Mattress Topper Market Size

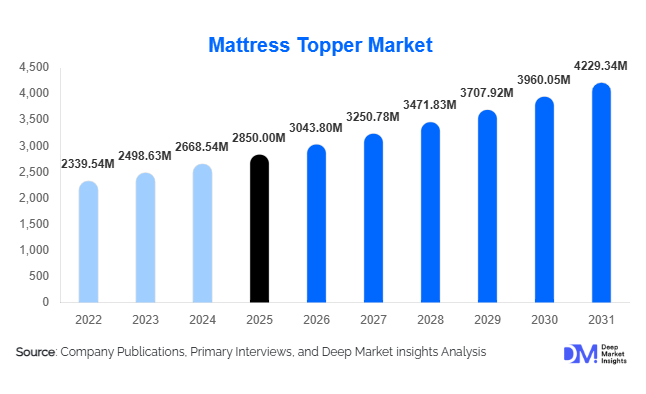

According to Deep Market Insights, the global mattress topper market size was valued at USD 2,850 million in 2025 and is projected to grow from USD 3,043.80 million in 2026 to reach USD 4,229.34 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The mattress topper market growth is primarily driven by rising consumer awareness regarding sleep health, increasing demand for cost-effective bedding upgrades, and the rapid expansion of online direct-to-consumer (DTC) sleep brands. Growing urbanization, higher disposable income, and the revival of the hospitality industry are further strengthening global demand. Consumers increasingly prefer mattress toppers as an affordable alternative to full mattress replacement, especially in mid-range and premium housing segments.

Key Market Insights

- Memory foam toppers dominate the market, accounting for nearly 42% of global revenue in 2025 due to superior pressure relief and orthopedic benefits.

- Online distribution channels lead with over 55% share, driven by DTC brands, compression packaging innovations, and attractive return policies.

- North America holds the largest regional share (34%), supported by high consumer spending and strong brand penetration.

- Asia-Pacific is the fastest-growing region, expanding at nearly 8% CAGR due to urban housing growth and rising middle-class income.

- Residential applications account for nearly 78% of demand, reflecting growing home comfort upgrades and mattress lifespan extension trends.

- The mid-range price segment leads with 47% share, offering an optimal balance between affordability and durability.

What are the latest trends in the mattress topper market?

Cooling and Temperature-Regulating Technologies

Temperature regulation has become a primary purchase consideration among consumers. Gel-infused memory foam, phase-change materials (PCM), breathable bamboo covers, and moisture-wicking fabrics are increasingly integrated into mattress toppers to address heat retention issues. Brands are focusing on airflow channel designs and open-cell foam technologies to enhance cooling performance. This trend is particularly strong in North America and Asia-Pacific, where consumers are willing to pay a premium for improved sleep comfort. Cooling toppers often command 15–20% higher average selling prices compared to standard variants, reinforcing margin expansion opportunities for manufacturers.

Sustainable and Organic Material Adoption

Eco-conscious consumers are shifting toward natural latex, organic cotton, and wool-based mattress toppers. Certifications related to chemical safety and textile sustainability significantly influence buying decisions in Europe and North America. Manufacturers are investing in bio-based polyurethane alternatives and recyclable packaging to meet tightening environmental regulations. The premium organic segment is expanding steadily, especially in Germany, the U.K., and the U.S., where sustainability-driven purchasing behavior is shaping bedding product development strategies.

What are the key drivers in the mattress topper market?

Growing Focus on Sleep Health and Wellness

Rising global awareness regarding spinal health, pressure relief, and sleep quality is significantly driving mattress topper adoption. Consumers increasingly view toppers as ergonomic enhancements that improve mattress support without requiring full replacement. Orthopedic recommendations and digital health awareness campaigns have contributed to rising adoption rates, especially among working professionals and aging populations.

E-Commerce Expansion and DTC Growth

The rapid growth of online retail has transformed mattress topper distribution. Brands leverage direct-to-consumer models to offer competitive pricing, extended trial periods, and bundled sleep accessories. Compression roll-pack packaging has reduced logistics costs, enabling cross-border exports from manufacturing hubs in China and Vietnam to North America and Europe. Online reviews and social media marketing continue to influence purchasing decisions.

What are the restraints for the global market?

Raw Material Price Volatility

Polyurethane foam and synthetic latex depend on petrochemical derivatives, making production costs vulnerable to crude oil price fluctuations. Sudden input cost increases impact margins, particularly in the economy and mid-range segments where pricing flexibility is limited.

Substitution by Advanced Hybrid Mattresses

Growing adoption of high-end hybrid mattresses with integrated pillow tops and built-in cooling layers reduces incremental demand for aftermarket mattress toppers. In premium markets, shorter mattress replacement cycles may limit long-term topper growth.

What are the key opportunities in the mattress topper industry?

Hospitality and Institutional Expansion

Rising investments in hotels, serviced apartments, hospitals, and student housing present bulk procurement opportunities. Commercial-grade mattress toppers with antimicrobial and fire-retardant features are witnessing growing demand. Countries such as India, Saudi Arabia, and the United Arab Emirates are expanding hospitality infrastructure, creating consistent large-scale purchasing demand.

Smart and Sensor-Integrated Sleep Solutions

Integration of sleep tracking sensors and IoT-based monitoring technologies into mattress toppers is emerging as a niche premium segment. Partnerships between bedding manufacturers and sleep-tech companies are enabling real-time sleep data analysis, appealing to tech-savvy consumers seeking optimized rest environments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2850 Million |

| Market Size in 2026 | USD 3043.80 Million |

| Market Size in 2031 | USD 4229.34 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Memory foam dominates the global mattress topper market with approximately 42% revenue share in 2025, maintaining leadership due to its superior contouring ability, motion isolation, and pressure-relief performance. The primary growth driver for this segment is rising consumer awareness regarding orthopedic health and spinal alignment. Increasing cases of back pain among working professionals and aging populations have strengthened demand for viscoelastic foam solutions that distribute body weight evenly and reduce pressure points. Additionally, technological advancements such as gel infusion, open-cell structures, and copper- or graphite-infused memory foam have improved breathability and temperature regulation, addressing historical heat retention concerns.

Latex toppers are gaining traction in Europe and premium U.S. segments, supported by the growing preference for natural, durable, and hypoallergenic bedding materials. Sustainability certifications and eco-conscious purchasing behavior are accelerating the adoption of natural latex products. Polyester fiberfill and cotton variants continue to cater to price-sensitive consumers, particularly in emerging markets, while hybrid and layered composite toppers (foam + fiber blends) are expanding within mid-to-premium categories as brands focus on multi-layer comfort engineering. Overall, material innovation and wellness-driven consumer preferences remain key demand catalysts.

Thickness Insights

The 2–3 inch thickness segment leads with nearly 38% share in 2025, driven by its balanced value proposition between comfort enhancement and affordability. This thickness provides noticeable support improvement without significantly altering mattress height, making it ideal for residential consumers seeking moderate firmness adjustment. The segment’s growth is primarily fueled by mid-range buyers and online shoppers who prioritize easy installation and compatibility with standard fitted sheets.

Thinner toppers (below 2 inches) are particularly popular in Asia-Pacific markets where compact bedding systems and space optimization are important, especially in urban apartments. Conversely, thicker toppers above 4 inches are witnessing rising demand in luxury hospitality and premium residential segments, where plush comfort and layered cushioning are valued. The hospitality sector’s emphasis on premium sleep experiences acts as a major driver for high-thickness categories.

Distribution Channel Insights

Online channels account for approximately 55% of global revenue, making them the leading distribution segment. The key driver behind this dominance is the rapid expansion of direct-to-consumer (DTC) brands leveraging e-commerce platforms. Digital marketing campaigns, customer reviews, extended trial periods, and competitive pricing models have accelerated consumer migration to online purchasing. Compression roll-pack technology has further reduced logistics costs, enabling cross-border shipments from Asian manufacturing hubs to North America and Europe.

Offline specialty bedding stores remain relevant in the premium segment, particularly for consumers who prefer in-store testing before purchase. Department stores and furniture retailers continue to perform steadily in Europe and Latin America, supported by traditional retail networks and bundled bedding sales. However, digital penetration and omnichannel strategies are expected to further strengthen online leadership over the forecast period.

End-Use Insights

Residential applications dominate with nearly 78% market share in 2025, primarily driven by increasing home comfort upgrades and cost-effective mattress life extension strategies. Rising awareness of sleep quality and ergonomic bedding solutions has led homeowners to adopt mattress toppers as an affordable alternative to mattress replacement. Growing urban housing developments and rising disposable incomes in the Asia-Pacific are further accelerating residential demand.

Commercial applications, including hotels, hospitals, dormitories, and serviced apartments, are expanding at over 7.5% CAGR. The key driver for this segment is hospitality infrastructure growth and rising healthcare investments. Hotels increasingly use premium mattress toppers to enhance guest comfort and brand differentiation, while healthcare facilities adopt pressure-relief toppers to prevent bedsores and improve patient recovery outcomes. Institutional procurement contracts are becoming an important revenue stream for manufacturers targeting bulk supply agreements.

Explore more data points, trends and opportunities Download Free Sample Report

Mattress Topper Market Segmentations

By Material Type

- Memory Foam

- Latex

- Polyurethane Foam

- Feather & Down

- Wool

- Cotton

- Polyester Fiberfill

- Hybrid/Blended

By Thickness

- Below 2 Inches

- 2–3 Inches

- 3–4 Inches

- Above 4 Inches

By Distribution Channel

- Online Retail

- Specialty Bedding Stores

- Furniture & Department Stores

By End-Use

- Residential

- Commercial

Regional Insights

North America

North America leads the global mattress topper market with a 34% share in 2025, with the United States accounting for nearly 80% of regional demand. The primary growth drivers include high disposable income, strong consumer focus on sleep health, and widespread adoption of DTC e-commerce brands. The presence of major bedding manufacturers and aggressive digital marketing strategies further stimulates market penetration. Rising cases of sleep disorders and back pain are increasing demand for orthopedic memory foam toppers. Canada contributes steady growth, driven by residential replacement cycles and rising home improvement spending.

Europe

Europe holds approximately 24% of global demand, led by Germany and the United Kingdom. The key regional growth driver is sustainability-oriented purchasing behavior. European consumers prioritize organic, hypoallergenic, and certified eco-friendly bedding materials, accelerating demand for latex and wool toppers. Stringent product safety regulations and environmental standards also encourage manufacturers to innovate with natural and recyclable materials. Growth is further supported by mature housing markets and renovation-driven bedding upgrades across Western Europe.

Asia-Pacific

Asia-Pacific represents 29% of global revenue and is the fastest-growing region, expanding at close to 8% CAGR. China dominates both manufacturing and domestic consumption, supported by strong export capabilities and rising middle-class purchasing power. India exhibits the highest growth rate in the region due to rapid urbanization, expanding e-commerce penetration, and increasing awareness of sleep health among younger consumers. Japan favors thinner toppers tailored to compact bedding layouts, reflecting urban housing constraints. Regional growth is further driven by rising hospitality investments and increasing adoption of mid-range bedding solutions.

Latin America

Latin America accounts for nearly 6% share, led by Brazil and Mexico. The primary growth drivers include expanding middle-income housing, gradual premiumization of bedding products, and improving retail infrastructure. While price sensitivity remains high, increasing exposure to global bedding brands through online platforms is supporting gradual market expansion. Residential demand remains the primary contributor, with emerging commercial adoption in urban hospitality centers.

Middle East & Africa

The Middle East & Africa region contributes around 7% of global revenue, with growth largely driven by hospitality sector expansion in the United Arab Emirates and Saudi Arabia. Large-scale tourism projects, luxury hotel developments, and government-backed diversification initiatives are stimulating commercial demand for premium mattress toppers. In Africa, South Africa leads regional consumption due to a relatively developed retail sector and rising urban housing projects. Increasing tourism inflows and infrastructure investments remain the key long-term drivers for regional growth.

Key Players in the Mattress Topper Market

- Tempur Sealy International

- Serta Simmons Bedding

- Sleep Number Corporation

- Kingsdown Inc.

- Hilding Anders

- Sheela Foam Ltd.

- Recticel

- Sinomax Group

- MLILY

- Emma Sleep

- Brooklyn Bedding

- ViscoSoft

- Lucid

- Dormeo

- Parachute Home