Mechanical Keyboard Market Size

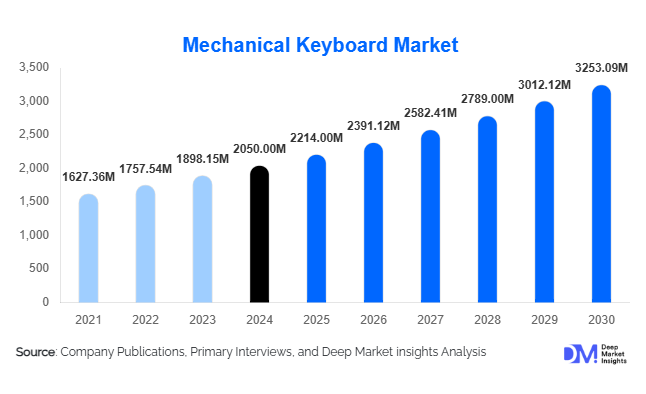

According to Deep Market Insights, the global mechanical keyboard market size was valued at USD 2,050 million in 2025 and is projected to grow from USD 2,214 million in 2026 to reach USD 3,253.09 million by 2031, expanding at a CAGR of 8% during the forecast period (2026–2031). The mechanical keyboard market growth is primarily driven by increasing demand from gaming and professional sectors, technological advancements in switch mechanisms and connectivity, and a rising preference for ergonomic, customizable input devices among consumers worldwide.

Key Market Insights

- Mechanical keyboards are increasingly becoming mainstream beyond gaming, driven by adoption in professional and creative work environments seeking durability, comfort, and productivity-enhancing features.

- Gaming remains the largest end-use segment globally, with gamers and esports enthusiasts demanding high-performance switches, low-latency connectivity, and RGB lighting customization.

- Asia-Pacific is emerging as a critical growth region, led by China, Japan, and South Korea, due to strong gaming culture, esports expansion, and rising middle-class consumer spending.

- Technological innovation continues to shape the market, including wireless mechanical keyboards, Hall effect switches, modular designs, and programmable keys.

- Customization and modularity are key trends, with hot-swappable switches, programmable macros, and personalized keycap sets driving consumer engagement.

- North America dominates in high-end mechanical keyboard adoption, driven by professional and gaming applications in the U.S. and Canada.

Mechanical Keyboard Market latest trends

Gaming and Professional Adoption Driving Growth

The demand for mechanical keyboards is heavily fueled by the gaming industry and hybrid work models. Esports, streaming, and competitive gaming require low-latency, durable keyboards with tactile feedback. Professionals in the IT, design, and programming sectors are increasingly adopting mechanical keyboards for ergonomic benefits and typing efficiency. As hybrid work becomes mainstream, the shift toward productivity-focused peripherals has expanded mechanical keyboards’ appeal beyond traditional gamers, creating a broader market for premium, durable input devices.

Customization and Modularity Trend

Consumers are demanding fully customizable keyboards. Features such as hot-swappable switches, programmable macros, and RGB lighting allow users to tailor keyboards to personal preferences. Modularity, including replaceable keycaps and switch types, is gaining traction among enthusiasts and professionals, boosting engagement and brand loyalty. This trend is shaping product development strategies, particularly in premium segments targeting high-end users who value personalization and longevity.

Mechanical Keyboard Market key drivers

Rising Gaming and Esports Popularity

The expanding global gaming industry is the primary driver for mechanical keyboards. Competitive gaming and esports require precision, tactile feedback, and fast response times, favoring mechanical switches over membrane alternatives. Gaming peripherals with RGB lighting, wireless connectivity, and ergonomic layouts have become standard, enhancing demand in both mature and emerging gaming markets.

Hybrid Work and Professional Usage

The adoption of hybrid and remote work models has led to increased investment in ergonomic and efficient computing peripherals. Professionals in IT, content creation, programming, and creative industries increasingly prefer mechanical keyboards for typing comfort, durability, and productivity. This trend is expected to sustain steady growth in the professional segment globally.

Technological Advancements in Switches and Connectivity

Innovations such as Hall effect switches, wireless low-latency connectivity, and RGB-customizable key mechanisms have broadened mechanical keyboard appeal. Wireless mechanical keyboards, in particular, address convenience without compromising performance, while advanced switches enhance durability and user satisfaction. Such technological differentiation is helping brands expand market share in both gaming and professional sectors.

Mechanical Keyboard Market restraints

High Cost Compared to Membrane Keyboards

Mechanical keyboards are typically more expensive than traditional membrane keyboards, which can deter cost-sensitive consumers. While premium models offer advanced features and durability, the upfront investment remains a barrier for mass adoption in some regions, particularly in emerging markets.

Noise Levels of Key Switches

The audible keypress sound of mechanical keyboards can be disruptive in shared or quiet office environments. Although silent switch variants are available, noise remains a limiting factor for widespread professional adoption, particularly in open-plan workspaces.

Mechanical Keyboard Market key opportunities

Emerging Markets Expansion

Regions such as Asia-Pacific and Latin America present significant growth opportunities. Increasing gaming culture, esports participation, and higher disposable income in countries like China, India, Brazil, and Mexico are driving demand for mechanical keyboards. Expanding distribution networks and localized marketing strategies can help global players capitalize on these emerging markets.

Integration of Advanced Switch Technologies

The adoption of Hall effect, optical, and hybrid switches provides opportunities for differentiation. These technologies offer enhanced durability, faster response, and customizable tactile experiences. Companies integrating such technologies can appeal to gamers and professionals seeking high-performance keyboards, increasing brand loyalty and premium product adoption.

Customization and Personalization

Offering hot-swappable switches, programmable macros, and custom keycaps enables brands to attract enthusiasts and professional users who value personalization. This trend also encourages repeat purchases and accessories sales, creating additional revenue streams and expanding market potential.

Product Type Insights

Linear switches dominate the market, accounting for approximately 45.2% of 2025sales due to their smooth keystroke, quiet operation, and gaming-friendly performance. Tactile and clicky switches are popular among professionals and typing enthusiasts seeking feedback and accuracy. Full-size keyboards remain the leading form factor, catering to both gaming and professional use with complete key layouts, including number pads and function keys. Wireless connectivity is rapidly growing, particularly in high-end products, as users seek clutter-free setups without latency compromises.

Application Insights

The gaming sector is the largest end-use segment, followed by the professional and creative industries. Gaming keyboards dominate due to esports and streaming trends, while professional segments value ergonomic, durable keyboards for extended typing sessions. Emerging applications include hybrid setups for remote work, content creation, and digital design, as well as new adoption in niche sectors such as financial trading and programming bootcamps. Export-driven demand is high from North America and Europe, sourcing high-performance keyboards from Asia-Pacific manufacturers.

Distribution Channel Insights

Online retail platforms, including e-commerce and brand direct-to-consumer websites, dominate mechanical keyboard sales. Physical electronics stores continue to cater to casual consumers, while specialty gaming and enthusiast shops support high-end models. Online communities, social media, and influencer reviews increasingly influence purchasing decisions, particularly among gamers and younger demographics. Subscription-based or membership models are emerging, offering exclusive access to limited-edition products and custom configurations.

Traveler Type Insights

Not applicable for this market; instead, consumer type segmentation focuses on gamers, professionals, and enthusiasts. Gamers represent the largest share, professionals and remote workers are growing steadily, and keyboard enthusiasts drive premium and modular product adoption.

Age Group Insights

Consumers aged 18–35 years drive growth in gaming and enthusiast segments, seeking performance and customization. Professionals aged 31–50 years contribute to premium keyboard adoption for ergonomic and productivity purposes. Older demographics (51+ years) are slowly entering high-end and silent-switch mechanical keyboards, mainly for professional or typing-intensive use.

| By Switch Type | By Application | By Distribution |

|---|---|---|

|

|

|

Regional Insights

North America

North America is a leading market, with the U.S. accounting for a major share due to high gaming engagement and professional adoption. Wired and premium mechanical keyboards dominate, with approximately 35% of global market share in 2025. Canada contributes steadily, driven by remote work trends and gaming culture.

Europe

Europe, led by Germany and the U.K., represents the second-largest region, with rising demand for ergonomic and customizable keyboards. The region contributes roughly 28% of the global market share in 2025. Younger demographics in Europe are driving growth in RGB-enabled and modular keyboards.

Asia-Pacific

China, Japan, and South Korea are key contributors to market expansion. Rising esports, gaming culture, and online streaming platforms fuel demand for high-performance keyboards. APAC is also the fastest-growing region, expected to surpass Europe by 2027 in terms of annual growth rate.

Latin America

Brazil and Mexico are emerging markets for gaming keyboards. Growing esports adoption and increasing internet penetration are driving gradual growth in high-performance keyboard demand.

Middle East & Africa

The UAE, Saudi Arabia, and South Africa are key markets, focusing on premium and gaming keyboards. Rising disposable income and gaming culture are expanding regional demand, although total volume remains smaller than in North America and Europe.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Mechanical Keyboard Market

- Logitech

- Razer

- Corsair

- SteelSeries

- HyperX

- Keychron

- Cooler Master

- ASUS

- MSI

- Redragon

- Ducky

- Fnatic

- G.Skill

- Bloody Gaming

- Akko