Men Rugby League Market Size

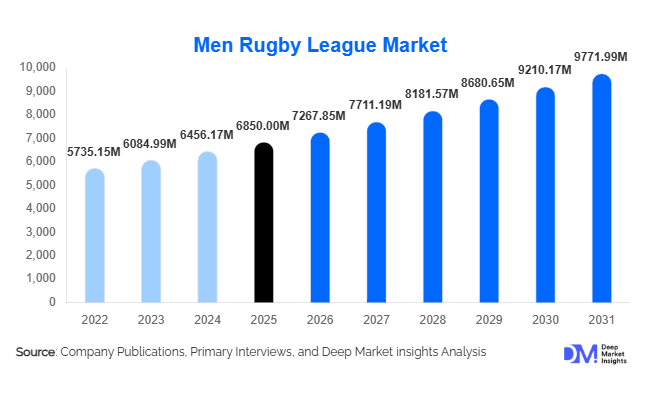

According to Deep Market Insights, the global men rugby league market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7,267.85 million in 2026 to reach USD 9,771.99 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The market growth is primarily driven by rising media rights valuations, increasing global fan engagement through digital platforms, and expanding commercialization of professional rugby leagues. The shift toward OTT streaming, international tournament expansion, and growing sponsorship investments are further strengthening the market outlook.

Key Market Insights

- Media and broadcasting rights dominate the market, accounting for over 40% of total revenues due to high-value multi-year deals.

- Tier 1 professional leagues lead globally, supported by strong fan bases, premium sponsorships, and established governance structures.

- Europe holds the largest market share, driven by the UK’s mature rugby league ecosystem.

- Asia-Pacific is the fastest-growing region, fueled by expansion in Australia and emerging markets.

- OTT streaming platforms are rapidly transforming consumption patterns, enabling direct-to-consumer monetization strategies.

- Sports betting and fantasy gaming integration is emerging as a high-growth revenue stream.

What are the latest trends in the men rugby league market?

Digital Streaming and Direct-to-Consumer Expansion

The increasing adoption of OTT platforms is reshaping how rugby league content is consumed globally. Leagues are investing in proprietary streaming platforms and digital partnerships to directly engage with audiences, reducing reliance on traditional broadcasters. Subscription-based models, real-time analytics, and personalized content delivery are enhancing fan experiences while creating scalable revenue streams. This trend is particularly prominent among younger audiences who prefer mobile-first viewing experiences.

Globalization of Rugby League

The sport is gradually expanding beyond traditional strongholds such as the UK and Australia into emerging markets like North America, Asia, and the Middle East. International tournaments, exhibition matches, and grassroots initiatives are being leveraged to build awareness and fan bases in these regions. This globalization strategy is expected to diversify revenue sources and reduce dependency on mature markets.

What are the key drivers in the men rugby league market?

Rising Value of Broadcasting Rights

Broadcasting rights remain the most significant growth driver, with media companies competing aggressively for exclusive sports content. Multi-year deals provide financial stability to leagues and teams while ensuring consistent revenue inflows. The demand for live sports, which retains high viewership and advertising value, continues to push rights valuations upward.

Growing Digital Fan Engagement

Social media platforms, mobile applications, and streaming services are enabling leagues to connect directly with global audiences. Enhanced fan engagement through interactive content, live updates, and behind-the-scenes access is driving viewership growth and increasing monetization opportunities through targeted advertising and subscriptions.

What are the restraints for the global market?

Limited Global Penetration

Compared to globally dominant sports such as football and cricket, rugby league has a relatively limited international presence. This restricts its ability to attract large-scale sponsorships and global media deals, thereby limiting overall market expansion.

High Operational and Infrastructure Costs

The cost of maintaining stadiums, player salaries, and organizing large-scale events remains high. Smaller leagues and emerging markets often face financial constraints, which can hinder growth and sustainability.

What are the key opportunities in the men rugby league industry?

Integration of Sports Betting and Fantasy Platforms

The legalization of sports betting in various regions has created new opportunities for revenue generation. Rugby league organizations are increasingly partnering with betting platforms to offer real-time engagement tools and fantasy leagues, enhancing fan interaction and monetization.

Expansion into Emerging Markets

Regions such as Asia-Pacific, North America, and the Middle East present significant growth potential. Investments in sports infrastructure, rising disposable incomes, and increasing interest in international sports are creating favorable conditions for market expansion.

Revenue Stream Insights

Media and broadcasting rights dominate the revenue mix, contributing approximately 42% of the total market in 2025, and continue to be the primary growth engine of the men rugby league market. This leadership is driven by long-term, high-value contracts between leagues and broadcasters, coupled with the rising premium for live sports content that attracts consistent viewership and advertising revenue. The increasing shift toward exclusive broadcasting agreements and bundled digital rights is further strengthening this segment’s dominance. Sponsorship and advertising form the second-largest revenue stream, supported by growing brand investments in sports marketing, jersey sponsorships, and integrated digital campaigns. Matchday revenues, including ticket sales, hospitality, and in-stadium spending, remain stable and are gradually recovering and expanding with improved fan experiences and stadium modernization. Merchandising and licensing are gaining traction as clubs and leagues invest in global branding and e-commerce platforms, enhancing fan monetization beyond matchdays. Meanwhile, betting and fantasy sports represent the fastest-growing segment, driven by regulatory liberalization in key markets, real-time data integration, and increased fan engagement through interactive platforms.

League Tier Insights

Tier 1 professional leagues account for nearly 55% of the global market, firmly establishing themselves as the backbone of the industry. Their dominance is primarily driven by established fan bases, lucrative sponsorship agreements, and premium broadcasting deals that significantly outpace other tiers. These leagues benefit from strong governance frameworks, international visibility, and the ability to attract elite players, which further enhances their commercial value. The continued expansion of franchise-based models and international competitions is reinforcing their leadership position. Tier 2 and semi-professional leagues contribute moderate revenues, often serving as feeder systems for top-tier competitions while maintaining regional fan engagement. Grassroots and developmental leagues, although smaller in revenue contribution, play a critical role in sustaining long-term growth by nurturing talent pipelines, increasing participation rates, and expanding the sport’s geographic footprint.

Distribution Platform Insights

Traditional TV broadcasting continues to lead with approximately 48% market share, owing to its extensive reach, established subscriber base, and strong advertising revenues. However, this segment is increasingly being complemented, and gradually challenged, by OTT and digital streaming platforms. The rapid adoption of digital streaming is driven by changing consumer behavior, particularly among younger audiences who prefer on-demand, mobile-first content. OTT platforms are enabling leagues to reach global audiences, offer flexible subscription models, and deliver personalized viewing experiences. The integration of advanced technologies such as AI-based recommendations, multi-angle viewing, and real-time statistics is further enhancing the appeal of digital platforms, positioning them as a key growth driver for future market expansion.

Event Type Insights

Regular season matches account for nearly 60% of total revenue, making them the most significant contributor to the market. Their dominance is attributed to the high frequency of games, consistent fan engagement, and recurring revenue streams from broadcasting, ticket sales, and sponsorships. Playoffs and championship events, while fewer in number, generate significantly higher per-event revenues due to premium ticket pricing, global viewership, and intensified sponsorship activity. These marquee events often serve as major revenue spikes for leagues. International tournaments are emerging as a key growth segment, driven by globalization strategies and efforts to expand the sport into new markets. Their increasing popularity is supported by cross-border broadcasting deals and rising international fan interest.

End-Use Insights

Media companies represent the largest end-use segment, valued at over USD 3,000 million in 2025, driven by the continuous demand for premium live sports content that guarantees high viewer engagement and advertising returns. Sports franchises and clubs are also major end-users, leveraging rugby league as a platform for revenue generation through sponsorships, merchandising, and fan engagement initiatives. Advertisers play a critical role in monetizing viewership, utilizing targeted campaigns and integrated branding opportunities across multiple platforms. The sports betting and fantasy segment is the fastest-growing end-use category, with growth rates exceeding 8% annually, fueled by increasing legalization, digital integration, and consumer interest in interactive sports experiences. Emerging applications, including digital fan engagement platforms, data analytics services, and immersive content technologies, are reshaping traditional revenue models and opening new monetization avenues for stakeholders across the value chain.

| By Revenue Stream | By League Tier | By Distribution Platform | By Event Type |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 20% of the global market, with the United States as the primary growth driver. The region’s expansion is fueled by increasing investments in sports infrastructure, growing interest in alternative and international sports, and the presence of a mature media and entertainment industry willing to invest in new content categories. The rise of OTT platforms and sports betting legalization in several U.S. states is further accelerating market growth by enhancing monetization opportunities and fan engagement. Additionally, strategic initiatives such as exhibition matches and grassroots programs are helping build awareness and expand the fan base.

Europe

Europe dominates the market with around 35% share, led by the UK and France. The region’s leadership is driven by a well-established rugby league ecosystem, strong historical roots of the sport, and highly organized league structures. High-value broadcasting agreements, extensive sponsorship networks, and loyal fan bases contribute significantly to revenue generation. Continuous investments in league development, stadium upgrades, and youth programs further strengthen Europe’s position. The region also benefits from strong regulatory frameworks and governance, ensuring sustainable growth and commercial stability.

Asia-Pacific

Asia-Pacific holds nearly 30% market share, with Australia as the dominant contributor due to its highly commercialized and widely followed rugby league competitions. The region is also the fastest-growing, with a CAGR exceeding 7%, driven by expansion into emerging markets such as India, Southeast Asia, and parts of East Asia. Key growth drivers include rising disposable incomes, increasing sports viewership, and government initiatives promoting sports development. The proliferation of digital platforms and mobile streaming is further enabling access to rugby league content across diverse demographics, significantly boosting regional demand.

Latin America

Latin America represents a smaller share of the market but is witnessing gradual growth, particularly in countries like Brazil. The region’s development is supported by increasing awareness of rugby league, grassroots initiatives, and partnerships with international organizations to promote the sport. Growing youth participation and the influence of global sports culture are contributing to rising interest. Additionally, improvements in digital connectivity and access to international broadcasts are enabling wider audience reach, creating a foundation for long-term growth.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth hub, driven by increasing investments in sports infrastructure and government-led initiatives to diversify economies through sports and entertainment. Countries such as the UAE and Saudi Arabia are actively hosting international events and developing world-class facilities, which are attracting global attention to rugby league. In Africa, the presence of untapped talent and growing grassroots participation is supporting market expansion. The region’s growth is further enhanced by rising disposable incomes, increased tourism-linked sporting events, and strategic partnerships with international leagues.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Men Rugby League Market

- National Rugby League (NRL)

- Rugby Football League (RFL)

- Super League Europe

- International Rugby League (IRL)

- Australian Rugby League Commission

- New Zealand Rugby League

- French Rugby League Federation

- Papua New Guinea Rugby League

- Tonga National Rugby League

- Samoa Rugby League

- Rugby League World Cup Organizing Committee

- Catalans Dragons

- Wigan Warriors

- St Helens R.F.C.

- Leeds Rhinos