Mini PCs Market Size

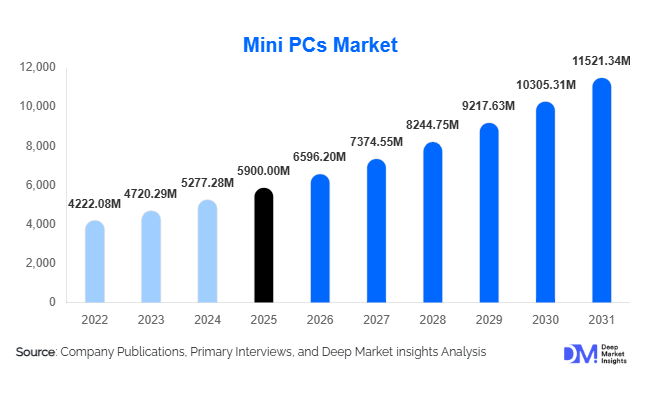

According to Deep Market Insights,the global mini PCs market size was valued at USD 5,900 million in 2025 and is projected to grow from USD 6,596.20 million in 2026 to reach USD 11,521.34 million by 2031, expanding at a CAGR of 11.8% during the forecast period (2026–2031). The market growth is primarily driven by the increasing adoption of compact computing solutions, rising demand for space-efficient enterprise workstations, the proliferation of digital signage networks, and expanding edge computing infrastructure across various industries worldwide.

Key Market Insights

- Mini PCs are increasingly being adopted for edge computing and IoT applications, enabling real-time data processing and low-latency operations in industrial, retail, and smart city environments.

- Ultra-compact mini PCs and stick PCs are gaining traction in corporate and home office setups due to their space-saving design, low energy consumption, and high performance relative to size.

- Asia Pacific dominates the mini PCs market, with China, Japan, South Korea, and India driving demand through electronics manufacturing growth and digitalization initiatives.

- North America remains a major market, fueled by enterprise adoption, digital signage deployment, and edge computing applications across the U.S. and Canada.

- Technological innovation such as AI-enabled mini PCs, ARM-based architectures, and multi-display support is enhancing the product value proposition for corporate, industrial, and retail segments.

What are the latest trends in the mini PCs market?

Rise of Edge Computing and Industrial Deployment

Mini PCs are increasingly being deployed as edge devices in industrial automation, smart retail, and IoT ecosystems. Compact form factors, low power consumption, and adequate processing performance allow mini PCs to act as local nodes for real-time data analytics, machine learning inference, and monitoring tasks. This trend has been accelerated by the need to reduce latency, bandwidth dependency, and operational costs associated with centralized cloud computing.

Expansion in Digital Signage and Retail Applications

Digital signage adoption is growing globally, driving demand for mini PCs as media players capable of handling high-resolution content, multiple displays, and networked management. Retailers are increasingly replacing traditional signage with dynamic content solutions, leveraging mini PCs for flexible deployment and low-maintenance operation. Emerging markets in Asia and Latin America are witnessing strong demand for affordable mini PCs to support digital transformation in retail.

Technological Integration and ARM-Based Systems

Mini PCs are embracing technological innovations, including ARM-based processors, AI accelerators, Thunderbolt connectivity, and multi-display graphics support. ARM-based mini PCs, such as Apple’s M-series, offer energy-efficient solutions for both consumer and enterprise applications. Manufacturers are also integrating fanless designs for silent operation, modular upgrades, and enterprise-grade security, enhancing adoption across sensitive office and industrial environments.

What are the key drivers in the mini PCs market?

Demand for Compact and Energy-Efficient Computing

Organizations and consumers increasingly prioritize devices that occupy minimal space while reducing energy consumption. Mini PCs provide full desktop computing capabilities with lower power requirements, which drives adoption in offices, educational institutions, and home environments. This demand aligns with global sustainability initiatives and corporate green IT strategies.

Growth of Corporate Workstations and Home Office Solutions

The transition toward open-office layouts and hybrid work models has boosted the adoption of mini PCs as space-saving and aesthetically appealing alternatives to traditional desktops. Mini PCs can be mounted behind monitors or integrated into workstations, offering a clutter-free workspace while supporting enterprise-level security and performance needs. This trend has accelerated in North America and Europe, where office space optimization is critical.

Expansion of Digital Signage and Smart Retail

Retailers worldwide are leveraging mini PCs for digital signage and point-of-sale applications. These devices enable dynamic content delivery, remote management, and high-resolution support. The global push toward smart retail and interactive customer experiences has been a strong driver for mini PCs, especially in Asia Pacific, where large retail chains are rapidly digitalizing their operations.

What are the restraints for the global mini PCs market?

Limited Upgradeability

Many mini PCs offer limited hardware upgrade options, with soldered memory and storage components restricting customization. Enterprises and power users who require scalable computing solutions may opt for traditional desktops or tower PCs, limiting broader adoption in performance-critical environments.

Thermal Constraints for High-Performance Applications

The compact form factor of mini PCs creates challenges in heat dissipation under high workloads. Intensive applications such as 3D rendering, AI processing, and gaming may encounter thermal throttling, limiting the usability of mini PCs in such contexts. Manufacturers are addressing this with fanless and advanced cooling designs, but thermal limitations remain a key restraint.

What are the key opportunities in the mini PCs market?

Edge Computing Expansion

With enterprises investing in edge computing to reduce latency and bandwidth use, mini PCs offer a compact, reliable solution for localized data processing. Industrial automation, smart manufacturing, and IoT deployments are key sectors where edge-enabled mini PCs can create significant value. Manufacturers offering ruggedized devices tailored for harsh industrial environments are positioned to benefit.

Smart Retail and Digital Signage Growth

Global retail digital transformation initiatives are creating demand for mini PCs in interactive signage, kiosks, and POS systems. Emerging markets in Asia Pacific and Latin America present untapped potential for cost-effective mini PC solutions, allowing new entrants and established players to capture growing demand.

Corporate Workspace Optimization

The trend toward minimalist office setups, hybrid work, and hot-desking encourages enterprises to adopt mini PCs for efficient, space-saving computing. Devices that support remote management, multi-display setups, and enterprise-grade security are increasingly sought after, presenting opportunities for vendors with customizable solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5900 Million |

| Market Size in 2026 | USD 6596.20 Million |

| Market Size in 2031 | USD 11521.34 Million |

| CAGR | 11.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The mini PCs market is primarily segmented by processor architecture and device form factor, both of which play a critical role in determining performance, power efficiency, and end-user suitability. Intel processor-based mini PCs currently dominate the market, accounting for approximately 61% of global revenue in 2025. Their strong position is supported by a mature ecosystem, extensive compatibility with enterprise software environments, and long-standing partnerships with OEM manufacturers and enterprise IT departments. Businesses continue to favor Intel-based devices for corporate workstations, commercial deployments, and institutional computing environments due to their reliability, optimized thermal performance, and compatibility with widely used operating systems and security frameworks.

Another key growth driver within the product category is the increasing demand for ultra-compact mini PCs, particularly systems with a volume below one liter. These devices account for nearly 42% of the market and are widely adopted due to their compact footprint, energy-efficient operation, and flexibility in installation. Their small form factor allows them to be mounted behind monitors, integrated into kiosks, or embedded within digital signage displays, making them highly suitable for modern office environments, retail installations, and space-constrained workspaces. As organizations increasingly prioritize space optimization and energy savings, demand for ultra-compact designs continues to accelerate.

At the same time, AMD-powered and ARM-based mini PCs are gaining traction across multiple applications. AMD-based devices are increasingly preferred by consumers and creative professionals due to their strong multi-core processing capabilities and competitive pricing, making them suitable for multitasking, light gaming, and multimedia workloads. Meanwhile, ARM-based mini PCs are emerging as a fast-growing category due to their superior power efficiency and increasing adoption in edge computing, AI inference, and low-power enterprise deployments. The success of ARM-based processors, including systems inspired by Apple’s M-series architecture, has further accelerated industry interest in energy-efficient computing platforms, particularly for IoT gateways, smart devices, and mobile-oriented computing environments.

Application Insights

Mini PCs are deployed across a wide range of application environments, including corporate offices, digital signage networks, home computing systems, industrial automation platforms, educational institutions, and healthcare facilities. Among these applications, corporate workstation deployments represent the largest segment, accounting for approximately 34% of the global market in 2025. The dominance of this segment is primarily driven by enterprise IT modernization initiatives, which encourage organizations to replace bulky desktop towers with compact, energy-efficient computing devices that offer comparable performance while occupying significantly less workspace.Mini PCs provide organizations with several operational advantages, including lower power consumption, simplified device management, and flexible installation options. Their ability to support virtualization, cloud computing platforms, and remote work environments has further strengthened their adoption in corporate settings. As hybrid work models continue to expand globally, enterprises are increasingly deploying mini PCs in offices, conference rooms, and remote workstations to maintain cost-efficient and scalable computing infrastructure.

Beyond corporate environments, digital signage and retail deployments represent one of the fastest-growing application areas. Retailers, shopping malls, restaurants, transportation hubs, and hospitality venues increasingly rely on mini PCs to power digital displays, interactive kiosks, and advertising networks. Their compact size allows seamless integration into display hardware while providing sufficient processing power to run multimedia content, analytics software, and remote management platforms.Industrial automation is another rapidly expanding application area as industries adopt smart manufacturing technologies and industrial IoT systems. Mini PCs are increasingly deployed in factories and production facilities to support edge computing, real-time monitoring, machine control, and predictive maintenance systems. Their ruggedized designs and ability to operate continuously in demanding environments make them suitable for industrial control systems, robotics integration, and smart logistics management.

Distribution Channel Insights

The mini PCs market is distributed through multiple channels, including direct enterprise procurement, online retail platforms, offline retail stores, and system integrator partnerships. Among these channels, direct enterprise procurement represents the largest revenue contributor, accounting for approximately 37% of global sales. Large corporations, government institutions, and educational organizations typically prefer purchasing mini PCs directly from manufacturers or authorized distributors to secure customized configurations, extended warranties, and large-scale deployment support.Direct procurement agreements also enable organizations to negotiate bulk pricing, integrate specialized hardware configurations, and ensure compatibility with existing enterprise IT infrastructure. These benefits make direct enterprise procurement the preferred channel for corporate workstations, digital signage networks, and institutional computing environments.

Online retail platforms have emerged as a dominant channel for consumer and small business purchases. E-commerce platforms provide buyers with access to a wide range of mini PC models, detailed specifications, and competitive pricing options, making them particularly attractive for home users, freelancers, and small enterprises. The growth of digital marketplaces has significantly improved product accessibility, especially in emerging markets where traditional electronics retail infrastructure may be limited.Offline retail stores continue to serve an important role, particularly for small businesses and first-time buyers who prefer hands-on product demonstrations and in-store technical support. In addition, system integrators are increasingly incorporating mini PCs into broader technology solutions, including IoT networks, surveillance systems, digital signage infrastructure, and smart retail installations. This integration-driven approach has further expanded the addressable market for mini PCs by positioning them as embedded computing components within larger digital ecosystems.

End-User Insights

The mini PCs market serves a diverse range of end users, including corporate enterprises, retail organizations, industrial operators, educational institutions, healthcare providers, and individual consumers. Among these groups, corporate and enterprise users represent the largest segment of demand. The leading driver for this segment is the growing need for compact, cost-efficient computing solutions that support enterprise productivity while reducing energy consumption and office space requirements. Organizations increasingly adopt mini PCs as replacements for traditional desktop computers due to their lower power usage, simplified maintenance, and compatibility with centralized IT management systems.Retail and digital signage applications represent one of the fastest-expanding end-user segments. Retailers are increasingly deploying mini PCs to power interactive displays, customer information kiosks, point-of-sale support systems, and advertising networks. Their compact design allows them to be easily integrated into store fixtures and display units while providing sufficient processing capacity for multimedia content and real-time analytics.

Industrial automation also represents a rapidly emerging opportunity within the mini PCs market. Manufacturing facilities, logistics companies, and industrial operators are increasingly adopting compact computing devices to support edge processing, machine connectivity, and IoT-enabled monitoring systems. Mini PCs can be deployed close to production equipment, enabling real-time data analysis and improving operational efficiency in smart factories.Consumer and home computing applications continue to contribute significantly to market demand, particularly in developing economies where compact and affordable computing devices are gaining popularity. Mini PCs are frequently used as home office computers, media centers, educational devices, and lightweight productivity systems. Their affordability and portability make them an attractive alternative to traditional desktop computers, especially for households seeking cost-effective computing solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Mini PCs Market Segmentations

By Processor Type

- Intel Processor-Based Mini PCs

- AMD Processor-Based Mini PCs

- ARM-Based Mini PCs

By Form Factor

- Ultra-Compact Mini PCs

- Compact Mini PCs

- Modular Mini PCs

- Stick PCs / Compute Sticks

By End-Use Industry

- Consumer / Home Computing

- Corporate & Enterprise

- Education

- Retail & Digital Signage

- Healthcare

- Industrial Automation

- Media & Entertainment

- Government & Defense

By Distribution Channel

- Online Retail

- Direct Sales / Enterprise Procurement

- Offline Retail Stores

- System Integrators & IT Solution Providers

Regional Insights

North America

North America accounted for approximately 27% of the global mini PCs market in 2025, supported by strong technology adoption across the United States and Canada. One of the primary drivers of regional growth is the widespread modernization of corporate IT infrastructure, as organizations increasingly transition toward compact, energy-efficient computing systems. Enterprises across sectors such as finance, healthcare, education, and government are replacing traditional desktop systems with mini PCs to reduce energy consumption and optimize workspace utilization.

Another major factor contributing to market growth in the region is the rapid expansion of digital signage networks across retail stores, transportation hubs, hospitality venues, and entertainment centers. Mini PCs are widely deployed to power advertising displays, interactive kiosks, and customer information systems due to their reliability and small form factor. Additionally, North America is a global leader in edge computing innovation, with technology companies and industrial enterprises investing heavily in decentralized computing architectures. Mini PCs are increasingly used as edge devices for data processing, IoT integration, and AI inference applications, further strengthening their market presence in the region.

Europe

Europe accounted for roughly 24% of the global mini PCs market in 2025, with major demand originating from Germany, the United Kingdom, and France. One of the primary drivers of regional market expansion is the strong adoption of industrial automation technologies across the continent. European manufacturers are actively investing in Industry 4.0 initiatives, integrating connected sensors, robotics systems, and smart factory infrastructure that rely on compact computing platforms such as mini PCs for edge data processing and equipment monitoring.

Corporate digital transformation initiatives are also supporting demand for mini PCs across office environments. Many European companies are redesigning workspaces to be more flexible and space-efficient, which encourages the use of compact computing devices that can be mounted behind displays or integrated into shared workstations. Furthermore, sustainability regulations and energy-efficiency policies implemented by the European Union are encouraging organizations to adopt low-power computing systems. Mini PCs align well with these sustainability goals due to their reduced energy consumption and smaller environmental footprint compared to conventional desktop computers.

Asia Pacific

Asia Pacific represents the largest regional market for mini PCs, accounting for approximately 38% of global demand. Rapid technological development, large-scale electronics manufacturing capabilities, and expanding digital infrastructure are key factors driving growth across the region. Countries such as China, Japan, South Korea, and India play a central role in both the production and consumption of compact computing devices.

China remains a major hub for mini PC manufacturing and component supply chains, enabling cost-effective production and widespread availability of compact computing systems. In Japan and South Korea, demand is driven by advanced consumer electronics markets and the strong presence of technology companies developing innovative computing solutions. Meanwhile, India represents one of the fastest-growing markets in the region due to expanding digitalization initiatives, government technology programs, and increased investment in IT infrastructure.

Rising middle-class populations and improving access to affordable computing devices are also contributing to market expansion across Southeast Asian economies. As small businesses, educational institutions, and households adopt digital technologies at a faster pace, mini PCs are increasingly viewed as an accessible and cost-effective computing solution.

Middle East & Africa

The Middle East and Africa region accounts for approximately 6% of the global mini PCs market, with growth largely driven by digital transformation initiatives across the Gulf Cooperation Council countries. Governments in nations such as the United Arab Emirates and Saudi Arabia are investing heavily in smart city development, public sector digitalization, and advanced infrastructure projects. These initiatives require compact computing solutions to support surveillance systems, information kiosks, and IoT networks, creating significant opportunities for mini PC adoption.

Retail modernization is another important factor contributing to market expansion. Shopping malls, entertainment venues, and hospitality establishments across the region are increasingly deploying digital signage displays and interactive customer engagement systems, many of which rely on mini PCs for processing and content management. In addition, growing investments in education technology and healthcare digitization are further strengthening the demand for compact and energy-efficient computing devices.

Latin America

Latin America holds approximately 5% of the global mini PCs market, with Brazil and Mexico representing the largest national markets in the region. One of the primary drivers of growth is the increasing adoption of digital signage networks across retail stores, transportation hubs, and commercial establishments. Businesses are gradually transitioning from static advertising displays to dynamic digital screens powered by compact computing platforms such as mini PCs.

Enterprise technology upgrades are also contributing to market development across the region. As companies modernize their IT infrastructure and adopt cloud-based applications, there is growing interest in smaller, more energy-efficient computing systems that reduce operational costs while maintaining reliable performance. Although market penetration remains lower compared to North America and Europe, improving internet connectivity, expanding technology investments, and the gradual digital transformation of businesses are expected to support steady growth of the mini PCs market across Latin America.

Key Players in the Global Mini PCs Market

- Intel Corporation

- ASUSTeK Computer Inc.

- HP Inc.

- Dell Technologies

- Lenovo Group Limited

- Acer Inc.

- Apple Inc.

- Gigabyte Technology

- MSI (Micro-Star International)

- Zotac Technology

- ASRock Inc.

- Minisforum

- Beelink

- Huawei Technologies Co., Ltd.

- Shuttle Inc.