Mini Computers Market Size

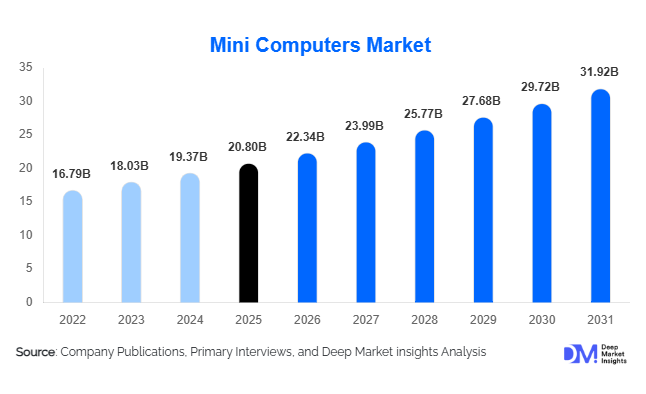

According to Deep Market Insights, the global mini computers market size was valued at USD 20.8 billion in 2025 and is projected to grow from USD 22.34 billion in 2026 to reach USD 31.92 billion by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The mini computers market growth is primarily driven by increasing demand for compact and energy-efficient computing systems, rapid expansion of edge computing infrastructure, rising adoption of Industry 4.0 technologies, and the growing need for AI-enabled localized processing across enterprise and industrial environments.

Key Market Insights

- Mini computers are increasingly replacing traditional desktop towers, particularly across enterprise offices, education, healthcare, and industrial automation environments, due to lower power consumption and compact form factors.

- Edge computing deployment is accelerating global demand, with mini computers being widely adopted as localized processing nodes across telecom, manufacturing, logistics, and smart city ecosystems.

- Asia-Pacific dominates the global mini computers market, supported by strong electronics manufacturing ecosystems in China, Taiwan, South Korea, and Japan.

- Industrial automation applications represent one of the fastest-growing segments, driven by Industry 4.0 adoption, robotics integration, and AI-enabled manufacturing systems.

- AI-enabled mini PCs are emerging rapidly, integrating NPUs, embedded GPUs, and advanced processors for machine learning inference and intelligent edge analytics.

- Online retail and direct-to-consumer channels dominate sales, allowing buyers to customize hardware configurations and compare compact computing solutions more efficiently.

What are the latest trends in the mini-computer market?

AI-Enabled Edge Computing Systems Gaining Momentum

The integration of AI acceleration into compact computing platforms is becoming one of the most significant trends shaping the mini-computers market. Manufacturers are increasingly introducing mini PCs equipped with neural processing units (NPUs), embedded GPUs, and AI accelerators capable of handling localized machine learning inference and real-time analytics. These systems are being adopted across industrial automation, surveillance, robotics, retail analytics, and healthcare diagnostics. Enterprises are shifting AI workloads from centralized cloud infrastructure toward localized edge processing to reduce latency and bandwidth costs. Compact AI-enabled systems are also being deployed in smart factories for predictive maintenance, machine vision, and autonomous operational control. The emergence of AI-ready processors from Intel, AMD, NVIDIA, and ARM-based chipmakers is further accelerating innovation within this segment.

Industrial and Rugged Mini Computers Expanding Across Smart Factories

Industrial-grade mini computers are witnessing strong adoption as manufacturers modernize facilities under Industry 4.0 initiatives. Rugged compact systems capable of operating under extreme temperatures, vibration, and dust exposure are replacing conventional industrial PCs and embedded controllers. These systems support industrial IoT gateways, machine control applications, robotics management, and real-time production analytics. DIN-rail embedded PCs and fanless mini computers are becoming increasingly popular across automotive manufacturing, semiconductor fabrication, energy infrastructure, and logistics automation environments. Demand is also increasing for modular industrial mini computers that allow scalable GPU and storage integration for advanced analytics workloads. Governments globally are supporting smart manufacturing transitions, further strengthening demand for compact industrial computing infrastructure.

What are the key drivers in the mini-computer market?

Growing Adoption of Edge Computing Infrastructure

The rapid expansion of edge computing infrastructure is one of the primary growth drivers for the mini-computers market. Industries including manufacturing, telecommunications, transportation, retail, and healthcare increasingly require real-time localized processing to support low-latency applications. Mini computers provide an ideal solution because of their compact design, energy efficiency, and ability to support AI-enabled workloads. Edge deployment reduces dependence on centralized cloud infrastructure and improves operational responsiveness. Telecom operators are also deploying mini computing systems within 5G infrastructure to process large volumes of distributed network data. This shift toward decentralized computing architecture continues to create strong demand for compact processing systems globally.

Rising Demand for Energy-Efficient Enterprise Computing

Enterprises and public institutions are increasingly prioritizing energy-efficient IT infrastructure as part of sustainability and operational cost reduction strategies. Mini computers consume significantly less electricity compared to traditional desktop towers and entry-level servers, while requiring smaller physical installation spaces. Organizations operating large office environments, educational campuses, and public service facilities are increasingly adopting mini PCs to reduce power consumption and cooling requirements. Sustainability regulations across Europe, North America, and the Asia-Pacific are further supporting the procurement of compact low-power computing systems. Hybrid work adoption and flexible workspace models are also encouraging enterprises to deploy portable and space-efficient computing solutions.

What are the restraints for the global market?

Thermal Management and Performance Limitations

One of the major challenges within the mini-computer market is thermal management. Compact form factors limit airflow and cooling capacity, particularly in high-performance configurations equipped with advanced CPUs and GPUs. Excessive heat generation can impact system reliability, reduce component lifespan, and restrict performance during compute-intensive workloads such as advanced rendering, large-scale simulation, and AI training. Manufacturers continue investing in vapor chamber cooling, advanced heat dissipation materials, and fanless thermal architectures; however, thermal optimization remains a critical engineering challenge within compact systems.

Intense Pricing Competition and Supply Chain Volatility

The market remains highly competitive with strong pricing pressure from regional manufacturers and ODM suppliers, particularly across Asia-Pacific. Aggressive pricing strategies reduce average selling prices and compress profit margins for established OEMs. Semiconductor shortages, fluctuating memory prices, and geopolitical disruptions affecting global electronics supply chains also create operational uncertainty. Manufacturers must balance innovation investments with cost competitiveness while maintaining product quality and performance standards. In lower-priced consumer categories, commoditization continues to intensify competition and reduce differentiation.

What are the key opportunities in the mini computers industry?

Expansion of Smart Cities and Intelligent Infrastructure

Global smart city initiatives present substantial opportunities for mini computer manufacturers. Compact computing systems are increasingly deployed across intelligent transportation systems, surveillance infrastructure, public safety networks, smart parking solutions, and digital signage environments. Governments across Asia-Pacific, the Middle East, Europe, and North America are investing heavily in connected urban infrastructure requiring localized processing capabilities. Mini computers provide ideal edge processing platforms for traffic analytics, environmental monitoring, and real-time public data management. The increasing integration of IoT sensors and AI-enabled urban management systems is expected to generate sustained demand for compact edge computing hardware over the coming decade.

Growth of AI-Driven Consumer and Gaming Applications

The rising popularity of AI-enabled gaming, content creation, and multimedia applications is opening new opportunities for high-performance mini-computers. Compact gaming PCs equipped with discrete GPUs and AI acceleration technologies are gaining traction among consumers seeking portable yet powerful computing systems. Streaming, 3D rendering, and AI-assisted creative workflows are increasingly being performed on mini workstations capable of handling advanced graphics workloads. The growing creator economy and expansion of eSports ecosystems are expected to strengthen demand for compact gaming and content creation systems globally. Vendors offering modular upgradeability, high-speed connectivity, and advanced cooling technologies are likely to gain a competitive advantage within this rapidly expanding segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 20.8 Billion |

| Market Size in 2026 | USD 22.34 Billion |

| Market Size in 2031 | USD 31.92 Billion |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Desktop mini PCs dominate the global market, accounting for nearly 46% of total revenue in 2025. These systems are widely adopted across enterprise offices, educational institutions, and residential environments because they combine performance efficiency with compact form factors. Consumer mini PCs remain highly popular for home entertainment, streaming, and productivity applications, while business mini PCs are increasingly replacing traditional desktop towers in enterprise environments. Industrial mini computers represent one of the fastest-growing product categories due to rising demand from smart manufacturing and industrial automation sectors. Rugged mini PCs and edge AI systems are increasingly deployed across logistics, robotics, machine vision, and industrial control applications. Single-board mini computers are also gaining traction in educational computing, IoT development, and embedded system design because of their affordability and flexibility.

Application Insights

Industrial automation remains the leading application segment, contributing approximately 27% of global market revenue in 2025. Smart factories increasingly rely on compact computing systems for robotics management, predictive maintenance, machine vision processing, and industrial analytics. Edge computing applications are expanding rapidly as enterprises seek low-latency, localized data processing capabilities. Digital signage and retail POS systems represent another important application segment, particularly across smart retail environments. Healthcare applications are also growing steadily, with mini-computers being deployed for diagnostic imaging, telemedicine systems, and patient monitoring infrastructure. Gaming and content creation applications are witnessing rapid growth as high-performance compact systems equipped with advanced GPUs become increasingly mainstream among consumers and creators.

Distribution Channel Insights

Online retail platforms dominate mini computer sales globally, accounting for more than 60% of total shipments in 2025. Consumers increasingly prefer online purchasing because of broader product selection, customizable hardware configurations, and transparent pricing comparisons. Direct-to-consumer sales channels are expanding rapidly as manufacturers strengthen their e-commerce capabilities and digital marketing strategies. Enterprise procurement contracts and IT system integrators remain important distribution channels for industrial and commercial deployments requiring customized solutions. Electronics retail stores continue to play a role in consumer-focused categories, particularly for gaming-oriented and premium mini computing systems. Value-added resellers are increasingly supporting deployment across enterprise edge computing and industrial automation environments.

Processor Architecture Insights

x86 architecture dominates the mini computers market with nearly 72% share in 2025 due to broad compatibility with enterprise applications, Windows operating systems, and industrial software ecosystems. Intel-based systems continue to lead commercial deployments because of their established enterprise infrastructure and strong processing capabilities. AMD-based mini PCs are gaining popularity within gaming, AI-enabled computing, and high-performance workstation categories due to competitive graphics performance and multi-core processing efficiency. ARM-based mini computers are witnessing increasing adoption in energy-efficient and embedded applications, particularly within IoT infrastructure, mobile edge devices, and low-power enterprise systems. RISC-V architecture remains an emerging segment with growing interest in open-source processor ecosystems and specialized embedded applications.

End-Use Industry Insights

The IT & telecommunications industry remains one of the largest end-use sectors for mini computers because of the growing deployment of edge nodes, network management systems, and compact server replacements. Manufacturing represents the fastest-growing end-use segment, supported by smart factory investments and Industry 4.0 adoption. Retail and e-commerce sectors are increasingly deploying mini computers in kiosks, digital signage, POS terminals, and customer analytics systems. Healthcare demand is rising steadily due to the increasing adoption of compact computing systems for diagnostics, imaging, and telemedicine infrastructure. Government agencies and educational institutions are also deploying energy-efficient mini PCs to modernize digital infrastructure while reducing operating costs. Emerging applications in autonomous robotics, AI surveillance, and intelligent transportation systems are expected to create additional growth opportunities across end-use industries.

Explore more data points, trends and opportunities Download Free Sample Report

Mini Computers Market Segmentations

By Product Type

- Desktop Mini PCs

- Industrial Mini Computers

- Single Board Mini Computers

- Stick PCs

- Thin Client Mini Computers

- Modular Mini Computing Systems

By Processor Architecture

- x86 Architecture

- ARM Architecture

- RISC-V Architecture

By Application

- Industrial Automation

- Edge Computing

- Digital Signage

- Gaming & eSports

- Healthcare Devices

- Retail POS Systems

- Education & E-learning

- Surveillance & Security

- Smart Manufacturing

- Media & Content Creation

By End-Use Industry

- Consumer Electronics

- IT & Telecommunications

- Manufacturing

- Healthcare

- Retail & E-commerce

- Government & Defense

- Education

- Automotive

- Energy & Utilities

By Distribution Channel

- Online Retail

- Direct Sales

- Electronics Retail Stores

- IT System Integrators

- Value-Added Resellers (VARs)

Regional Insights

North America

North America accounted for approximately 31% of the global mini-computers market in 2025. The United States remains the largest regional market due to strong enterprise IT spending, rapid adoption of edge computing infrastructure, and increasing investments in AI-enabled localized processing systems. Hybrid work trends and enterprise digitalization continue to accelerate demand for compact computing systems across commercial sectors. Canada is witnessing increasing adoption across healthcare, education, and public infrastructure modernization projects. The region also benefits from strong innovation ecosystems and the presence of major technology developers focusing on AI-capable compact computing platforms.

Europe

Europe represents a major market for industrial and energy-efficient mini computers, driven by advanced manufacturing ecosystems and strict sustainability regulations. Germany leads regional demand due to strong Industry 4.0 adoption and extensive deployment of industrial automation systems. The United Kingdom is witnessing increasing enterprise demand for compact office computing solutions, while France and Italy continue expanding digital retail and smart infrastructure deployments. European organizations increasingly prioritize low-power computing systems to align with carbon reduction goals and energy efficiency mandates. Industrial mini PCs are particularly gaining traction across automotive manufacturing, logistics, and factory automation applications.

Asia-Pacific

Asia-Pacific dominates the global mini computers market with nearly 38% share in 2025 and remains the fastest-growing region globally. China leads both manufacturing and consumption because of its massive electronics production ecosystem and growing digital infrastructure investments. Taiwan remains a critical global hub for compact computing hardware, semiconductor manufacturing, and motherboard production. Japan and South Korea continue to witness strong demand from robotics, automation, and advanced electronics industries. India is emerging as one of the fastest-growing markets due to expanding digitalization initiatives, rising SME technology adoption, and government support for domestic electronics manufacturing through initiatives such as “Make in India” and PLI schemes.

Latin America

Latin America is gradually expanding within the mini computer market, led by Brazil and Mexico. Rising adoption of digital retail infrastructure, educational technology systems, and SME digitization is supporting demand for compact computing solutions. Mexico benefits from strong integration with North American electronics supply chains and increasing manufacturing investments. Regional demand remains price-sensitive, encouraging adoption of affordable compact systems across both consumer and commercial environments.

Middle East & Africa

The Middle East & Africa region is witnessing increasing demand for mini computers driven by smart city initiatives, telecom modernization projects, and government-led digital transformation programs. UAE and Saudi Arabia are investing heavily in AI infrastructure, surveillance systems, and intelligent transportation networks that require localized edge computing capabilities. South Africa remains an important regional market due to the rising adoption of industrial automation and enterprise digital infrastructure. Increasing investments in connected urban infrastructure and public sector digitization are expected to support long-term regional growth.

Key Players in the Mini-Computers Market

- Intel Corporation

- Apple Inc.

- Dell Technologies

- HP Inc.

- Lenovo Group

- ASUS

- Acer Inc.

- MSI

- Gigabyte Technology

- ZOTAC

- Shuttle Inc.

- MINISFORUM

- Beelink

- Azulle

- Raspberry Pi Foundation