Meat Tenderizer Market Size

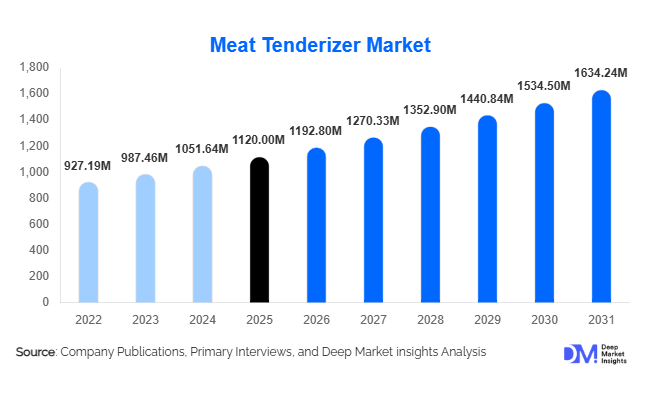

According to Deep Market Insights, the global meat tenderizer market size was valued at USD 1,120 million in 2025 and is projected to grow from USD 1,192.80 million in 2026 to reach USD 1,634.24 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The meat tenderizer market is experiencing growth primarily driven by the rising demand for ready-to-cook and marinated meat products, the increasing adoption of mechanized and chemical tenderization methods, and the growth in the commercial foodservice and meat processing sectors across the globe.

Key Market Insights

- Mechanical tenderizers dominate the product landscape, particularly in commercial and processing applications, due to precision, safety, and uniform meat texture.

- Powdered chemical tenderizers are widely adopted in households and small-scale foodservice operations for convenience, controlled dosing, and longer shelf life.

- North America holds the largest share of the meat tenderizer market, led by the U.S. and Canada, driven by processed meat consumption and foodservice demand.

- Asia-Pacific is the fastest-growing region, with China, India, and Japan contributing significantly due to urbanization, rising disposable income, and western-style diet adoption.

- Offline retail remains the dominant distribution channel, although online e-commerce platforms are increasingly capturing urban and tech-savvy consumer segments.

- Technological integration, including smart mechanical tenderizers and hybrid enzyme-mechanical solutions, is enhancing efficiency, consistency, and adoption across commercial kitchens and meat processing plants.

What are the latest trends in the meat tenderizer market?

Hybrid and Smart Tenderization Solutions

Manufacturers are increasingly integrating mechanical and chemical tenderization methods to deliver uniform meat texture with faster processing times. Smart tenderizers equipped with sensors, IoT connectivity, and adjustable pressure settings are becoming popular in commercial kitchens and meat processing units, ensuring precise, repeatable results. These innovations not only reduce wastage and improve efficiency but also enable predictive maintenance, helping operators optimize equipment utilization. Hybrid solutions are particularly attractive in ready-to-cook and packaged meat industries where quality consistency is critical for global exports.

Growing Adoption of Enzyme-Based Tenderizers

Chemical tenderizers containing enzymes like bromelain, papain, and ficin are increasingly preferred for household and small-scale foodservice use. These products simplify meat preparation, shorten cooking time, and enhance tenderness without altering flavor. The trend is especially pronounced in urban areas and emerging markets, where consumers are seeking convenience in home cooking, and small restaurants are adopting enzyme tenderizers to maintain consistent meat quality.

What are the key drivers in the meat tenderizer market?

Rising Demand for Processed and Ready-to-Cook Meat

The global appetite for ready-to-cook, marinated, and frozen meat products is fueling meat tenderizer demand. Foodservice establishments, catering companies, and meat processors require consistent tenderness and texture, which drives the adoption of both mechanical and chemical tenderizers. The growth of convenience-oriented consumption patterns in urban households further accelerates this trend.

Technological Advancements in Tenderizers

Advanced mechanical tenderizers, including blade, needle, and mallet-based solutions, have improved safety, speed, and uniformity. Automation and smart controls in these systems reduce labor requirements, minimize product waste, and ensure consistent output, making them appealing to large-scale meat processors and commercial kitchens.

Urbanization and Lifestyle Changes

Busy lifestyles in urban regions are creating a higher demand for convenient cooking tools. Meat tenderizers that save time, improve flavor, and deliver predictable results are increasingly popular in both household and commercial settings, boosting overall market growth.

What are the restraints for the global market?

High Initial Costs for Advanced Tenderizers

Automated and hybrid mechanical tenderizers involve significant upfront investments, which can deter smaller restaurants, households, and emerging market users from adoption. This cost barrier limits the widespread penetration of technologically advanced solutions.

Regulatory Restrictions on Chemical Tenderizers

Enzyme-based tenderizers face strict regulatory limits in certain countries, including maximum allowed concentrations and labeling requirements. Compliance increases operational costs and can restrict market entry, particularly for new entrants in regulated regions.

What are the key opportunities in the meat tenderizer industry?

Expansion in Emerging Markets

Regions like APAC and LATAM offer high growth potential due to increasing meat consumption, urbanization, and rising disposable income. Affordable, user-friendly tenderizers for households and small restaurants can capture this growing demand. For instance, packaged enzyme powders and compact mechanical devices are expected to see strong uptake in India and Brazil.

Integration of Smart and Automated Solutions

Commercial kitchens and meat processing plants are increasingly seeking smart tenderizers that offer precise control, uniform quality, and predictive maintenance features. Companies investing in R&D for IoT-enabled tenderizers can gain a competitive edge by reducing wastage, improving efficiency, and providing consistent results at scale.

Government and Local Manufacturing Initiatives

Programs like “Make in India” and “Made in China 2026” support domestic manufacturing and the modernization of food processing equipment. Companies can leverage these initiatives to expand production capacities, benefit from tax incentives, and develop products compliant with international safety standards for exports.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1120 Million |

| Market Size in 2026 | USD 1192.80 Million |

| Market Size in 2031 | USD 1634.24 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Mechanical tenderizers dominate the global market, accounting for approximately 45% of the 2025 market share. Their leadership is driven by precision, reliability, and wide acceptance in both commercial kitchens and meat processing plants, where consistent texture and reduced cooking time are critical. Powdered enzyme-based tenderizers hold around 35% market share, favored for convenience, long shelf life, and ease of use in household and small-scale foodservice applications. Hybrid solutions, which combine mechanical action with enzymatic tenderization, are emerging as premium offerings for commercial kitchens and industrial meat processing. These hybrids are gaining traction because they ensure uniform tenderness while improving operational efficiency, addressing the growing demand from large-scale production and ready-to-cook meat sectors. The rising trend of automation and smart tenderization solutions further reinforces mechanical tenderizers as the leading product type.

Application Insights

The commercial foodservice segment is the largest application, accounting for roughly 40% of the market. Restaurants, hotels, and catering services rely heavily on tenderizers to maintain consistent meat quality, texture, and flavor, especially in high-volume operations. Household use is steadily expanding, particularly in urban centers, where consumers increasingly prefer ready-to-cook and convenience-focused meal preparation. Meanwhile, the meat processing and packaging industry is witnessing robust growth due to the demand for frozen and pre-marinated meat products, which require large-scale uniform tenderization. The growth in foodservice and processing applications is further supported by automation trends, hybrid tenderizer adoption, and increasing consumer awareness of meat quality standards, highlighting the interconnection between product type and application adoption.

Distribution Channel Insights

Offline retail channels, including supermarkets, hypermarkets, and specialty kitchenware stores, hold a dominant 55% market share, providing consumers with trusted purchase points and in-store guidance. Online platforms are rapidly growing, particularly in urban areas, due to e-commerce adoption and convenience, allowing consumers to compare products, access reviews, and receive doorstep delivery. For commercial and industrial applications, B2B supply channels are critical, enabling bulk sales to restaurants, hotels, and meat processing plants. Emerging trends such as subscription-based models, direct-to-business sales, and smart device bundling are driving market penetration, particularly in industrial and commercial segments, while reinforcing the adoption of high-end mechanical and hybrid tenderizers.

End-Use Insights

The meat processing and packaging industry leads demand, accounting for approximately 38% of the global market. The need for uniform meat texture, consistent flavor, and reliable production timelines in frozen and ready-to-cook products drives tenderizer adoption. Foodservice establishments, including restaurants and catering services, are expanding their use of mechanical and chemical tenderizers to ensure quality and operational efficiency. Residential kitchens show steady growth, fueled by compact mechanical devices and enzyme-based tenderizers for convenience cooking. Export-oriented markets, including the U.S., Japan, and EU countries, further amplify industrial demand, as these regions emphasize quality standards and uniformity in meat imports. Growth in ready-to-cook and frozen meat consumption globally continues to support all end-use segments, highlighting the cross-influence of product type, application, and distribution channels.

Explore more data points, trends and opportunities Download Free Sample Report

Meat Tenderizer Market Segmentations

By Product Type

- Mechanical Tenderizers

- Powdered Enzyme-Based Tenderizers

- Hybrid Tenderizers

By Application

- Commercial Foodservice

- Household Use

- Meat Processing & Packaging

By Distribution Channel

- Offline Retail

- Online Platforms

- B2B Supply Channels

- Subscription-Based & Direct-to-Business Models

Regional Insights

North America

North America holds approximately 32% of the market in 2025, with the U.S. and Canada leading consumption. Drivers include high consumption of processed meat, advanced foodservice infrastructure, and a strict regulatory focus on food safety and quality. Adoption of advanced mechanical and chemical tenderizers in meat processing plants is high due to automation trends and efficiency requirements in commercial kitchens. Additionally, increasing consumer preference for ready-to-cook meals and frozen meat products is boosting demand across both industrial and household segments.

Europe

Europe accounts for around 28% of the global market, with Germany, France, and the U.K. as major contributors. The region is driven by strong consumer preference for premium and high-quality meat products, the widespread adoption of automated processing technologies, and rigorous food safety regulations. Hybrid tenderizers combining mechanical and chemical processes are gaining traction in commercial kitchens, enabling foodservice providers to maintain consistency and improve operational efficiency. Rising demand in processed meat and frozen meals across Western Europe further fuels regional growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR of around 8%, led by China, India, and Japan. Drivers include rapid urbanization, rising disposable incomes, and a shift toward Western-style diets, leading to higher meat consumption per capita. Growth is also propelled by expanding foodservice sectors, including quick-service restaurants, hotels, and catering companies, alongside increasing household adoption of enzyme-based tenderizers for convenience cooking. Government initiatives supporting food processing modernization and improving cold chain infrastructure are also contributing significantly to regional expansion.

Latin America

Brazil and Argentina are the largest contributors in Latin America, where the market is primarily driven by meat processing and export-oriented production. High consumption of beef and other meats, coupled with an increasing number of industrial meat processing plants, fuels demand for both mechanical and chemical tenderizers. Growing outbound meat exports to North America and Europe encourage the adoption of advanced tenderization technologies to meet international quality standards. Additionally, urban expansion and rising disposable incomes are gradually increasing household and foodservice adoption.

Middle East & Africa

The Middle East, led by the UAE, Saudi Arabia, and Qatar, is emerging as a high-income consumer market for premium tenderizers, driven by disposable income, rising foodservice sophistication, and increased consumption of processed and frozen meat products. Africa remains a key production region for raw meats, where growing domestic consumption and expansion of commercial meat processing plants are driving adoption. Government investment in industrial food processing and modernization of cold chain infrastructure further supports regional market growth. The convergence of high-income urban centers and expanding industrial meat processing creates unique opportunities for premium and hybrid tenderizer solutions.

Key Players in the Meat Tenderizer Market

- JBS S.A.

- Tyson Foods, Inc.

- Smithfield Foods, Inc.

- Cargill, Inc.

- Hormel Foods Corporation

- Maple Leaf Foods

- Marfrig Global Foods

- BRF S.A.

- Perdue Farms

- OSI Group

- NH Foods Ltd.

- Danish Crown

- Minerva Foods

- Seaboard Foods

- Keystone Foods