Men Perfume Market Size

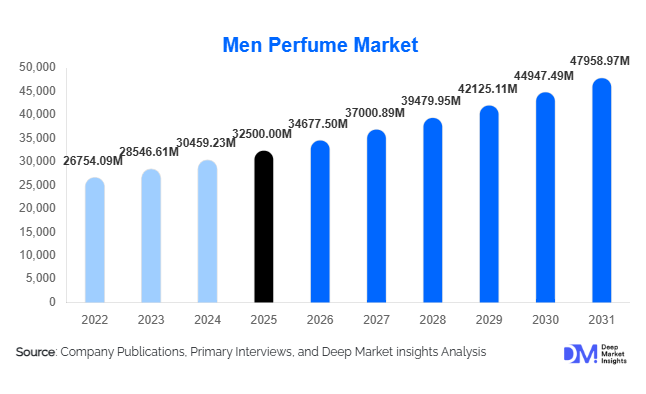

According to Deep Market Insights, the global men perfume market size was valued at USD 32,500 million in 2025 and is projected to grow from USD 34,677.50 million in 2026 to reach USD 47,958.97 million by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The market growth is primarily driven by rising awareness of male grooming, increasing demand for premium and luxury fragrances, and the rapid expansion of e-commerce platforms that enhance product accessibility worldwide. Shifting consumer perceptions around masculinity and personal care are further fueling adoption, particularly among millennials and Gen Z consumers who view fragrances as an extension of personal identity and lifestyle.

Key Market Insights

- Premiumization is a dominant trend, with consumers increasingly opting for high-end and niche fragrances offering longer-lasting scents and unique compositions.

- Millennials account for the largest demand share, driven by higher spending power and strong brand engagement.

- Europe dominates the global market, supported by established fragrance manufacturing hubs and strong consumer demand.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes and increasing grooming awareness.

- Online retail channels are rapidly expanding, enabling global brand reach and personalized consumer engagement.

- Sustainability and clean-label formulations are gaining traction, influencing purchasing decisions and brand loyalty.

What are the latest trends in the men perfume market?

Rise of Niche and Personalized Fragrances

The market is witnessing a shift toward niche and artisanal fragrances that emphasize individuality and exclusivity. Consumers are increasingly seeking unique scent profiles rather than mass-produced options, leading to the growth of boutique fragrance houses. Personalization technologies, including AI-based scent profiling and custom blending services, are further enhancing consumer engagement. This trend is particularly strong among younger demographics who prioritize self-expression and are willing to experiment with unconventional fragrance notes.

Growth of Sustainable and Eco-Friendly Products

Sustainability is becoming a critical factor in product development. Brands are investing in natural ingredients, biodegradable packaging, and refillable bottles to align with consumer expectations and regulatory requirements. Transparency in sourcing and production processes is also gaining importance, with companies highlighting ethical practices such as cruelty-free testing and reduced carbon footprints. This trend is expected to shape long-term brand positioning and consumer trust.

What are the key drivers in the men perfume market?

Increasing Male Grooming Awareness

The growing acceptance of male grooming products is a primary driver of market expansion. Social media influence, celebrity endorsements, and changing cultural norms have significantly increased awareness and adoption of fragrances among men. Fragrances are now considered essential grooming products rather than luxury items, particularly in urban markets.

Expansion of E-commerce and Digital Channels

The rapid growth of online retail has transformed the fragrance industry by improving accessibility and convenience. Consumers can explore a wide range of products, compare prices, and access reviews before making purchases. Digital marketing strategies, including influencer collaborations and targeted advertising, are further driving online sales growth.

What are the restraints for the global market?

High Market Competition and Brand Saturation

The men perfume market is highly competitive, with numerous global and regional players competing for market share. This saturation increases marketing costs and makes differentiation challenging, particularly for new entrants.

Volatility in Raw Material Prices

Fluctuations in the prices of natural ingredients such as essential oils can impact production costs and profit margins. Supply chain disruptions and environmental factors further exacerbate this challenge, creating uncertainty for manufacturers.

What are the key opportunities in the men perfume industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities due to rising disposable incomes and increasing awareness of personal grooming. Companies that tailor products to regional preferences and price sensitivities can capture substantial market share in these regions.

Direct-to-Consumer and Digital Personalization Models

The adoption of direct-to-consumer business models allows brands to engage directly with customers, improving margins and brand loyalty. Personalized recommendations, subscription services, and virtual scent discovery tools are enhancing customer experience and driving repeat purchases.

Product Type Insights

Eau de Parfum (EDP) dominates the men perfume market, accounting for approximately 38% of the total market share in 2025. This leadership position is primarily driven by its higher concentration of fragrance oils (typically 15–20%), which ensures longer-lasting scent performance compared to other product types. Consumers, particularly in the premium and luxury segments, increasingly prefer fragrances that offer durability and strong projection, reducing the need for frequent reapplication. This trend is further reinforced by rising disposable incomes and the growing perception of perfumes as lifestyle and status products. Eau de Toilette (EDT) continues to hold a significant share due to its affordability and suitability for daily wear, especially in warmer climates where lighter fragrances are preferred. Meanwhile, colognes and aftershaves cater to entry-level consumers and high-frequency usage, particularly in emerging markets. The overall shift toward high-performance and premium formulations continues to solidify EDP’s global dominance.

Fragrance Family Insights

Woody fragrances lead the market with an estimated 30% share, driven by their deep-rooted association with traditional masculine identities and their versatility across both formal and casual settings. Notes such as sandalwood, cedarwood, and vetiver are widely preferred due to their longevity and universal appeal. The dominance of woody fragrances is further supported by their strong presence in premium and luxury product lines. Fresh fragrances, including citrus, aquatic, and green notes, are gaining traction among younger consumers and in tropical regions, where lighter and more refreshing scents are favored for daily use. Oriental and gourmand fragrances are expanding rapidly within the luxury segment, driven by demand for bold, distinctive, and long-lasting scent profiles. This diversification in fragrance preferences highlights a shift toward personalization and experimentation among consumers.

Price Segment Insights

The premium segment holds the largest share at approximately 45% of the global market, driven by the increasing consumer inclination toward affordable luxury. This segment benefits from strong brand equity, aspirational marketing, and a balance between quality and price accessibility. Consumers are increasingly willing to invest in premium fragrances that offer superior quality, longer-lasting performance, and brand prestige. The luxury segment, while smaller in volume, contributes disproportionately to revenue due to significantly higher price points and profit margins, often exceeding 30–40%. Mass-market products continue to drive volume growth, particularly in emerging economies, where affordability and accessibility remain key purchase drivers. However, gradual income growth in these regions is expected to shift demand toward premium offerings over time.

Distribution Channel Insights

Offline retail channels dominate the men perfume market with around 60% market share, primarily because fragrances are sensory products that consumers prefer to test before purchasing. Department stores, specialty fragrance boutiques, and duty-free outlets remain critical touchpoints, offering personalized assistance and brand experiences. The dominance of offline channels is particularly evident in premium and luxury segments, where in-store experiences influence purchase decisions. However, online retail is the fastest-growing distribution channel, driven by increasing internet penetration, smartphone usage, and the convenience of home delivery. E-commerce platforms are leveraging AI-driven recommendations, customer reviews, and virtual try-on technologies to replicate in-store experiences. The integration of omnichannel strategies is further enhancing consumer engagement and expanding market reach.

Packaging Type Insights

Spray bottles account for nearly 70% of the market share, owing to their convenience, controlled application, and widespread consumer acceptance. The dominance of spray packaging is also linked to its compatibility with modern fragrance formulations and branding aesthetics. Premium and luxury brands increasingly use innovative spray mechanisms and high-end packaging designs to enhance product appeal. Additionally, travel-sized and refillable packaging options are gaining traction, driven by rising demand for portability and sustainability. Refillable bottles, in particular, are becoming a key differentiator as brands respond to environmental concerns and regulatory pressures, especially in Europe.

Age Group Insights

Millennials represent the largest consumer segment, contributing approximately 50% of the market share. This dominance is driven by their higher disposable incomes, strong brand consciousness, and willingness to experiment with different fragrance profiles. Millennials also actively engage with digital platforms, making them highly responsive to online marketing and influencer-driven campaigns. Gen Z consumers are emerging as the fastest-growing segment, influenced by social media trends, celebrity endorsements, and a strong inclination toward self-expression and individuality. This group is more likely to explore niche and personalized fragrances, contributing to the growth of artisanal and direct-to-consumer brands. Older demographics, while smaller in volume, continue to drive demand for classic and premium fragrances, ensuring stability in the market.

Usage Occasion Insights

Daily wear fragrances dominate the market with around 40% share, supported by the increasing integration of perfumes into everyday grooming routines. This trend is particularly strong among urban consumers who view fragrances as essential personal care products. The growth of workplace culture and social interactions further reinforces daily usage. Formal and special occasion fragrances, on the other hand, are key drivers of premium and luxury segment growth, as consumers seek distinctive and long-lasting scents for events, celebrations, and evening wear. Seasonal and occasion-based marketing strategies by brands continue to stimulate demand in this segment.

| By Product Type | By Fragrance Family | By Price Segment | By Distribution Channel | By Packaging Type |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 28% of the global market, with the United States being the largest contributor. The region’s growth is driven by high consumer awareness of personal grooming, strong purchasing power, and a well-established retail infrastructure. The widespread adoption of premium and luxury fragrances, supported by celebrity endorsements and brand-driven marketing, further fuels demand. Additionally, the rapid expansion of e-commerce and subscription-based fragrance services is enhancing accessibility and customer retention. The presence of major global players and continuous product innovation also contribute to sustained market growth in this region.

Europe

Europe leads the global men perfume market with approximately 35% share, supported by its long-standing heritage in fragrance manufacturing and strong consumer demand. Countries such as France, Germany, Italy, and the UK play a pivotal role, with France serving as a global hub for perfume production and innovation. The region’s growth is driven by high disposable incomes, strong preference for luxury and niche fragrances, and increasing demand for sustainable and clean-label products. Regulatory frameworks promoting ingredient transparency and environmental sustainability are also shaping product development. Additionally, Europe’s well-developed distribution network and strong tourism-driven sales, particularly through duty-free channels, further boost market performance.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a projected CAGR exceeding 8%. The growth is primarily driven by rising disposable incomes, rapid urbanization, and increasing awareness of personal grooming in countries such as China and India. The expanding middle-class population and growing influence of Western lifestyle trends are accelerating fragrance adoption. In China, the market is benefiting from strong e-commerce penetration and digital marketing, while India is witnessing increased demand due to a young population and rising brand consciousness. Japan and South Korea contribute significantly to premium fragrance demand, driven by innovation, high-quality standards, and consumer preference for unique scent profiles. The region’s growth is further supported by the increasing availability of international brands and localized product offerings.

Latin America

Latin America holds approximately 7% share of the global market, with Brazil and Mexico leading regional demand. Growth in this region is driven by urbanization, increasing middle-class income, and rising penetration of international fragrance brands. Cultural emphasis on personal grooming and fragrance usage also supports market expansion. Additionally, the growing popularity of direct selling and e-commerce platforms is improving product accessibility. However, economic volatility and price sensitivity remain key challenges, making mass and premium segments more prominent than luxury offerings.

Middle East & Africa

The Middle East & Africa region accounts for around 10% of the market, with strong demand in countries such as the UAE and Saudi Arabia. The region’s growth is primarily driven by a deep cultural affinity for fragrances, high per capita spending on luxury products, and a preference for strong, long-lasting scents such as oud and oriental blends. The presence of affluent consumers and a thriving luxury retail sector further supports market expansion. In Africa, the market is gradually growing due to increasing urbanization, rising disposable incomes, and improving awareness of personal grooming products. The expansion of retail infrastructure and the entry of international brands are expected to further accelerate growth across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Men Perfume Market

- LVMH

- L’Oréal Group

- Estée Lauder Companies

- Coty Inc.

- Chanel

- Puig

- Shiseido Company

- Hermès

- Kering Beauté

- Inter Parfums

- Amorepacific

- Beiersdorf

- Revlon

- Avon Products

- Elizabeth Arden