle East, high disposable incomes and a preference for premium products are supporting growth in advanced and aesthetically designed holders. In Africa, expanding smartphone penetration and improving distribution networks are contributing to gradual market development. Additionally, infrastructure development and increasing adoption of digital services are expected to further boost demand in the coming years.

Key Players in the Mobile Phone Holder Market

- Belkin International

- Scosche Industries

- iOttie Inc.

- RAM Mounts

- Spigen Inc.

- Baseus

- Anker Innovations

- Aukey

- Xiaomi

- Samsung Electronics

- Logitech

- Nite Ize

- WizGear

- Lamicall

- ESR Gear