Minimalist Window System Market Size

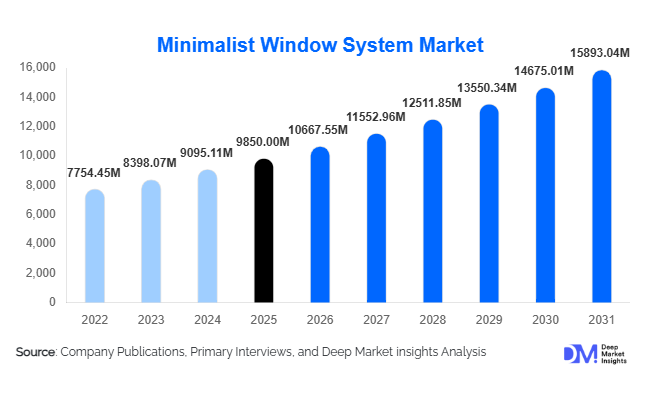

According to Deep Market Insights, the global minimalist window system market size was valued at USD 9,850 million in 2025 and is projected to grow from USD 10,667.55 million in 2026 to reach USD 15,893.04 million by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The minimalist window system market growth is primarily driven by the rising demand for modern architectural aesthetics, increasing adoption of energy-efficient building solutions, and growing investments in luxury residential and commercial infrastructure worldwide.

Key Market Insights

- Minimalist window systems are gaining traction due to their ultra-slim profiles and large glass surfaces, enhancing natural lighting and indoor-outdoor connectivity.

- Aluminum-based systems dominate the market, supported by durability, recyclability, and the ability to support expansive glazing.

- Europe leads the global market, driven by stringent energy efficiency regulations and mature construction practices.

- Asia-Pacific is the fastest-growing region, fueled by rapid urbanization and increasing demand for premium housing in China and India.

- Smart and automated window systems are emerging rapidly, integrating IoT and home automation technologies.

- New construction projects account for the majority of demand, as minimalist systems are easier to integrate during the design phase.

What are the latest trends in the minimalist window system market?

Integration of Smart and Automated Window Systems

Technological advancements are transforming the minimalist window system market, with increasing adoption of motorized and IoT-enabled systems. Smart windows can be controlled remotely, integrated with home automation platforms, and programmed for climate responsiveness. Features such as automatic shading, sensor-based opening/closing, and electrochromic glass are gaining traction among tech-savvy consumers. These innovations not only enhance convenience but also contribute to energy efficiency, making them highly attractive in modern smart homes and commercial buildings.

Shift Toward Sustainable and Energy-Efficient Glazing

Sustainability is becoming a central focus in construction, driving demand for energy-efficient glazing solutions such as double and triple-glazing, as well as Low-E coatings. Minimalist window systems are increasingly designed to meet stringent energy codes, particularly in Europe and North America. Manufacturers are also focusing on recyclable materials like aluminum and incorporating thermal break technologies to improve insulation. This trend aligns with global green building certifications and growing consumer awareness around environmental impact.

What are the key drivers in the minimalist window system market?

Rising Demand for Modern Architectural Design

Contemporary architecture emphasizes clean lines, openness, and transparency, driving demand for minimalist window systems. Large glass panels with slim frames enhance aesthetics and create seamless indoor-outdoor transitions, making them highly desirable in both residential and commercial projects. Architects and developers increasingly prefer these systems to achieve modern design goals.

Stringent Energy Efficiency Regulations

Governments worldwide are implementing strict building energy codes, pushing the adoption of high-performance window systems. Minimalist windows with advanced glazing technologies help reduce heat loss and improve energy efficiency, making them essential for compliance. This is particularly significant in Europe, where sustainability standards are highly enforced.

Growth in Urbanization and Premium Housing

Rapid urbanization and rising disposable incomes, especially in the Asia-Pacific, are boosting demand for premium housing. Consumers are increasingly investing in high-end features such as minimalist windows to enhance property value and living standards. This trend is accelerating market growth across emerging economies.

What are the restraints for the global market?

High Initial Cost of Installation

Minimalist window systems are significantly more expensive than traditional windows due to advanced materials, precision engineering, and specialized installation. This limits adoption in cost-sensitive markets and restricts penetration beyond premium segments.

Complex Installation and Maintenance

These systems require skilled labor and precise installation, increasing project timelines and costs. Maintenance of large glass panels and automated components can also be challenging, which may deter some end users and developers.

What are the key opportunities in the minimalist window system industry?

Expansion in Luxury Residential Markets

Rising wealth in emerging economies is driving demand for luxury housing, creating strong opportunities for minimalist window system manufacturers. High-end villas, condominiums, and gated communities increasingly incorporate these systems as a premium design element, offering significant growth potential.

Growth in Smart Home Integration

The increasing adoption of smart homes presents opportunities for integrating automated and IoT-enabled window systems. Manufacturers can differentiate themselves by offering advanced features such as remote operation, energy optimization, and smart glass technologies, unlocking higher margins and customer value.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9850 Million |

| Market Size in 2026 | USD 10667.55 Million |

| Market Size in 2031 | USD 15893.04 Million |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sliding minimalist window systems continue to dominate the global market, accounting for approximately 42% of the total share in 2025. This leadership position is primarily driven by their superior space optimization, ease of operation, and ability to support large uninterrupted glass panels, which are critical for modern architectural designs. Sliding systems are particularly favored in urban residential apartments and high-end commercial buildings where maximizing usable space and achieving seamless indoor-outdoor transitions are key priorities. The increasing adoption of multi-track and pocket sliding systems in luxury villas and hospitality projects is further strengthening this segment’s growth trajectory.

Fixed minimalist window systems hold a strong position in commercial and institutional applications, especially in office buildings, airports, and retail spaces, where maximizing daylight penetration and energy efficiency is essential. Meanwhile, bi-fold systems are rapidly gaining traction in the premium residential segment, particularly in regions with favorable climates, as they enable complete wall openings and flexible space utilization. The growing demand for panoramic views and open-plan living concepts is expected to further accelerate adoption across these product categories.

Application Insights

The residential segment leads the minimalist window system market, contributing approximately 50% of the global share in 2025. This dominance is driven by rising demand for luxury housing, increasing consumer preference for modern architectural aesthetics, and the growing importance of natural lighting and ventilation in home design. High-net-worth individuals and premium housing developers are key adopters, particularly in urban and suburban regions where property value enhancement is a major consideration.

Commercial applications represent a substantial share, with offices, retail outlets, and hospitality spaces leveraging minimalist window systems to enhance building aesthetics, improve energy efficiency, and create visually appealing environments. The shift toward green buildings and sustainable commercial infrastructure is further supporting demand in this segment. Institutional applications, including airports, hospitals, and educational facilities, are increasingly adopting these systems to improve occupant comfort, reduce energy consumption, and meet regulatory standards. The integration of large glazing surfaces in institutional buildings is also contributing to improved indoor environmental quality.

Installation Type Insights

New construction dominates the market with nearly 65% share in 2025, as minimalist window systems are most effectively integrated during the initial design and construction phase. Architects and developers prefer incorporating these systems in new projects to achieve seamless aesthetics, structural compatibility, and optimal energy performance. The global boom in residential and commercial construction, particularly in the Asia-Pacific and the Middle East, is significantly driving this segment.

Retrofit and replacement installations are witnessing steady growth, especially in mature markets such as Europe and North America. Aging building infrastructure, combined with stringent energy efficiency regulations, is encouraging property owners to upgrade traditional window systems with high-performance minimalist alternatives. Government incentives for energy-efficient renovations and increasing awareness of sustainability benefits are further supporting this segment’s expansion.

Material Insights

Aluminum frames dominate the minimalist window system market, accounting for approximately 55% of the total share in 2025. This leadership is driven by aluminum’s high strength-to-weight ratio, corrosion resistance, and ability to support ultra-slim profiles without compromising structural integrity. Additionally, aluminum’s recyclability aligns with global sustainability goals, making it a preferred choice among environmentally conscious developers and architects.

uPVC and composite materials are gaining traction, particularly in mid-range residential applications, where cost-effectiveness and thermal insulation are key considerations. Composite frames, combining materials such as aluminum and wood or uPVC, are increasingly being adopted to achieve a balance between performance, aesthetics, and affordability. These materials are expected to witness higher growth rates as manufacturers focus on expanding their offerings to cater to a broader customer base.

Explore more data points, trends and opportunities Download Free Sample Report

Minimalist Window System Market Segmentations

By Product Type

- Sliding Minimalist Window Systems

- Fixed Minimalist Window Systems

- Casement Minimalist Window Systems

- Tilt & Turn Window Systems

- Bi-fold Minimalist Window Systems

By Application

- Residential

- Commercial

- Institutional

By Installation Type

- New Construction

- Retrofit / Replacement

By Material

- Aluminum Frames

- uPVC Frames

- Steel Frames

- Composite Frames

Regional Insights

Europe

Europe remains the largest market, accounting for approximately 34% of the global share in 2025, with strong demand in Germany, Italy, France, and the UK. The region’s leadership is primarily driven by stringent energy efficiency regulations, such as the Nearly Zero-Energy Building (NZEB) standards, which mandate the use of high-performance building materials, including advanced window systems. Germany stands out as a key contributor due to its robust construction sector, strong manufacturing base, and high adoption of sustainable building practices. Additionally, the region’s mature architectural industry and preference for minimalist design aesthetics continue to drive steady demand. Retrofit activity is particularly strong in Western Europe, where aging infrastructure is being upgraded to meet modern energy standards.

Asia-Pacific

Asia-Pacific accounts for approximately 30% of the global market and is the fastest-growing region, with a CAGR exceeding 9%. China dominates regional demand due to its massive construction industry and large-scale urban development projects. India is emerging as a high-growth market, driven by rapid urbanization, increasing disposable incomes, and government initiatives promoting housing and infrastructure development. Southeast Asian countries such as Indonesia, Vietnam, and Thailand are also witnessing rising adoption due to expanding middle-class populations and growing investments in commercial real estate. The increasing preference for premium housing and modern architectural designs is a key driver across the region.

North America

North America holds around 22% share, led by the United States, followed by Canada. The region’s growth is driven by strong demand for high-end residential construction, increasing renovation and retrofit activities, and the adoption of energy-efficient building solutions. Stringent building codes and sustainability certifications such as LEED are encouraging the use of advanced window systems. Additionally, the rising popularity of smart homes and automated building technologies is supporting the adoption of motorized and IoT-enabled minimalist window systems across the region.

Middle East & Africa

The Middle East is experiencing significant growth, particularly in the UAE, Saudi Arabia, and Qatar, driven by large-scale luxury real estate developments and mega infrastructure projects such as smart cities and tourism-focused developments. The region’s hot climate also necessitates high-performance glazing solutions, boosting demand for energy-efficient minimalist window systems. In Africa, growth is moderate but steadily increasing, supported by urbanization, infrastructure development, and rising investments in commercial construction in countries such as South Africa, Nigeria, and Kenya.

Latin America

Latin America accounts for nearly 6% of the global market, with Brazil and Mexico leading adoption. Growth in the region is driven by the gradual modernization of construction practices, increasing urbanization, and rising demand for premium building materials in high-end residential and commercial projects. Government initiatives to improve infrastructure and growing foreign investments in real estate are also contributing to market expansion. However, cost sensitivity remains a challenge, leading to higher adoption of mid-range minimalist window solutions.