Mixer Grinder Market Size

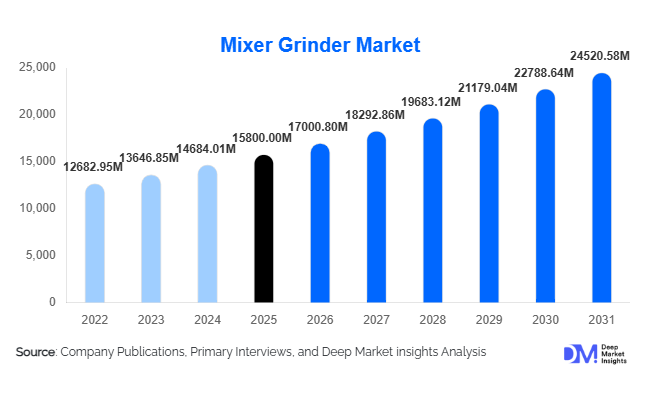

According to Deep Market Insights, the global mixer grinder market size was valued at USD 15,800 million in 2025 and is projected to grow from USD 17,000.80 million in 2026 to reach USD 24,520.58 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The mixer grinder market growth is primarily driven by rising urbanization, increasing disposable income, and the growing demand for convenient and time-saving kitchen appliances across both developed and emerging economies.

Key Market Insights

- Household demand dominates the market, accounting for nearly 70% of global consumption, driven by daily cooking requirements in the Asia-Pacific.

- Mid-range mixer grinders are the most preferred segment, balancing affordability with functionality and capturing a significant share of global sales.

- Asia-Pacific leads the global market, supported by strong demand from India and China due to traditional cooking practices.

- Online distribution channels are rapidly expanding, growing at a faster rate than offline retail due to e-commerce penetration.

- Technological advancements, including smart and IoT-enabled appliances, are gaining traction in developed markets.

- Foodservice industry demand is accelerating, driven by the growth of restaurants, cloud kitchens, and catering businesses globally.

What are the latest trends in the mixer grinder market?

Shift Toward Multi-functional Appliances

Consumers are increasingly opting for multi-functional mixer grinders that combine blending, grinding, chopping, and juicing capabilities. This trend is driven by the need to optimize kitchen space and enhance efficiency. Manufacturers are introducing all-in-one appliances with interchangeable jars and advanced blade technologies, reducing the need for multiple devices. This shift is particularly prominent in urban households where compact and versatile appliances are preferred. The trend is also influencing product design, with brands focusing on ergonomic builds, easy maintenance, and enhanced durability to cater to evolving consumer expectations.

Smart and Energy-Efficient Innovations

The integration of smart technologies is transforming the mixer grinder landscape. IoT-enabled appliances with programmable settings, app connectivity, and automated controls are emerging in premium segments. Additionally, energy-efficient motors and noise reduction technologies are gaining importance, particularly in developed markets where sustainability and user comfort are key considerations. Manufacturers are investing in R&D to develop eco-friendly products with lower power consumption and extended lifespan, aligning with global energy efficiency standards and environmental regulations.

What are the key drivers in the mixer grinder market?

Rising Urbanization and Changing Lifestyles

Rapid urbanization has significantly increased the adoption of modern kitchen appliances. Busy lifestyles and time constraints are pushing consumers toward efficient cooking solutions, making mixer grinders an essential household tool. Urban households are increasingly prioritizing convenience, leading to higher demand for automated appliances that simplify food preparation processes.

Growth in Disposable Income

Increasing disposable incomes, particularly in emerging economies, are enabling consumers to invest in durable and high-quality appliances. The transition from manual cooking methods to electric appliances is accelerating, supported by improved purchasing power and changing consumption patterns. This trend is further driving demand for premium and mid-range mixer grinders.

What are the restraints for the global market?

Price Sensitivity in Developing Markets

Despite growing demand, price sensitivity remains a key challenge in low- and middle-income regions. Consumers often opt for lower-cost alternatives, limiting the penetration of premium products. This creates pressure on manufacturers to balance affordability with quality while maintaining profitability.

Durability and Maintenance Concerns

Frequent breakdowns and maintenance issues, particularly in low-cost products, can impact consumer trust. The presence of unorganized manufacturers offering substandard products further exacerbates this issue, posing a challenge for established brands aiming to maintain quality standards and customer satisfaction.

What are the key opportunities in the mixer grinder industry?

Expansion in Emerging Economies

Emerging markets such as India, Indonesia, and African countries offer significant growth opportunities due to rising electrification, urbanization, and increasing awareness of modern appliances. Rural penetration remains relatively low, providing untapped potential for manufacturers to expand distribution networks and introduce affordable product variants tailored to local needs.

Smart Appliance Integration

The adoption of smart kitchen appliances presents a major opportunity for innovation. IoT-enabled mixer grinders with automated settings, voice control, and recipe integration can attract tech-savvy consumers. This segment allows companies to differentiate their offerings and command premium pricing, particularly in developed markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15800 Million |

| Market Size in 2026 | USD 17000.80 Million |

| Market Size in 2031 | USD 24520.58 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Stand mixer grinders dominate the global market, accounting for approximately 52% of total revenue in 2025. Their leadership is primarily driven by their multi-functionality, durability, and adaptability to diverse cooking requirements, especially in high-usage markets across the Asia-Pacific. These appliances typically come with multiple jar configurations and varying motor capacities, enabling consumers to perform grinding, blending, and mixing operations efficiently. The increasing preference for all-in-one kitchen appliances and replacement demand for older units further strengthen this segment’s dominance.

Portable and compact mixer grinders are gaining traction, particularly among urban consumers, nuclear families, and millennials, due to their lightweight design, space efficiency, and ease of storage. This segment is benefiting from rising urbanization and shrinking kitchen spaces globally. Meanwhile, commercial heavy-duty mixer grinders, though smaller in overall share, are witnessing robust growth driven by the expansion of the foodservice industry, cloud kitchens, and catering businesses. Their high-capacity motors and continuous usage capability make them essential for bulk food preparation, positioning this segment as the fastest-growing within product categories.

Application Insights

Household applications lead the market with nearly 68% share in 2025, supported by the indispensable role of mixer grinders in daily cooking routines, particularly in emerging economies where fresh ingredient preparation is common. Rising electrification, increasing disposable income, and growing awareness of modern kitchen appliances are key drivers for this segment. Additionally, post-pandemic behavioral shifts toward home cooking have reinforced long-term demand.

Commercial applications, including restaurants, cafes, quick-service restaurants (QSRs), and catering services, are expanding at a faster pace, driven by the global growth of the foodservice sector. The proliferation of cloud kitchens and food delivery platforms has significantly increased the need for efficient food preparation equipment. Food processing units represent a niche yet steadily growing segment, particularly in developing regions, where small-scale food manufacturing and local processing activities are increasing, contributing to incremental demand.

Distribution Channel Insights

Offline retail channels, including supermarkets, hypermarkets, and specialty appliance stores, account for around 60% of market share, primarily due to consumer preference for physical product inspection, brand trust, and immediate purchase. In many developing markets, offline channels also benefit from strong dealer networks and localized distribution.

However, online retail is the fastest-growing distribution channel, driven by increasing internet penetration, smartphone usage, and the convenience of home delivery. E-commerce platforms offer competitive pricing, wider product selection, and customer reviews, which influence purchase decisions. Additionally, brand-owned websites and direct-to-consumer (D2C) models are gaining importance as manufacturers seek higher margins and stronger customer engagement. Promotional campaigns, festive discounts, and financing options are further accelerating online adoption.

Price Range Insights

The mid-range segment (USD 50–120) dominates the market, capturing approximately 47% share, driven by its optimal balance between affordability, performance, and durability. This segment caters to the largest consumer base, particularly in emerging economies, where consumers seek value-for-money products with reliable performance.

The economy segment continues to serve price-sensitive consumers in rural and semi-urban markets, where affordability is a key purchasing factor. Meanwhile, the premium segment is gaining traction in developed regions due to rising demand for advanced features such as smart connectivity, noise reduction, energy efficiency, and premium aesthetics. Premiumization is further supported by increasing consumer willingness to invest in long-lasting and technologically advanced appliances.

End-Use Insights

Household consumers represent the largest end-use segment, accounting for around 70% of total demand. This dominance is driven by daily usage frequency, replacement cycles, and rising penetration in developing regions. The increasing number of nuclear families and urban households is further strengthening demand in this segment.

The foodservice industry is the fastest-growing end-use segment, supported by the rapid expansion of restaurants, QSR chains, and cloud kitchens globally. The need for operational efficiency, consistency in food preparation, and scalability is driving the adoption of high-performance mixer grinders. Small-scale food manufacturing units are also emerging as a key demand contributor, particularly in emerging markets where local food production and entrepreneurship are expanding. This segment is benefiting from government support for small businesses and food processing industries.

Explore more data points, trends and opportunities Download Free Sample Report

Mixer Grinder Market Segmentations

By Product Type

- Stand Mixer Grinders

- Portable/Compact Mixer Grinders

- Commercial/Heavy-Duty Mixer Grinders

By Application

- Household/Residential Use

- Restaurants & Cafés

- Catering Services

- Food Processing Units

By Distribution Channel

- Online Retail

- Supermarkets/Hypermarkets

- Specialty Appliance Stores

- Brand-Owned Stores

By Price Range

- Economy Segment (< USD 50)

- Mid-Range Segment (USD 50–120)

- Premium Segment (> USD 120)

By End-Use

- Household Consumers

- Foodservice Industry

- Small Food Manufacturing Units

Regional Insights

Asia-Pacific

Asia-Pacific dominates the mixer grinder market with approximately 45% share in 2025, making it the largest and most influential regional market. India and China are the primary contributors, with India alone accounting for nearly 18% of global demand. The region’s dominance is driven by strong cultural dependence on fresh food preparation, high frequency of usage, and widespread adoption of mixer grinders as essential kitchen appliances.

Key growth drivers include rapid urbanization, rising disposable incomes, an expanding middle-class population, and increasing electrification in rural areas. Additionally, strong domestic manufacturing capabilities and government initiatives such as “Make in India” are supporting production and affordability. The expansion of e-commerce and retail networks is further improving product accessibility, particularly in tier-2 and tier-3 cities.

North America

North America holds around 15% of the global market, led by the United States. The region is characterized by high adoption of premium and technologically advanced appliances. Demand is driven by increasing consumer preference for smart kitchen solutions, convenience, and energy-efficient products. Growth in this region is supported by rising interest in healthy cooking, home meal preparation, and multifunctional appliances. The presence of established brands, strong distribution channels, and high replacement demand further contributes to market stability. Additionally, the growing popularity of international cuisines requiring blending and grinding is indirectly boosting demand.

Europe

Europe accounts for approximately 18% of the global market, with Germany, the UK, and France as major contributors. The region is driven by demand for high-quality, durable, and energy-efficient appliances, aligned with stringent regulatory standards. Key growth drivers include increasing focus on sustainability, energy efficiency regulations, and rising consumer awareness of eco-friendly products. Additionally, the growing popularity of home cooking and diverse culinary practices is supporting demand. Premiumization trends are strong in Europe, with consumers willing to pay for advanced features and superior build quality.

Middle East & Africa

The Middle East & Africa region holds about 10% market share, with steady growth driven by urbanization, rising disposable income, and increasing adoption of modern kitchen appliances. Countries such as the UAE and South Africa are key markets. Growth drivers include increasing dependence on imported appliances, expansion of retail infrastructure, and rising expatriate population, which influences demand for diverse cooking appliances. Additionally, improving electrification and infrastructure development in African countries is creating new growth opportunities. The region also benefits from strong import flows from Asia-Pacific manufacturing hubs.

Latin America

Latin America contributes around 12% of the global market, led by Brazil and Mexico. The region is experiencing steady growth due to improving economic conditions, urbanization, and rising adoption of modern kitchen appliances. Key drivers include the expansion of the middle-class population, increasing retail penetration, and growing awareness of convenience-driven cooking solutions. Additionally, the rise of small food businesses and local food processing activities is supporting demand. While price sensitivity remains a challenge, the market is gradually shifting toward mid-range and durable products, indicating long-term growth potential.