Men Skincare Products Market Size

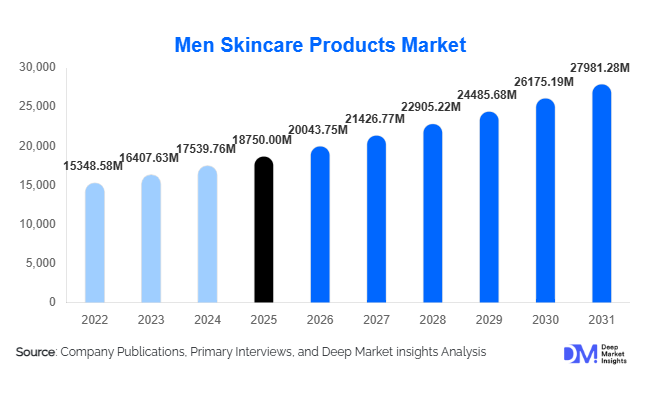

According to Deep Market Insights, the global men skincare products market size was valued at USD 18,750 million in 2025 and is projected to grow from USD 20,043.75 million in 2026 to reach USD 27,981.28 million by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). The market growth is primarily driven by increasing male grooming awareness, rising demand for clean-label and dermatologically tested products, and the rapid expansion of e-commerce-led distribution channels worldwide.

Men’s skincare has evolved beyond traditional shaving products into a comprehensive personal care category that includes facial cleansers, moisturizers, serums, sunscreens, beard care, and targeted treatment solutions. Urbanization, social media influence, professional appearance standards, and growing disposable incomes are encouraging men across all age groups to adopt structured skincare routines. Premiumization trends, especially in North America, Europe, and parts of Asia-Pacific, are raising average selling prices, while emerging markets such as India, Brazil, and Indonesia are driving volume growth. The shift toward natural, organic, and “free-from” formulations is also reshaping product development pipelines globally.

Key Market Insights

- Facial care products dominate the market, accounting for nearly 42% of global revenue in 2025, led by moisturizers, cleansers, and SPF-based products.

- Mass-market pricing tier holds around 55% share, though premium and luxury segments are growing at faster rates due to higher margins.

- Asia-Pacific leads globally with approximately 38% market share, supported by strong demand from China, South Korea, Japan, and India.

- Online retail accounts for about 28% of global sales, driven by subscription models and direct-to-consumer (DTC) brands.

- Natural and clean-label formulations represent over 31% of total revenue, reflecting rising health and sustainability consciousness.

- The top five global players collectively hold nearly 48% market share, indicating moderate consolidation.

What are the latest trends in the men skincare products market?

Clean-Label and Dermatological Formulations Gaining Traction

Consumers are increasingly seeking paraben-free, sulfate-free, vegan, and cruelty-free products. The clean beauty movement has gained significant traction in the male segment, prompting brands to reformulate core SKUs and introduce ingredient transparency initiatives. Dermatologist-backed skincare and clinically proven formulations are gaining prominence, particularly in anti-aging, acne control, and pigmentation treatment categories. Many brands are investing in R&D centers focused on male skin physiology, recognizing differences in oil production, pore size, and shaving-related irritation. This trend is strengthening premium product positioning and supporting higher price realizations.

Digital-First and Subscription-Based Models

The rise of digital-native brands is reshaping purchasing behavior. Direct-to-consumer platforms now offer personalized skincare regimens based on AI-driven skin analysis tools. Subscription-based delivery models are enhancing customer retention and improving lifetime value metrics. Social commerce, influencer marketing, and mobile-first engagement strategies are particularly effective among Gen Z and Millennial consumers. Online channels are also improving product accessibility in emerging economies, reducing reliance on traditional retail infrastructure and enabling niche brands to scale globally.

What are the key drivers in the men skincare products market?

Rising Male Grooming Awareness

Changing social norms and increased emphasis on personal appearance in professional environments are encouraging men to adopt multi-step skincare routines. The growing acceptance of self-care culture and visibility of male grooming influencers have accelerated category adoption globally. This shift has particularly boosted demand among the 25–34 age group, which accounts for nearly 36% of total market revenue.

Premiumization and Product Innovation

Innovation in lightweight formulations, anti-pollution skincare, SPF-infused moisturizers, and beard-specific solutions is expanding the addressable market. Premium skincare products, though representing a smaller share compared to mass products, are growing at faster rates due to aspirational branding and higher disposable incomes in developed markets. Technological advancements such as encapsulated active ingredients and skin microbiome-friendly formulations are further enhancing product differentiation.

What are the restraints for the global market?

Price Sensitivity in Emerging Markets

While demand is rising globally, affordability remains a constraint in price-sensitive regions. Premium and luxury segments face slower penetration in lower-income economies, limiting rapid expansion beyond urban centers.

Intense Competition and Brand Fragmentation

The proliferation of indie and DTC brands has intensified competition. Marketing expenses, influencer collaborations, and promotional pricing strategies are compressing margins, especially in saturated markets such as the U.S. and Western Europe.

What are the key opportunities in the men skincare products industry?

Expansion in Emerging Economies

Rapid urbanization and rising middle-class income in countries such as India, Indonesia, Brazil, and Mexico present strong growth opportunities. Localization of product formulations tailored to tropical climates, pollution exposure, and regional skin concerns can enhance penetration. Government manufacturing initiatives such as “Make in India” and regional production incentives are reducing entry barriers for multinational brands.

Integration of AI and Personalization Technologies

AI-powered skin diagnostics and personalized product bundles represent a significant opportunity. Brands leveraging data analytics to recommend customized regimens can increase customer loyalty and premium pricing power. Digital integration also enables real-time feedback loops, accelerating product development and innovation cycles.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18750 Million |

| Market Size in 2026 | USD 20043.75 Million |

| Market Size in 2031 | USD 27981.28 Million |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Facial care products dominate the men skincare products market with approximately 42% share in 2025, making it the leading product segment globally. The primary driver behind this dominance is the structural shift from basic grooming to multi-step skincare routines among urban male consumers. Daily-use products, such as cleansers and moisturizers, have achieved high penetration rates across both developed and emerging economies, forming the backbone of recurring demand. Additionally, increasing awareness about sun protection and pollution-induced skin damage has significantly boosted SPF-based products and anti-pollution creams. Anti-aging serums and wrinkle-care solutions are witnessing accelerated growth, particularly among consumers aged 30 and above, due to rising professional image consciousness and preventive skincare adoption.

Shaving and beard care products account for nearly 30% of total revenue, supported by consistent global demand for shaving creams, foams, gels, and aftershaves. The resurgence of beard grooming trends has strengthened the beard oil and conditioning sub-segment, particularly in North America, Europe, and parts of the Middle East. Body care products contribute around 18%, driven by increasing awareness of holistic grooming routines and premium body lotions tailored to male skin. Specialized treatment products, including acne, pigmentation, and sensitive-skin solutions, represent roughly 10% but are expanding rapidly due to rising dermatological consultations and growing demand for targeted skincare formulations.

Price Tier Insights

The mass-market segment leads with approximately 55% share of global revenue in 2025, primarily driven by affordability and wide retail penetration across supermarkets, hypermarkets, and drugstores. The leading growth driver for this segment is strong volume demand from Asia-Pacific and Latin America, where price sensitivity remains high and brand loyalty is developing. Large-scale promotional campaigns and bundled grooming kits further reinforce mass-segment dominance.

Premium products account for about 32% of the market, benefiting from ingredient innovation, dermatological endorsements, and aspirational branding. Growth in this segment is supported by rising disposable income, particularly in urban centers across the United States, China, South Korea, and the UAE. Luxury skincare, although smaller at around 13%, commands the highest margins and is expanding steadily in high-income regions, fueled by exclusive formulations, advanced anti-aging solutions, and designer brand positioning.

Distribution Channel Insights

Hypermarkets and supermarkets collectively account for nearly 34% of global sales, making them the largest distribution channel by value. Their dominance is driven by strong supply chain networks, competitive pricing, and accessibility in both urban and semi-urban areas. However, online retail, holding approximately 28% share, is the fastest-growing channel globally. The key growth driver for online sales is the rapid expansion of e-commerce ecosystems, subscription-based grooming models, influencer-driven marketing, and AI-powered personalized product recommendations.

Pharmacies and specialty beauty stores together contribute around 30%, particularly benefiting dermatological and premium skincare lines, where professional consultation plays a role in purchase decisions. Direct-to-consumer (DTC) subscription platforms are emerging as high-retention sales models, enabling brands to gather consumer data, optimize pricing strategies, and improve profit margins through disintermediation.

Age Group Insights

The 25–34 age group leads the market with nearly 36% share in 2025, driven by high skincare engagement, rising disposable income, and strong influence from digital media and workplace grooming standards. This segment represents the most active adopters of preventive skincare, including SPF, anti-aging serums, and specialized treatments. The 15–24 segment is growing rapidly due to acne treatment demand and social media-driven beauty awareness, especially across Asia-Pacific and North America. Consumers aged 35–44 contribute significantly to anti-aging product sales, as early signs of aging increase adoption of premium skincare solutions. Meanwhile, the 45+ demographic is gradually expanding its participation in the market, particularly in developed economies, where mature male consumers are increasingly adopting high-margin anti-wrinkle and pigmentation-correction products.

Explore more data points, trends and opportunities Download Free Sample Report

Men Skincare Products Market Segmentations

By Product Type

- Facial Care Products

- Shaving & Beard Care Products

- Body Care Products

- Specialized & Treatment Products

By Price Tier

- Mass Market

- Premium

- Luxury

By Distribution Channel

- Online Retail

- Hypermarkets & Supermarkets

- Pharmacies & Drugstores

- Specialty Beauty Stores

- Direct-to-Consumer (DTC) Subscriptions

By Age Group

- 15–24 Years

- 25–34 Years

- 35–44 Years

- 45+ Years

By Ingredient Profile

- Conventional Formulations

- Natural & Organic

- Clean/Free-From

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 38% of the global market share in 2025, making it the largest regional contributor. The primary driver of regional growth is a strong grooming culture combined with rapid urbanization and digital retail expansion. China contributes nearly 14% of global revenue, supported by a highly developed e-commerce ecosystem, livestream commerce, and rising middle-class spending. South Korea acts as an innovation hub, leading in advanced formulations, skincare layering routines, and export-oriented production. India is the fastest-growing market in the region at nearly 9% CAGR, driven by expanding urban populations, increasing youth awareness, and government-backed manufacturing initiatives that encourage local production and reduce import dependence.

North America

North America accounts for around 26% share, with the United States representing nearly 20% of global demand. The leading driver for regional growth is premiumization and clean-label adoption. High disposable incomes, strong brand penetration, and widespread acceptance of male grooming culture support sustained demand. The U.S. market is characterized by rapid innovation cycles, celebrity-endorsed brands, and strong DTC penetration. Canada contributes stable growth, supported by rising awareness of dermatological skincare and sustainability-focused purchasing behavior.

Europe

Europe contributes approximately 22% of the global market, led by Germany, the UK, and France. Growth in this region is primarily driven by sustainability regulations, eco-certification standards, and consumer preference for natural and organic products. The UK and Germany show strong demand for beard care and anti-aging solutions, while France remains a premium skincare innovation center. Strict regulatory frameworks around ingredient transparency and environmental compliance are encouraging brands to invest in clean formulations and recyclable packaging, further supporting market expansion.

Latin America

Latin America represents nearly 8% of global revenue, with Brazil and Mexico as key contributors. The major driver of growth in this region is rising urban middle-class income and strong cultural emphasis on personal grooming. Brazil, in particular, demonstrates above-average growth due to high beauty product consumption per capita and increasing male participation in skincare routines. Expanding retail networks and improving digital payment infrastructure are also supporting online sales growth.

Middle East & Africa

The Middle East & Africa accounts for around 6% of global sales. In the Middle East, the UAE and Saudi Arabia are leading premium markets, driven by high disposable income, luxury retail expansion, and a strong preference for international brands. Grooming is culturally embedded, supporting sustained demand for beard and facial care products. In Africa, South Africa leads regional production and consumption, supported by established retail infrastructure and growing awareness of male skincare. Rising tourism, expatriate populations, and increasing urbanization are further contributing to gradual regional market expansion.

Key Players in the Men Skincare Products Market

- L'Oréal

- Procter & Gamble

- Unilever

- Beiersdorf AG

- Estée Lauder Companies

- Shiseido Company

- Johnson & Johnson

- Kao Corporation

- Coty Inc.

- Amorepacific Corporation

- Revlon Inc.

- Colgate-Palmolive

- Edgewell Personal Care

- LVMH

- LG Household & Health Care