Microwave Cart Market Size

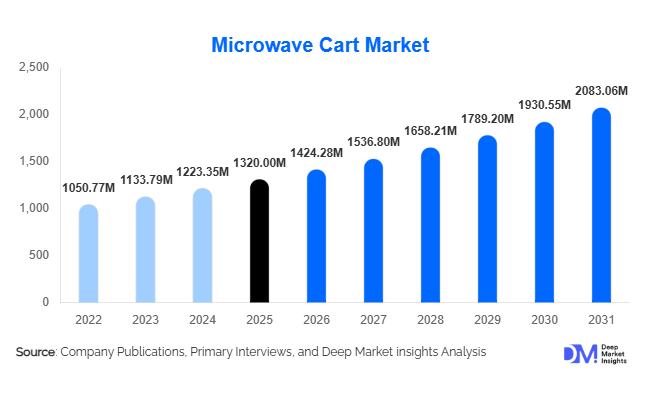

According to Deep Market Insights, the global microwave cart market size was valued at USD 1,320 million in 2025 and is projected to grow from USD 1,424.28 million in 2026 to reach USD 2,083.06 million by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). Market growth is primarily driven by increasing adoption of modular kitchen furniture, rising urban apartment living, and growing demand for multifunctional storage solutions across residential and commercial environments. Microwave carts are evolving from basic appliance stands into integrated kitchen organization systems that combine storage, mobility, and space optimization. Expanding e-commerce penetration and flat-pack furniture logistics have further accelerated global adoption, making microwave carts accessible across both developed and emerging markets.

Key Market Insights

- Space-saving and multifunctional furniture demand is rising globally, driven by urbanization and smaller residential layouts.

- Online retail channels dominate sales growth, supported by flat-pack shipping and direct-to-consumer furniture models.

- Residential households account for the majority of demand, supported by increasing microwave appliance penetration worldwide.

- Asia-Pacific is the fastest-growing regional market, fueled by expanding middle-class housing and rapid e-commerce adoption.

- Wood-based microwave carts remain the leading product category, balancing affordability with aesthetic compatibility.

- Commercial foodservice and institutional demand is expanding, particularly across offices, hospitals, and cloud kitchens.

What are the latest trends in the microwave cart market?

Rise of Multifunctional and Modular Kitchen Furniture

Consumers increasingly prefer furniture that serves multiple purposes within limited living spaces. Microwave carts now integrate drawers, cabinets, adjustable shelving, and mobility features, transforming them into compact kitchen workstations. Modular kitchen trends have encouraged manufacturers to design adaptable carts compatible with different layouts and appliance sizes. Urban households and rental accommodations particularly favor flexible furniture that can be relocated easily without permanent installation. Manufacturers are also introducing foldable and compact models targeting studio apartments and micro-housing developments, reflecting broader global shifts toward efficient living environments.

E-Commerce-Driven Product Innovation

The rapid expansion of online furniture retail has reshaped how microwave carts are designed and marketed. Companies are prioritizing flat-pack engineering, lightweight materials, and simplified assembly systems to reduce logistics costs and improve delivery efficiency. Digital platforms enable consumers to compare designs, pricing, and reviews, encouraging faster purchase decisions. Augmented visualization tools and AI-powered recommendation engines are increasingly integrated into online retail platforms, helping customers visualize furniture placement before purchasing. Social media marketing and influencer-led home organization trends are further accelerating demand, particularly among younger homeowners and renters.

What are the key drivers in the microwave cart market?

Growing Demand for Space Optimization Solutions

Rising housing costs and shrinking apartment sizes worldwide are driving demand for compact furniture solutions. Microwave carts offer an affordable alternative to permanent cabinetry installations, enabling flexible kitchen organization. Urban consumers increasingly prioritize mobility and adaptability, which positions microwave carts as essential functional furniture rather than optional accessories. This driver is particularly strong in densely populated cities across Asia-Pacific and Europe, where efficient space utilization directly influences purchasing decisions.

Expansion of Commercial Microwave Usage

The growth of quick-service restaurants, shared workspaces, and healthcare facilities has increased the installation of microwaves in commercial environments. These settings require movable platforms that enable easy cleaning, relocation, and operational flexibility. Heavy-duty microwave carts designed with metal frames and high load-bearing capacity are gaining popularity across institutional buyers. Growth of cloud kitchens and food delivery ecosystems further reinforces demand for flexible kitchen infrastructure.

What are the restraints for the global market?

Competition from Built-In Kitchen Cabinetry

In developed markets, high-income households increasingly adopt built-in modular kitchens that integrate appliances directly into cabinetry. This trend reduces the need for standalone microwave carts in premium residential segments. Custom kitchen installations also offer aesthetic uniformity, limiting adoption among luxury housing projects where permanent fixtures are preferred.

Raw Material Price Volatility

Fluctuations in engineered wood, steel, and transportation costs create pricing pressure for manufacturers. Since microwave carts operate within highly competitive and price-sensitive categories, companies often struggle to transfer cost increases to consumers. Margin compression remains a key challenge, especially for mid-range and economy product segments.

What are the key opportunities in the microwave cart industry?

Growth of Compact Urban Housing

Rapid urbanization and expansion of rental housing markets create strong opportunities for portable furniture solutions. Microwave carts appeal to renters and young professionals seeking non-permanent kitchen infrastructure. Manufacturers focusing on lightweight, foldable, and modular designs tailored to compact living environments can capture growing demand across emerging economies.

Institutional and Foodservice Expansion

Hospitals, educational campuses, corporate offices, and cloud kitchens increasingly deploy microwave carts to support shared pantry infrastructure. Institutional procurement provides recurring bulk orders and long-term contracts, offering stable revenue streams. Stainless steel and heavy-duty variants are particularly attractive in these environments due to durability and hygiene compliance.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1320 Million |

| Market Size in 2026 | USD 1424.28 Million |

| Market Size in 2031 | USD 2083.06 Million |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Mobile microwave carts dominate the global market, accounting for nearly 34% of total demand, primarily driven by increasing consumer preference for flexible and space-efficient kitchen solutions. The leading segment benefits from rising urbanization, smaller residential layouts, and growing demand for movable furniture that enhances kitchen functionality without permanent installation. Wheeled designs enable easy repositioning, simplified cleaning processes, and adaptability across multi-purpose living spaces, making them particularly attractive for apartments and rental housing. Multifunction storage carts are gaining strong traction as consumers increasingly seek integrated furniture solutions combining appliance placement with organized storage capacity. Fixed microwave carts continue to appeal to budget-conscious buyers and households prioritizing stability and affordability, especially in price-sensitive markets. Meanwhile, heavy-duty commercial variants are expanding steadily within foodservice environments and institutional kitchens where durability and load-bearing capacity are critical. Foldable and collapsible designs are emerging rapidly in densely populated urban markets, supported by growing demand for compact furniture that can be stored efficiently when not in use, reflecting broader trends toward modular and flexible home interiors.

Material Type Insights

Wood-based microwave carts hold the largest market share at approximately 46%, supported by strong consumer preference for aesthetically pleasing and cost-effective furniture materials that align with modern kitchen décor. The segment’s leadership is driven by the scalability of engineered wood manufacturing, including MDF and particle board, which enables manufacturers to deliver visually appealing products at competitive price points. These materials provide design versatility, allowing finishes that mimic premium wood textures while maintaining affordability. Metal-based carts, particularly stainless steel variants, are witnessing accelerated adoption within commercial and institutional applications due to superior durability, hygiene compliance, and resistance to moisture and heat exposure. Growth in professional kitchens and foodservice establishments further strengthens this segment. Composite and glass-based materials cater to premium and design-focused consumers seeking contemporary aesthetics and minimalist styling, particularly in developed markets where interior design trends influence purchasing behavior. Increasing innovation in material combinations is also enabling manufacturers to balance durability with visual appeal, expanding consumer choice across price tiers.

Price Range Insights

The mid-range segment (USD 80–200) leads the global market with approximately 41% share, driven by balanced consumer expectations between affordability, durability, and functional design. This segment benefits from rising disposable incomes and growing willingness among consumers to invest in long-lasting home organization products without entering premium price brackets. Mid-range products typically offer enhanced storage configurations, improved material quality, and better mobility features, making them the preferred choice for mainstream households. Economy-priced microwave carts remain highly relevant in emerging markets where affordability remains the primary purchase driver, supported by expanding middle-class populations and first-time furniture buyers. Premium models priced above USD 200 are gaining momentum among design-conscious consumers, hospitality operators, and institutional buyers seeking superior build quality, aesthetic differentiation, and extended product lifespans. The gradual premiumization of home furniture and increased emphasis on kitchen aesthetics continue to support growth across higher-value segments.

Application Insights

Residential applications dominate the market, accounting for nearly 62% of total demand, supported by rising global microwave oven ownership and increasing consumer focus on home organization and kitchen space optimization. The leading residential segment is driven by lifestyle shifts toward multifunctional living spaces, smaller apartment sizes, and increased home renovation activities. Consumers increasingly view microwave carts as both functional furniture and interior design elements that enhance kitchen efficiency. Commercial applications are expanding rapidly as restaurants, cafés, and cloud kitchens invest in compact and movable kitchen infrastructure to optimize workspace utilization. Growth in quick-service restaurants and shared workplace pantries further contributes to adoption. Institutional applications across healthcare facilities, educational campuses, and corporate environments are also increasing steadily, driven by infrastructure expansion and the need for organized shared kitchen areas that improve operational efficiency and hygiene management.

Explore more data points, trends and opportunities Download Free Sample Report

Microwave Cart Market Segmentations

By Product Type

- Fixed Microwave Carts

- Mobile Microwave Carts

- Multifunction Kitchen Storage Microwave Carts

- Foldable/Compact Microwave Carts

- Heavy-Duty Commercial Microwave Carts

By Material Type

- Wood-Based Microwave Carts

- Metal-Based Microwave Carts

- Glass & Composite Microwave Carts

- Plastic/Polymer-Based Microwave Carts

By Application

- Residential Household Use

- Commercial Foodservice Use

- Institutional Use

By Distribution Channel

- Online Retail

- Furniture Stores

- Hypermarkets & Superstores

- Specialty Kitchen Stores

Distribution Channel Insights

Online retail accounts for approximately 48% of global sales, emerging as the leading distribution channel due to expanding e-commerce ecosystems and changing consumer purchasing behavior. The segment’s growth is driven by wide product assortments, transparent pricing comparisons, customer reviews, and convenient home delivery options. Direct-to-consumer brand websites and large online marketplaces enable manufacturers to reach geographically diverse customers while reducing reliance on traditional retail infrastructure. Offline retail channels, including furniture stores, home improvement outlets, and hypermarkets, continue to play a significant role, particularly in developing markets where consumers prefer physical product inspection before purchase. Hybrid omnichannel strategies are increasingly adopted by retailers, combining online discovery with offline experience to enhance customer confidence and improve conversion rates.

End-Use Industry Insights

The household furniture sector represents the primary end-use industry, accounting for nearly 58% of global demand, driven by continuous residential furniture replacement cycles and growing consumer investment in organized living environments. Demand within this segment is supported by increasing homeownership rates, renovation activities, and rising awareness of ergonomic kitchen layouts. The foodservice industry is the fastest-growing end-use segment, expanding at close to 10% annually as cloud kitchens, cafés, and quick-service restaurants adopt modular and movable equipment solutions to maximize operational efficiency. Healthcare facilities and corporate offices are emerging as important secondary growth areas, as shared pantry installations and employee welfare initiatives encourage investment in organized kitchen infrastructure. Increasing institutional spending on infrastructure modernization further supports long-term demand growth.

Regional Insights

North America

North America holds approximately 32% of global market share, led by the United States, which accounts for nearly 24% of total demand. Regional growth is primarily driven by high household appliance penetration, strong adoption of modular furniture concepts, and widespread acceptance of online furniture retail platforms. Consumers increasingly prioritize convenience-oriented home solutions, supporting demand for mobile and multifunctional microwave carts. Rising home renovation spending, growth in apartment living, and increasing preference for space-saving kitchen layouts further strengthen market expansion. Canada contributes steady growth supported by urban residential construction, remodeling activities, and increasing consumer spending on home improvement products. The region also benefits from strong logistics infrastructure and mature e-commerce ecosystems that accelerate product accessibility.

Europe

Europe represents nearly 26% of global demand, with Germany, the United Kingdom, and France leading consumption. Regional growth is supported by compact urban housing structures that encourage adoption of multifunctional and space-efficient furniture solutions. Sustainability trends play a significant role in purchasing decisions, with consumers increasingly favoring eco-certified materials and environmentally responsible manufacturing practices. Regulatory emphasis on sustainable furniture production encourages innovation in recyclable materials and engineered wood products. Additionally, minimalist interior design trends and high awareness of aesthetic home organization solutions continue to drive steady demand across Western Europe, while Eastern Europe experiences growth through rising disposable incomes and residential modernization.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at over 9% CAGR, driven by rapid urbanization, expanding middle-class populations, and accelerating residential construction activities. China accounts for nearly 15% of global demand due to its large-scale furniture manufacturing ecosystem and strong domestic consumption. India is emerging as the fastest-growing country, supported by urban housing expansion, increasing microwave penetration, and rapid growth of e-commerce platforms that improve furniture accessibility across tier-two and tier-three cities. Japan and South Korea contribute stable demand driven by compact living environments and advanced consumer preference for efficient space utilization. Rising disposable incomes and increasing adoption of modular furniture concepts across Southeast Asia further reinforce regional growth momentum.

Latin America

Latin America accounts for around 9% of global market share, led by Brazil and Mexico. Regional growth is driven by increasing household appliance adoption, expanding urban populations, and gradual improvement in middle-class purchasing power. Affordable and multifunctional furniture solutions remain central to consumer purchasing decisions due to price sensitivity across the region. Growth in organized retail channels and expanding e-commerce penetration are improving product availability and supporting market expansion. Additionally, rising residential development and modernization of urban housing infrastructure continue to create steady demand for compact kitchen furniture solutions.

Middle East & Africa

The Middle East & Africa region contributes approximately 7% of global demand and is witnessing gradual expansion supported by infrastructure development and hospitality sector growth. The UAE and Saudi Arabia act as primary growth engines due to large-scale residential construction projects, tourism expansion, and increasing investments in hospitality and foodservice infrastructure. Rising adoption of modern kitchen layouts and premium home furnishings supports demand in high-income urban centers. Across Africa, improving urbanization rates, expanding healthcare infrastructure, and growth in corporate office developments are encouraging adoption of organized pantry solutions. Increasing institutional investments and gradual retail modernization are expected to sustain long-term regional growth.

Key Players in the Microwave Cart Market

- Sauder Woodworking Co.

- Winsome Wood Inc.

- Linon Home Décor Products

- Ameriwood Home

- HOMCOM (Aosom Group)

- South Shore Furniture

- Prepac Manufacturing Ltd.

- Bush Industries Inc.

- Walker Edison Furniture Company

- Dorel Industries Inc.

- Hodedah Import Inc.

- Monarch Specialties Inc.

- Origami Rack

- Seville Classics

- COSTWAY Inc.