Menstrual Discs Market Size

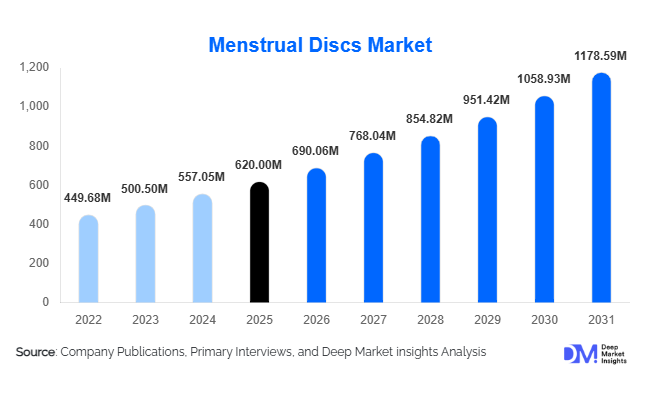

According to Deep Market Insights, the global menstrual discs market size was valued at USD 620 million in 2025 and is projected to grow from USD 690.06 million in 2026 to reach USD 1,178.59 million by 2031, expanding at a CAGR of 11.3% during the forecast period (2026–2031). The menstrual disc market's growth is primarily driven by rising consumer awareness of sustainable feminine hygiene products, increasing adoption of reusable menstrual care solutions, and the expanding availability of innovative menstrual wellness products through digital and retail channels.

Key Market Insights

- Reusable menstrual discs are rapidly replacing disposable menstrual products, supported by sustainability awareness and long-term cost benefits among consumers.

- Medical-grade silicone discs dominate the product landscape, owing to superior comfort, durability, hypoallergenic properties, and regulatory safety compliance.

- North America dominates the global menstrual discs market, driven by premium product adoption, advanced e-commerce penetration, and strong femtech ecosystem development.

- Asia-Pacific is the fastest-growing regional market, supported by rising menstrual health awareness, urbanization, and increasing disposable incomes in countries such as India and China.

- Online retail channels account for the largest market share, with direct-to-consumer platforms and subscription models reshaping purchasing behavior.

- Product innovation remains a key competitive factor, with manufacturers focusing on pull-tab designs, self-emptying mechanisms, and ergonomic leak-resistant structures.

Menstrual Discs Market Trends

Sustainable Menstrual Care Products Gaining Strong Momentum

Consumer demand for environmentally sustainable menstrual products is significantly transforming the feminine hygiene industry. Menstrual discs, particularly reusable variants manufactured using medical-grade silicone, are gaining traction as eco-friendly alternatives to disposable sanitary pads and tampons. Consumers are increasingly evaluating the environmental footprint of personal care products, encouraging brands to emphasize reusability, biodegradable packaging, and carbon-conscious manufacturing. Sustainability-focused purchasing behavior is particularly prominent among millennials and Gen Z demographics across North America and Europe. Governments and NGOs promoting menstrual health awareness and waste reduction initiatives are further accelerating the adoption of reusable menstrual care solutions. Many manufacturers are also integrating sustainability certifications, recyclable packaging, and ethical sourcing practices into their branding strategies to strengthen consumer trust and long-term market positioning.

Digital-First Menstrual Wellness Ecosystems Expanding

The menstrual discs market is increasingly benefiting from the rapid growth of femtech platforms, subscription-based wellness services, and direct-to-consumer digital engagement models. Social media platforms, influencer-led education campaigns, and online menstrual health communities are helping normalize discussions around menstrual discs while educating first-time users about product benefits and usage techniques. Companies are integrating AI-powered menstrual tracking applications, personalized product recommendations, and virtual consultation services to strengthen consumer engagement. E-commerce channels are also enabling discreet purchasing experiences, subscription-based replenishment, and targeted marketing strategies that improve customer retention. In addition, product reviews, tutorial videos, and community-led awareness initiatives are significantly reducing barriers associated with internal menstrual product adoption, especially among younger urban consumers.

Menstrual Discs Market Drivers

Growing Awareness Regarding Sustainable Feminine Hygiene

The increasing global focus on environmental sustainability is a primary factor driving the expansion of the menstrual discs market. Traditional menstrual products generate substantial non-biodegradable waste, encouraging consumers to seek reusable and low-waste alternatives. Menstrual discs offer extended usability, reduced landfill contribution, and lower long-term ownership costs, making them attractive among environmentally conscious consumers. Sustainability campaigns by governments, NGOs, and educational institutions are further strengthening awareness regarding reusable menstrual hygiene products. The growing popularity of zero-waste lifestyles and eco-conscious personal care consumption is expected to continue supporting strong demand growth globally.

Rising Acceptance of Intimate Wellness Products

Changing societal attitudes toward menstrual health and intimate wellness are significantly supporting the adoption of menstrual discs. Historically, internal menstrual products faced cultural resistance in several regions; however, increasing public conversations around menstrual wellness are normalizing product usage. Social media influencers, healthcare professionals, and menstrual equity campaigns are actively educating consumers regarding comfort, safety, and convenience benefits associated with menstrual discs. The increasing participation of women in sports, fitness activities, travel, and professional work environments is also boosting demand for long-duration leak-resistant menstrual solutions that support active lifestyles.

Menstrual Discs Market Restraints

Consumer Learning Curve and Product Familiarity Challenges

One of the key restraints limiting menstrual discs market expansion is the learning curve associated with product insertion, removal, and positioning. First-time users may initially experience discomfort or uncertainty regarding proper usage techniques, which can affect repeat purchases and long-term adoption rates. Consumer education remains critical, particularly in emerging economies where awareness regarding internal menstrual hygiene products remains comparatively low. Limited physician guidance and insufficient product demonstrations in offline retail environments also continue to challenge market penetration.

Competition from Conventional Menstrual Hygiene Products

Despite growing awareness regarding sustainable alternatives, sanitary pads and tampons continue to dominate global feminine hygiene spending due to widespread familiarity, affordability, and retail availability. In developing regions, traditional products remain deeply entrenched due to cultural preferences and lower upfront costs. Premium pricing for reusable menstrual discs may discourage price-sensitive consumers despite long-term economic advantages. Additionally, social stigma and misinformation surrounding internal menstrual products continue to restrict adoption in several conservative markets.

Menstrual Discs Market Opportunities

Expansion Across Emerging Economies

Emerging economies across Asia-Pacific, Latin America, and Africa present substantial growth opportunities for menstrual disc manufacturers. Rising urbanization, improving healthcare access, increasing female workforce participation, and expanding internet penetration are contributing to greater awareness regarding modern menstrual hygiene products. Countries such as India, Indonesia, Brazil, and South Africa are witnessing rapid growth in e-commerce adoption, enabling consumers to access premium feminine hygiene products more conveniently. Government menstrual hygiene initiatives and NGO-led awareness programs are further supporting market accessibility. Manufacturers capable of introducing affordable reusable discs tailored to regional preferences and purchasing power are expected to gain significant competitive advantages in these high-growth markets.

Integration with Femtech and Subscription-Based Wellness Models

The rapid expansion of the femtech ecosystem presents major opportunities for menstrual disc manufacturers to diversify consumer engagement strategies. Companies are increasingly integrating menstrual wellness applications, AI-powered cycle tracking platforms, and subscription-based product delivery services into their business models. Personalized menstrual care recommendations, educational content, and telehealth-supported wellness consultations are strengthening long-term customer retention and improving user confidence. Partnerships between menstrual care brands and digital health platforms are also enabling cross-selling opportunities within broader women’s wellness categories including reproductive health, hormonal wellness, and pelvic care.

Product Type Insights

Reusable menstrual discs dominate the global market, accounting for nearly 68% of total revenue in 2025. Long-term cost savings, environmental sustainability, and increasing consumer preference for eco-friendly menstrual hygiene solutions drive their popularity. Medical-grade silicone reusable discs are particularly favored due to durability, flexibility, and comfort during extended wear. Disposable menstrual discs continue gaining traction among convenience-focused consumers and first-time users seeking lower-commitment alternatives before transitioning to reusable products. Hybrid reusable designs featuring pull-tabs and leak-resistant structures are emerging as premium offerings that improve accessibility for beginner users. Manufacturers are also introducing size-specific and anatomy-adaptive product variants to improve user comfort and reduce leakage concerns.

Material Type Insights

Medical-grade silicone remains the dominant material segment, representing approximately 61% of global market demand due to its hypoallergenic properties, flexibility, and compliance with healthcare safety standards. Silicone discs are widely preferred because they offer superior durability and can be reused for multiple years without compromising product integrity. Thermoplastic elastomer (TPE) materials are also gaining popularity due to softer textures and enhanced flexibility, particularly among younger consumers and first-time users. Biodegradable material innovation is emerging as a developing trend, with companies investing in sustainable polymers and eco-conscious manufacturing techniques to differentiate products in premium sustainability-focused segments.

Distribution Channel Insights

Online retail channels dominate the menstrual discs market, contributing more than 52% of global sales in 2025. Direct-to-consumer websites, e-commerce marketplaces, and subscription-based purchasing models are transforming how consumers access menstrual wellness products. Digital channels provide discreet purchasing experiences, educational tutorials, product comparison tools, and customer reviews that improve user confidence and support repeat purchases. Social media marketing and influencer collaborations are also driving significant online traffic and product awareness. Offline distribution through pharmacies, supermarkets, and wellness stores continues expanding as menstrual discs gain mainstream retail visibility. Healthcare clinics and institutional procurement channels are additionally supporting market growth through menstrual health awareness programs and public hygiene initiatives.

Consumer Age Group Insights

Consumers aged 20–29 years represent the largest user segment globally, supported by strong awareness regarding sustainable lifestyle choices and higher willingness to experiment with innovative menstrual care products. This demographic is highly influenced by social media education, digital wellness communities, and eco-conscious consumption patterns. The 30–45 years age group also contributes significantly to premium product demand, particularly for reusable silicone discs offering convenience and long-duration comfort. Teenagers are gradually emerging as a growing consumer segment due to increasing menstrual education initiatives and rising parental acceptance of sustainable hygiene products. Mature consumers above 45 years remain a smaller but stable segment, primarily seeking comfort-focused products with softer ergonomic designs.

End-Use Insights

Individual consumer use accounts for over 82% of total market demand, driven by increasing awareness regarding menstrual wellness and broader access to reusable hygiene products through digital commerce channels. Consumers are increasingly prioritizing comfort, sustainability, and long-duration wear functionality when selecting menstrual hygiene products. Healthcare and gynecology applications are also witnessing gradual expansion as healthcare professionals increasingly recommend menstrual discs for consumers seeking alternatives to traditional products. Institutional menstrual health programs led by NGOs, schools, and public healthcare agencies are emerging as fast-growing end-use segments, particularly in developing economies where menstrual hygiene accessibility remains a public health priority. Sports and travel applications are additionally contributing to demand growth as consumers seek leak-resistant menstrual products compatible with active lifestyles.

| By Product Type | By Material Type | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for nearly 39% of the global menstrual discs market in 2025, making it the leading regional market. The United States dominates regional demand due to strong consumer awareness, premium feminine wellness spending, and rapid adoption of reusable menstrual care products. The region benefits from advanced e-commerce infrastructure, strong femtech investment activity, and widespread social acceptance of menstrual wellness discussions. Canada is also witnessing strong growth supported by sustainability-conscious consumers and government-supported menstrual equity initiatives. Subscription-based menstrual wellness services and digital-first brands continue driving strong market penetration across North America.

Europe

Europe represents approximately 28% of global market revenue, led by Germany, the United Kingdom, France, and the Nordic countries. European consumers demonstrate strong preference for sustainable menstrual products, supported by environmental awareness and strict regulatory emphasis on product safety. Reusable menstrual discs are particularly popular among younger urban demographics seeking low-waste lifestyle alternatives. The region also benefits from well-developed retail infrastructure and increasing partnerships between menstrual wellness brands and healthcare providers. Carbon-neutral manufacturing practices and eco-certified packaging are emerging as important competitive differentiators across the European market.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR exceeding 14% during the forecast period. China and India represent the largest growth opportunities due to increasing urbanization, rising disposable incomes, and expanding awareness regarding menstrual hygiene alternatives. India is witnessing rapid adoption through direct-to-consumer feminine wellness startups and menstrual education campaigns supported by NGOs and healthcare organizations. Japan and South Korea continue driving premium product innovation, while Southeast Asian markets are gradually increasing awareness regarding reusable menstrual hygiene products. Expanding e-commerce penetration and smartphone usage are accelerating digital product accessibility across the region.

Latin America

Latin America is emerging as a steadily growing market led by Brazil, Mexico, and Argentina. Increasing female workforce participation, improving healthcare awareness, and rising social media influence are contributing to stronger adoption of sustainable menstrual care products. E-commerce channels are playing a crucial role in expanding product accessibility, particularly in urban markets. Regional demand is increasingly shifting toward reusable silicone discs among middle-income and environmentally conscious consumers seeking long-term cost savings and improved menstrual comfort.

Middle East & Africa

The Middle East & Africa region currently represents a smaller share of the global market but offers substantial long-term growth potential. The UAE and Saudi Arabia are emerging as premium markets driven by rising wellness spending and increasing awareness regarding intimate healthcare products. South Africa remains one of the leading African markets due to improving menstrual health awareness and expanding retail access. NGO-led menstrual health initiatives and government-supported hygiene awareness programs are gradually improving product acceptance across several African countries, creating future opportunities for affordable reusable menstrual disc solutions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Menstrual Discs Market

- The Flex Company

- Intimina

- Saalt

- Diva International Inc.

- Lumma

- Nixit

- Cora

- Ruby Cup

- Mooncup Ltd.

- Lena Cup LLC

- Me Luna GmbH

- FemmyCycle

- Blossom Cup

- LadyCup

- Merula GmbH