Microwaveable Stuffed Animal Toys Market Size

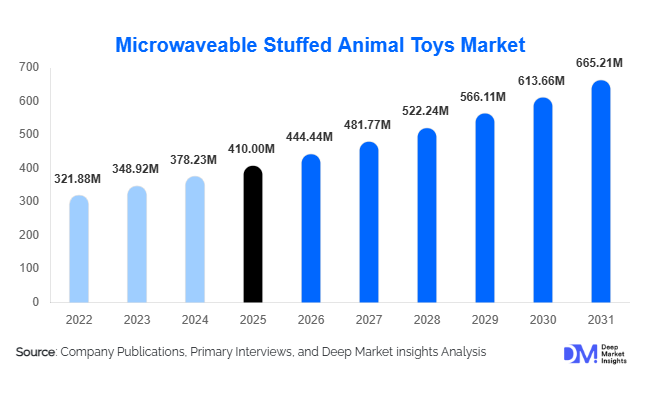

According to Deep Market Insights, the global microwaveable stuffed animal toys market size was valued at USD 410 million in 2025 and is projected to grow from USD 444.44 million in 2026 to reach USD 665.21 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The market growth is primarily driven by rising awareness of non-electric heat therapy products, increasing demand for comfort-based wellness solutions for children and adults, and the premiumization of plush toys with aromatherapy and organic fillings.

Key Market Insights

- Natural grain-filled plush toys dominate the market, accounting for over 50% of total sales in 2025 due to perceived safety and eco-friendliness.

- Online retail channels contribute more than 40% of global revenue, driven by D2C brand expansion and cross-border e-commerce growth.

- North America holds the largest regional share (35%), supported by strong consumer spending and high awareness of therapeutic plush products.

- Asia-Pacific is the fastest-growing region, expanding at nearly 10% CAGR through 2031 due to rising disposable income and gifting culture.

- Mid-range products (USD 20–40 price band) represent the largest revenue share, balancing affordability and premium features.

- Adult adoption is rising steadily, particularly for stress relief, menstrual comfort, and sleep therapy applications.

What are the latest trends in the microwaveable stuffed animal toys market?

Premiumization and Aromatherapy Integration

Manufacturers are increasingly incorporating aromatherapy elements such as lavender and chamomile into microwaveable plush toys, enhancing their positioning as wellness products rather than simple children’s toys. This trend supports higher average selling prices and improved brand differentiation. Premium packaging, organic certifications, and sustainable textile sourcing are becoming mainstream among leading brands. Companies are also launching seasonal and limited-edition collections to drive repeat purchases, especially during holiday gifting cycles. The shift toward wellness branding has expanded target demographics to include teenagers and adults seeking relaxation and sleep support solutions.

Expansion of Direct-to-Consumer (D2C) Sales Channels

E-commerce platforms and D2C websites now account for more than 42% of global revenue. Digital marketing campaigns targeting parents, wellness-focused adults, and gift buyers are significantly enhancing brand visibility. Influencer marketing, social media advertising, and subscription-based seasonal product launches are accelerating sales. Cross-border logistics improvements are enabling U.S. and European brands to expand into Asia-Pacific and Latin America without heavy capital expenditure. Personalized plush toys and customizable scents are further boosting online sales conversions.

What are the key drivers in the microwaveable stuffed animal toys market?

Growing Demand for Non-Electric Heat Therapy Products

Parents and adult consumers are increasingly seeking safe, microwave-based heat therapy alternatives to electric heating pads. Microwaveable plush toys provide portable, reusable, and child-safe warmth, making them attractive for bedtime routines and minor muscle discomfort. Rising awareness around child anxiety and sleep disorders has strengthened this demand globally.

Rising Wellness and Mental Health Awareness

The broader wellness industry, growing at over 8% annually, is positively influencing this market. Consumers are integrating comfort-based therapeutic products into daily routines. Plush toys that combine warmth with calming scents align with holistic health practices, supporting consistent market expansion.

What are the restraints for the global market?

Raw Material Price Volatility

Natural fillings such as wheat and flaxseed are subject to agricultural price fluctuations. Volatile textile costs and logistics disruptions also impact production margins, particularly for mid-range brands competing on price.

Stringent Safety Regulations

Compliance with CPSIA, CE, and ASTM safety standards increases manufacturing costs. Product recalls due to overheating risks or stitching defects can significantly impact brand reputation and financial performance.

What are the key opportunities in the microwaveable stuffed animal toys industry?

Adult Therapeutic Market Expansion

Adult consumers represent the fastest-growing end-user segment. Products designed for menstrual relief, neck and shoulder therapy, and stress management can significantly increase the addressable market size. Premium adult-oriented collections also allow higher margins and subscription-based repeat purchases.

Sustainable and Organic Product Lines

Eco-conscious consumers in North America and Europe are willing to pay premium prices for certified organic fillings and biodegradable packaging. Sustainable sourcing and traceable supply chains offer long-term competitive advantage and institutional sales opportunities in healthcare and pediatric therapy centers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 410 Million |

| Market Size in 2026 | USD 444.44 Million |

| Market Size in 2031 | USD 665.21 Million |

| CAGR | 8.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Configuration Insights

Fully microwaveable plush toys dominate the global market, accounting for approximately 46% of total revenue in 2025. The leading position of this segment is primarily driven by ease of use, stronger heat retention capability, and simplified product design that eliminates detachable components. Consumers, particularly parents, prefer single-piece microwaveable plush toys due to reduced risk of insert misplacement and consistent heating performance. The growth of bedtime therapy routines and child anxiety management solutions has further strengthened demand for these integrated models. Additionally, manufacturers are improving stitching durability and internal heat distribution technology, enhancing product safety and longevity, two critical purchase drivers.

Removable heat-pack variants are gaining traction, especially among hygiene-conscious parents who prefer washable outer covers. This sub-segment benefits from rising awareness of product cleanliness, particularly in North America and Europe. Meanwhile, licensed character-based microwaveable plush toys are emerging as a strong niche segment in Asia-Pacific, where gifting culture and character merchandising significantly influence purchase decisions. Customizable and personalized plush toys, offering embroidered names, tailored scents, and seasonal themes, are expanding rapidly via direct-to-consumer online platforms. These customized products command premium pricing, increasing average selling prices and strengthening brand loyalty.

Filling Material Insights

Natural grain-based fillings lead the market with an estimated 52% revenue share in 2025. The dominance of this segment is driven by consumer preference for perceived safety, natural heat retention properties, and eco-friendly positioning. Wheat, flaxseed, and millet-based fillers provide longer heat duration and a more evenly distributed warmth profile, making them suitable for both pediatric and adult therapeutic applications. Increasing demand for chemical-free and non-electric heat therapy solutions has further accelerated adoption of natural fillings.

Gel-based inserts are widely used in adult-oriented therapeutic plush products due to their consistent temperature distribution and flexibility. These variants are particularly popular for menstrual relief and muscle therapy applications. Organic-certified fillings are gaining strong momentum in Europe, supported by strict regulatory compliance standards and sustainability-focused consumer behavior. Brands emphasizing traceable sourcing and biodegradable packaging are capturing premium market segments and achieving higher profit margins.

Distribution Channel Insights

Online retail remains the dominant distribution channel, contributing approximately 42% of global revenue in 2025. The leadership of this segment is driven by expanding e-commerce penetration, digital marketing strategies targeting parents and wellness consumers, and the rapid growth of cross-border logistics. Direct-to-consumer (D2C) models allow brands to control pricing, gather consumer data, and launch limited-edition collections efficiently. Personalized plush toys and subscription-based seasonal offerings are particularly well-suited to online platforms, further strengthening channel dominance.

Specialty toy stores and wellness retailers maintain steady demand, especially in urban centers where consumers seek in-person product verification. Mass retail chains continue to generate volume sales in North America due to competitive pricing strategies. Pharmacies and wellness stores are increasingly positioning microwaveable plush toys as therapeutic comfort products rather than traditional toys, expanding their consumer base to adult users and healthcare-oriented buyers.

End-User Insights

Children aged 4–12 years represent the largest end-user segment, accounting for approximately 44% of total market revenue in 2025. The dominance of this segment is driven by gifting occasions, bedtime comfort applications, and parental demand for non-medicated soothing solutions. Increasing awareness of childhood anxiety and sleep disturbances has reinforced the segment’s growth.

However, the adult user segment is the fastest-growing category, projected to expand at nearly 9% CAGR through 2031. Growth is supported by rising stress levels, menstrual pain management demand, and increased adoption of heat therapy for relaxation and muscle tension relief. Teenagers also represent an emerging segment, particularly in the Asia-Pacific, where plush toys are culturally integrated into gifting practices.

Explore more data points, trends and opportunities Download Free Sample Report

Microwaveable Stuffed Animal Toys Market Segmentations

By Product Configuration

- Fully Microwaveable Plush Toys

- Removable Heat-Pack Plush Toys

- Scented Therapeutic Plush Toys

- Licensed Character Microwaveable Plush Toys

- Customized & Personalized Microwaveable Plush Toys

By Filling Material

- Natural Grain-Based Fillings (Wheat, Flaxseed, Millet)

- Gel-Based Thermal Inserts

- Synthetic Bead-Based Fillers

- Organic-Certified Natural Fillings

By Distribution Channel

- Online Retail (E-commerce & D2C)

- Specialty Toy Stores

- Mass Retail Chains & Hypermarkets

- Pharmacies & Wellness Stores

- Gift Shops & Seasonal Retailers

By End-User

- Infants & Toddlers (0–3 Years)

- Children (4–12 Years)

- Teenagers (13–18 Years)

- Adults (Therapeutic & Wellness Users)

Regional Insights

North America

North America leads the global microwaveable stuffed animal toys market with a 35% market share in 2025, driven primarily by the United States, which accounts for approximately 28% of global revenue. Regional growth is supported by high disposable income levels, strong e-commerce infrastructure, and widespread awareness of mental wellness products. Parents in the U.S. increasingly prefer non-electric therapeutic products for children, while adult adoption for stress management is rising steadily. Seasonal gifting demand and established retail distribution networks further reinforce market dominance. Canada contributes consistent growth through specialty toy retailers and wellness-focused outlets.

Europe

Europe holds approximately 27% of global revenue, with the U.K., Germany, and France serving as major demand centers. Regional growth is strongly driven by stringent safety regulations, which enhance consumer trust and encourage premium product adoption. Germany demonstrates particularly strong demand for organic-certified and sustainably sourced plush products. Additionally, increasing focus on eco-friendly consumption patterns and rising awareness of alternative therapy solutions support regional expansion. Online retail penetration and cross-border trade within the European Union further facilitate steady growth.

Asia-Pacific

Asia-Pacific accounts for approximately 25% of the global market and is the fastest-growing region, expanding at nearly 10% CAGR through 2031. Growth drivers include rising middle-class income, expanding urbanization, and a strong gifting culture across China, Japan, and South Korea. China dominates regional production and consumption due to its robust manufacturing ecosystem and growing domestic demand. Japan shows a strong affinity for character-licensed plush toys, while India is emerging as a high-potential market driven by increasing online retail penetration and rising awareness of wellness products. Rapid digital commerce growth and influencer-driven marketing are accelerating regional sales.

Latin America

Latin America represents approximately 7% of the global market, led by Brazil and Mexico. Regional growth is primarily driven by seasonal gifting patterns, improving retail infrastructure, and rising urban middle-class populations. Increasing access to international e-commerce platforms is enabling consumers to purchase imported premium brands. However, price sensitivity remains a limiting factor, favoring mid-range product adoption.

Middle East & Africa

The Middle East & Africa region accounts for around 6% of global revenue. The UAE and South Africa serve as primary demand hubs due to higher disposable incomes and well-developed retail ecosystems. Growth in the Middle East is driven by a premium gifting culture and strong import networks for international brands. In Africa, expanding urban retail centers and increasing consumer awareness are gradually supporting adoption. Cross-border imports and distributor-led retail expansion are key enablers of regional growth.

Key Players in the Microwaveable Stuffed Animal Toys Market

- Warmies

- Intelex Group

- Greenlife Value GmbH

- Aroma Home

- Habibi Plush

- Cozy Time Limited

- Sootheze

- Chongqing Lechuang Toy Co., Ltd.

- Intelex Australia

- Intelex Canada

- Intelex Japan

- Intelex South Africa

- Intelex New Zealand

- Intelex Europe

- Intelex USA LLC