Measuring Cups & Spoons Market Size

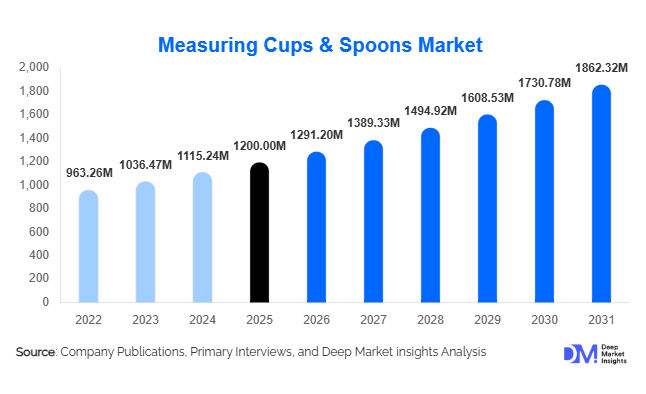

According to Deep Market Insights, the global measuring cups & spoons market size was valued at USD 1,200 million in 2025 and is projected to grow from USD 1,291.20 million in 2026 to reach USD 1,862.32 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The market growth is primarily driven by the rising popularity of home cooking and baking, increasing demand for precision in food preparation, and the expansion of the global foodservice industry. Growing consumer awareness regarding portion control, coupled with the influence of digital cooking content and social media, is further accelerating adoption across both residential and commercial segments.

Key Market Insights

- Home cooking and baking trends are significantly boosting demand, with consumers increasingly relying on precise measurement tools for consistent results.

- Stainless steel measuring tools are gaining popularity due to durability, safety, and premium appeal over plastic alternatives.

- Asia-Pacific dominates the global market, supported by large-scale manufacturing and rising domestic consumption.

- Online retail channels are witnessing the fastest growth, driven by convenience, product variety, and competitive pricing.

- Commercial kitchens and cloud kitchens are expanding rapidly, increasing demand for standardized measuring tools.

- Sustainability trends are reshaping product innovation, with eco-friendly materials and recyclable packaging gaining traction.

What are the latest trends in the measuring cups & spoons market?

Shift Toward Premium and Durable Materials

Consumers are increasingly shifting from low-cost plastic measuring tools to premium materials such as stainless steel and silicone. This transition is driven by concerns regarding food safety, durability, and environmental impact. Stainless steel products, in particular, offer resistance to corrosion and long-term usability, making them highly preferred in both residential and commercial kitchens. Manufacturers are also introducing aesthetically appealing designs with polished finishes and engraved measurement markings to enhance product longevity and usability. This trend is especially prominent in developed markets where consumers are willing to pay a premium for quality and sustainability.

Growth of E-commerce and Digital Influence

The rapid expansion of e-commerce platforms is transforming the distribution landscape of measuring cups and spoons. Consumers now have access to a wide variety of products, including international brands and innovative designs, through online marketplaces. Social media platforms and cooking influencers are playing a crucial role in shaping consumer preferences, often promoting specific product types or brands. Product bundling, discounts, and customer reviews available online are further influencing purchasing decisions. This digital shift is particularly strong among younger consumers and urban households, making online retail the fastest-growing channel in the market.

What are the key drivers in the measuring cups & spoons market?

Rising Home Cooking and Baking Culture

The increasing popularity of home cooking and baking is a primary driver of market growth. Consumers are experimenting with diverse cuisines and recipes that require precise ingredient measurements, boosting demand for measuring tools. The influence of cooking shows, online tutorials, and social media platforms has significantly contributed to this trend. Additionally, the shift toward healthier eating habits has encouraged individuals to prepare meals at home, further supporting market expansion.

Expansion of the Global Foodservice Industry

The rapid growth of restaurants, bakeries, and cloud kitchens is driving demand for measuring cups and spoons in commercial settings. These establishments rely on standardized measurements to maintain consistency in food quality and taste. The increasing number of quick-service restaurants and food delivery services is further accelerating demand for professional-grade measuring tools, particularly in urban areas.

Product Innovation and Functional Design Improvements

Manufacturers are continuously innovating to enhance product functionality and user convenience. Features such as adjustable measuring tools, dual measurement systems (metric and imperial), stackable designs, and magnetic handles are gaining popularity. These innovations not only improve usability but also differentiate products in a competitive market, attracting both new and repeat customers.

What are the restraints for the global market?

Availability of Low-Cost Unbranded Products

The presence of low-cost, unbranded measuring tools in developing markets poses a significant challenge for established manufacturers. These products are often sold at significantly lower prices, making it difficult for branded players to compete, especially in price-sensitive regions. This leads to reduced profit margins and market fragmentation.

Long Product Replacement Cycle

Measuring cups and spoons are durable products with long lifespans, resulting in infrequent replacement purchases. Unlike consumable kitchen items, these tools do not require frequent repurchasing, which limits volume growth in mature markets. This factor slows down overall market expansion despite steady demand from new consumers.

What are the key opportunities in the measuring cups & spoons industry?

Smart Kitchen Integration

The emergence of smart kitchens presents a significant opportunity for innovation in measuring tools. Products integrated with digital sensors and mobile applications can provide real-time measurement conversions, nutritional insights, and enhanced accuracy. Such advanced solutions are expected to attract tech-savvy consumers and premium buyers, particularly in developed markets.

Expansion in Emerging Markets

Emerging economies in Asia-Pacific and Latin America offer substantial growth potential due to rising disposable incomes, urbanization, and increasing exposure to global cuisines. Governments promoting small food businesses and entrepreneurship are indirectly boosting demand for standardized kitchen tools. Manufacturers can capitalize on this opportunity by offering affordable and localized product ranges.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1200.00 Million |

| Market Size in 2026 | USD 1291.20 Million |

| Market Size in 2031 | USD 1862.32 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Combined measuring cup and spoon sets dominate the global measuring tools market, accounting for approximately 38% of the total market share in 2025. The leadership of this segment is primarily driven by its ability to offer an all-in-one, cost-efficient, and highly practical solution for both novice and experienced users. Consumers increasingly prefer bundled kitchenware products that simplify purchasing decisions and reduce overall expenditure, particularly in price-sensitive and space-constrained households. The growing trend of modular and compact kitchen designs has further accelerated the adoption of stackable and nesting sets that optimize storage efficiency. Additionally, manufacturers are innovating with ergonomic designs, engraved measurement markings for durability, and aesthetically appealing finishes, which enhance product usability and longevity. The expansion of home cooking trends, influenced by digital platforms and culinary content, has also significantly boosted demand for these integrated measuring solutions, making them a staple in modern kitchens across both developed and emerging markets.

Material Insights

Stainless steel leads the material segment with an estimated 34% market share in 2025, supported by its superior durability, corrosion resistance, and premium visual appeal. The leading position of this segment is largely attributed to the increasing consumer shift away from plastic products due to concerns related to chemical leaching, environmental sustainability, and long-term usability. Stainless steel measuring tools are widely regarded as a long-term investment, particularly in commercial and professional kitchens where frequent use demands high-performance materials. In addition, the ease of cleaning, dishwasher compatibility, and resistance to staining further enhance their suitability for both residential and foodservice environments. Growing awareness regarding food safety standards and hygiene has also reinforced demand for metal-based measuring tools, especially in regulated markets. Furthermore, the rising popularity of premium kitchenware products, particularly in developed economies, continues to drive the adoption of stainless steel across multiple end-use segments.

Capacity Insights

Medium-capacity measuring tools ranging from 100 to 500 ml hold the largest share at approximately 42% of the global market in 2025. The dominance of this segment is primarily driven by its versatility and applicability across a wide range of cooking and baking requirements. These measuring tools strike an optimal balance between precision and practicality, making them suitable for everyday household use as well as professional culinary applications. Their widespread adoption is further supported by their compatibility with diverse recipes and portion sizes, reducing the need for multiple measuring tools. Additionally, the growing trend of standardized recipes and portion-controlled meal preparation has reinforced the demand for medium-capacity tools that ensure accuracy and consistency. The segment also benefits from increasing demand in the foodservice industry, where efficiency and flexibility in ingredient measurement are critical for operational productivity.

End-Use Insights

The residential segment dominates the market, accounting for nearly 55% of the total market share in 2025, driven by evolving consumer lifestyles and a strong resurgence in home-based culinary activities. The leading position of this segment is largely fueled by the increasing popularity of home cooking, baking, and health-conscious meal preparation, particularly in the post-pandemic era. Consumers are increasingly focusing on portion control, nutritional accuracy, and experimentation with global cuisines, all of which require precise measuring tools. The rapid proliferation of digital cooking platforms, social media influencers, and online recipe content has significantly influenced consumer behavior, encouraging more individuals to invest in quality kitchenware. Moreover, rising disposable incomes and the growing trend of kitchen renovation and modernization have further contributed to the expansion of the residential segment, making it the primary driver of overall market demand.

Distribution Channel Insights

Offline retail channels continue to dominate the market with around 60% market share in 2025, supported by their established presence across supermarkets, hypermarkets, and specialty kitchenware stores. The leading position of this segment is driven by consumers’ preference for physically evaluating product quality, material, and usability before purchase. In-store promotions, brand visibility, and immediate product availability also contribute to sustained demand through offline channels. However, the rapid expansion of e-commerce platforms is reshaping the competitive landscape, with online channels gaining significant traction due to their convenience, competitive pricing, and extensive product variety. The integration of user reviews, product comparisons, and doorstep delivery services has enhanced consumer confidence in online purchases. As digital penetration continues to increase globally, the market is expected to witness a gradual shift toward omnichannel retail strategies, where both offline and online platforms complement each other to maximize consumer reach.

Price Range Insights

Mid-range products dominate the pricing segment, accounting for approximately 48% of the global market in 2025. The leadership of this segment is primarily driven by its ability to offer an optimal balance between affordability and quality, catering to a broad consumer base across diverse income groups. These products typically provide durable materials, reliable measurement accuracy, and modern designs without the premium price tag, making them highly attractive for both residential users and small-scale commercial establishments. The segment also benefits from increasing consumer awareness regarding product quality and long-term value, prompting a shift away from low-cost, short-lived alternatives. While premium products are gaining traction in developed markets due to rising demand for high-end kitchenware, economy products continue to maintain relevance in price-sensitive regions. However, the mid-range segment remains the most resilient and widely adopted category, supported by its versatility and strong value proposition.

Explore more data points, trends and opportunities Download Free Sample Report

Measuring Cups & Spoons Market Segmentations

By Product Type

- Measuring Cups

- Measuring Spoons

- Combined Sets

By Material

- Plastic

- Metal

- Glass

- Silicone

- Ceramic

By Capacity

- Small Capacity

- Medium Capacity

- Large Capacity

By End-Use

- Residential

- Commercial

- Institutional

By Distribution Channel

- Online Retail

- Offline Retail

By Price Range

- Economy

- Mid-Range

- Premium

Regional Insights

North America

North America holds approximately 28% of the global market share in 2025, driven by strong consumer purchasing power and a deeply ingrained culture of home cooking and baking. The United States leads regional demand, supported by high adoption of premium kitchenware products and increasing consumer interest in culinary experimentation. Market growth in this region is further driven by the widespread influence of cooking shows, digital recipe platforms, and celebrity chefs, which encourage consumers to invest in high-quality measuring tools. Additionally, the presence of well-established retail infrastructure and leading kitchenware brands enhances product accessibility and availability. Growing awareness of food portion control and dietary management also contributes to sustained demand. The rising trend of smart kitchens and technologically advanced kitchen tools is expected to further support market expansion in the region.

Europe

Europe accounts for nearly 24% of the global market share, with key countries such as Germany, the United Kingdom, and France leading demand. The regional market is strongly influenced by stringent regulations related to food safety, material quality, and environmental sustainability, which have encouraged the adoption of high-quality and certified measuring tools. Consumers in Europe demonstrate a strong preference for eco-friendly and reusable products, driving demand for stainless steel and other sustainable materials. The region also benefits from a well-established culinary tradition and a high level of cooking proficiency among consumers, which supports consistent demand for precise measuring instruments. Furthermore, the growing trend of premium kitchenware and designer products, particularly in Western Europe, continues to contribute to market growth, alongside increasing adoption of online retail channels.

Asia-Pacific

Asia-Pacific dominates the global market with approximately 32% share in 2025 and represents the fastest-growing region. Major economies such as China and India are key contributors, driven by rapid urbanization, expanding middle-class populations, and rising disposable incomes. The increasing penetration of modern retail formats and e-commerce platforms has significantly improved product accessibility across urban and semi-urban areas. Additionally, the growing influence of Western cooking practices and baking trends is accelerating demand for measuring tools in the region. Countries such as Japan and South Korea contribute through strong demand for premium, innovative, and aesthetically designed kitchenware products. The region’s robust manufacturing base also plays a critical role in supporting both domestic consumption and global exports, making Asia-Pacific a central hub in the global supply chain. The expansion of the foodservice industry and increasing number of quick-service restaurants further amplify regional demand.

Latin America

Latin America accounts for around 8% of the global market, led by countries such as Brazil and Mexico. Market growth in this region is primarily driven by rising disposable incomes, improving living standards, and increasing interest in home cooking and baking activities. The gradual shift toward modern kitchen practices and tools is supporting the adoption of measuring equipment across households. Additionally, the expansion of organized retail networks and growing penetration of e-commerce platforms are enhancing product availability. Cultural influences, including traditional cooking practices and family-oriented meal preparation, also contribute to consistent demand. As urbanization continues and consumer awareness increases, the region is expected to witness steady growth in the adoption of advanced and durable kitchen tools.

Middle East & Africa

The Middle East & Africa region holds approximately 8% of the global market share, with growth driven by rapid urbanization and the expansion of the hospitality and tourism sectors. Countries such as the UAE and Saudi Arabia are witnessing significant demand due to increasing investments in hotels, restaurants, and catering services. The rising influx of international tourists has further boosted the need for standardized and high-quality kitchen tools in the foodservice industry. Additionally, increasing disposable incomes and the growing adoption of modern lifestyles are encouraging consumers to invest in better kitchenware products. The region also benefits from strong import activities, with a large proportion of measuring tools sourced from global manufacturing hubs. As retail infrastructure continues to develop and consumer awareness rises, the market is expected to experience gradual but sustained growth.

Key Players in the Measuring Cups & Spoons Market

- OXO International Ltd.

- Newell Brands Inc.

- Lifetime Brands Inc.

- Groupe SEB

- Tupperware Brands Corporation

- KitchenAid (Whirlpool Corporation)

- Cuisipro

- Norpro Inc.

- Progressive International

- Trudeau Corporation

- Joseph Joseph Ltd.

- Zyliss

- WMF Group

- Brabantia

- Rubbermaid Commercial Products