Maternity Clothing Market Size

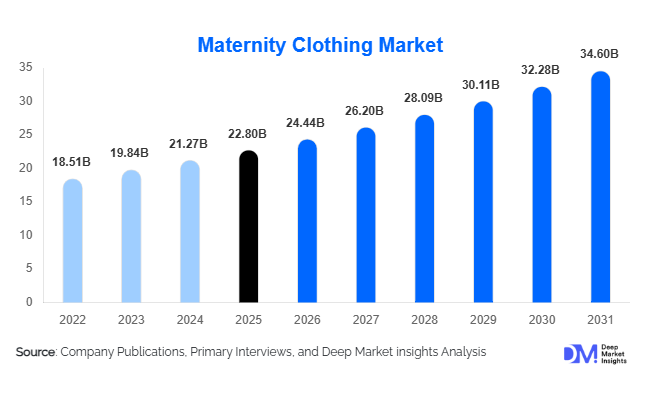

According to Deep Market Insights, the global maternity clothing market size was valued at USD 22.8 billion in 2025 and is projected to grow from USD 24.44 billion in 2026 to reach USD 34.60 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The maternity clothing market growth is primarily driven by rising awareness about maternal health and comfort, increasing participation of women in the workforce, and the growing adoption of e-commerce and sustainable fashion trends tailored to expecting mothers globally.

Key Market Insights

- Dresses dominate product offerings, providing versatility and comfort for casual, formal, and postpartum use, accounting for 28% of the 2025 market share.

- Online distribution channels are rapidly expanding, with 42% of sales in 2025, driven by e-commerce platforms, social media promotion, and direct-to-consumer models.

- Cotton remains the leading fabric type, representing 35% of global consumption, owing to its comfort, breathability, and skin-friendly properties during pregnancy.

- Late-pregnancy wear drives peak demand, accounting for 40% of the market, as clothing needs intensify in the final trimester.

- Asia-Pacific is the fastest-growing region, led by China and India, with urbanization, rising middle-class income, and digital adoption fueling rapid expansion.

- Sustainable and functional textiles, including organic cotton and stretchable fabrics, are reshaping product design and premium segment growth.

What are the latest trends in the maternity clothing market?

Rise of Sustainable and Functional Apparel

Brands are increasingly incorporating sustainable fabrics such as organic cotton, bamboo, and eco-certified materials into maternity collections. Stretchable, breathable, and temperature-regulating textiles are gaining traction to provide comfort and support during pregnancy. Smart textiles with anti-bacterial and moisture-wicking properties are also being introduced, creating a niche for premium maternity wear. Sustainability certifications and ethical manufacturing practices have become key differentiators for global consumers, particularly in Europe and North America.

Digital-First and Direct-to-Consumer Models

The surge in e-commerce and social media marketing has transformed maternity retail. Consumers now prefer brand-owned websites, online marketplaces, and social commerce platforms to access diverse collections and personalized shopping experiences. Brands are leveraging influencer marketing, subscription models, and targeted promotions to capture repeat customers. This digital-first approach is particularly advantageous for new entrants aiming to reach untapped markets in Asia-Pacific, Latin America, and the Middle East.

What are the key drivers in the maternity clothing market?

Increasing Female Workforce Participation

More women continuing professional work during pregnancy are driving demand for stylish, functional maternity workwear. Comfortable yet professional designs are increasingly preferred, particularly in urban centers and developed countries such as the U.S., Germany, and the U.K. Corporate maternity programs and flexible dress codes are further accelerating market demand.

Growing Awareness of Maternal Health & Comfort

Consumers are prioritizing clothing that supports health and comfort during pregnancy. Ergonomic designs, stretchable fabrics, and breathable materials are now considered essential. This trend is supported by healthcare recommendations, social media education, and lifestyle influencers promoting maternal wellness.

Influence of Fashion Trends and Social Media

Expectant mothers increasingly seek trendy, aesthetically appealing maternity clothing. Celebrity endorsements and social media campaigns drive the adoption of premium and designer segments. Fashion-forward maternity collections now cater to both casual and formal occasions, reflecting a shift from purely functional apparel to style-conscious choices.

What are the restraints for the global market?

Limited Usage Period

Maternity clothing has a short lifecycle, typically covering pregnancy and early postpartum stages. This limits consumer willingness to invest in higher-priced or specialty items, particularly in price-sensitive regions.

Price Sensitivity in Emerging Markets

Consumers in developing countries often prefer regular clothing in larger sizes rather than specialized maternity wear, limiting market penetration. This is a key challenge for global brands aiming to expand in price-conscious markets such as India, Nigeria, and Latin America.

What are the key opportunities in the maternity clothing market?

Expansion in Emerging Markets

Countries such as India, Indonesia, Brazil, and Nigeria are witnessing growing awareness about maternal health and rising disposable incomes. Localized product offerings tailored to cultural preferences, coupled with improving retail infrastructure, provide opportunities for brands to capture untapped demand.

Integration of Sustainable & Functional Textiles

There is increasing potential for innovation through eco-friendly fabrics and technologically enhanced textiles. Brands investing in stretchable, breathable, and anti-bacterial materials can differentiate themselves and attract premium consumers. Sustainability certifications and transparent supply chains offer further market advantages.

Growth of Direct-to-Consumer (D2C) and Digital Platforms

Leveraging online platforms allows brands to bypass traditional retail, reduce costs, and build strong consumer relationships. Subscription models, influencer marketing, and personalized recommendations are creating new revenue streams. This model is particularly beneficial for startups and niche brands entering the market globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 22.8 Billion |

| Market Size in 2026 | USD 24.44 Billion |

| Market Size in 2031 | USD 34.60 Billion |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dresses dominate the maternity clothing market, capturing approximately 28% of the global market share in 2025, primarily due to their versatility, comfort, and adaptability across different stages of pregnancy and postpartum use. Unlike other product categories, dresses offer ease of wear, minimal sizing constraints, and flexibility, making them a preferred choice for expecting mothers globally. The segment benefits significantly from the growing trend of multifunctional apparel, where dresses are designed to transition seamlessly from pregnancy to nursing and postpartum phases. Mid-range dresses account for the largest share within this segment, as they strike a balance between affordability and quality, particularly appealing to middle-income consumers. Meanwhile, premium designer maternity dresses are gaining traction in developed markets, driven by fashion-conscious consumers influenced by social media and celebrity culture. The rapid expansion of online retail and social commerce platforms has further amplified demand, enabling brands to offer a wide variety of styles, customization options, and seasonal collections, thereby reinforcing the segment’s leadership position.

Application Insights

Casual maternity wear remains the largest application segment, driven by the everyday clothing needs of pregnant women and the increasing preference for comfortable, breathable, and stylish apparel. This segment accounts for the majority of consumption due to its high frequency of use and broader product availability across price points. However, postpartum and activewear segments are emerging as the fastest-growing categories, supported by rising awareness around maternal recovery, fitness, and overall well-being. The growing popularity of prenatal and postnatal fitness programs has significantly boosted demand for maternity activewear, including stretchable leggings, yoga pants, and athleisure clothing. Additionally, nursing-friendly clothing is gaining widespread acceptance, as breastfeeding-friendly designs become mainstream and are increasingly recommended by healthcare professionals. Export-driven demand plays a critical role in supporting global supply, with manufacturing hubs such as China, India, and Bangladesh accounting for a significant share of exports to North America and Europe, where demand for affordable yet quality maternity apparel continues to rise.

Distribution Channel Insights

Online channels dominate the maternity clothing market, accounting for approximately 42% of total sales in 2025, reflecting the rapid digital transformation of the retail sector. E-commerce platforms, brand-owned websites, and social commerce channels provide consumers with unparalleled convenience, extensive product variety, and competitive pricing. The ability to compare products, access customer reviews, and benefit from promotional offers has significantly increased online adoption, particularly among younger and urban consumers. Additionally, direct-to-consumer (D2C) models are gaining momentum, enabling brands to improve margins and establish stronger customer relationships through personalized experiences. Despite the dominance of online channels, offline retail continues to play a crucial role, especially in premium and high-touch segments where consumers prefer in-store trials and personalized assistance. Specialty maternity stores and department stores remain important in urban and developed regions, offering curated collections and enhancing brand visibility. The integration of omnichannel strategies is further strengthening distribution networks, allowing seamless transitions between online and offline shopping experiences.

End-User Insights

The late-pregnancy segment dominates the maternity clothing market, accounting for approximately 40% of the total market share in 2025, as clothing requirements peak during the third trimester due to significant physical changes. This stage drives the highest demand for specialized apparel with enhanced stretchability, support, and comfort features. Early and mid-pregnancy segments follow, with moderate demand driven by gradual wardrobe transitions. Notably, the postpartum segment is the fastest-growing, expanding at a CAGR of over 8%, fueled by increasing awareness of postnatal recovery needs and the rising adoption of nursing-friendly clothing. Functional features such as adjustable fits, breathable fabrics, and easy-access designs for breastfeeding are key purchase drivers. Urban working women represent the primary consumer base, as they seek stylish, professional, and multifunctional maternity apparel that aligns with modern lifestyle needs. Additionally, increasing dual-income households and delayed pregnancies are further contributing to higher spending on maternity clothing globally.

Explore more data points, trends and opportunities Download Free Sample Report

Maternity Clothing Market Segmentations

By Product Type

- Topwear

- Bottomwear

- Dresses

- Innerwear

- Outerwear

- Activewear & Loungewear

- Specialty Wear

By Application

- Casual Wear

- Workwear/Formal Wear

- Activewear & Fitness

- Postpartum & Nursing Wear

By Distribution Channel

- Online Retail

- Specialty Maternity Stores

- Supermarkets/Hypermarkets

- Department Stores

- Social Commerce Platforms

By End-User Stage

- Early Pregnancy

- Mid Pregnancy

- Late Pregnancy

- Postpartum Stage

Regional Insights

North America

North America holds approximately 30% of the global maternity clothing market, with the United States accounting for the largest share, followed by Canada. The region’s dominance is driven by high disposable income, strong consumer awareness regarding maternal health, and a well-established retail infrastructure. The widespread adoption of e-commerce and direct-to-consumer brands has significantly boosted accessibility and product variety. Additionally, the high participation of women in the workforce has increased demand for professional and stylish maternity wear. Premiumization trends, coupled with the growing influence of social media and celebrity endorsements, are further driving demand for high-quality and designer maternity clothing. The presence of leading global brands and continuous product innovation also contributes to sustained market growth in the region.

Europe

Europe accounts for around 25% of the global market, led by key countries such as Germany, the United Kingdom, and France. The region is characterized by strong demand for sustainable and ethically produced maternity clothing, driven by stringent environmental regulations and high consumer awareness. The growing preference for organic fabrics and eco-friendly manufacturing processes is shaping product development strategies. Additionally, premiumization trends are prominent, with consumers willing to pay higher prices for quality and sustainable products. The increasing adoption of online retail channels, particularly among younger demographics, is further supporting market expansion. Government policies supporting maternal health and work-life balance also indirectly contribute to sustained demand for maternity apparel.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR of approximately 8.5%, and accounts for nearly 28% of the global market. China and India are the primary growth engines, driven by large population bases, rising birth rates in certain regions, and increasing disposable income among the middle class. Rapid urbanization and changing lifestyle patterns are encouraging the adoption of specialized maternity clothing over traditional alternatives. The region also benefits from strong manufacturing capabilities and export-oriented textile industries, particularly in China, India, and Bangladesh. The rapid expansion of e-commerce platforms and the growing influence of social media are further accelerating demand, especially among younger consumers seeking fashionable and affordable maternity wear.

Middle East & Africa

The Middle East & Africa region represents approximately 9% of the global market, with key demand centers in Saudi Arabia, the UAE, and Nigeria. High birth rates and a growing focus on maternal health and wellness are primary drivers of market growth. Increasing urbanization and rising disposable income, particularly in Gulf Cooperation Council (GCC) countries, are supporting demand for premium and mid-range maternity clothing. Additionally, the expansion of modern retail infrastructure and e-commerce platforms is improving product accessibility. Cultural preferences for modest fashion are also influencing product design, creating opportunities for region-specific maternity apparel collections.

Latin America

Latin America accounts for approximately 8% of the global market, with Brazil and Mexico being the leading contributors. Market growth is driven by increasing urbanization, improving retail infrastructure, and rising awareness of maternal health. The expansion of international and regional brands into these markets is enhancing product availability and variety. However, price sensitivity remains a key challenge, limiting widespread adoption of premium maternity clothing. Despite this, the growing middle-class population and increasing penetration of e-commerce platforms are expected to drive steady market growth. Additionally, the influence of Western fashion trends and social media is gradually reshaping consumer preferences toward more specialized maternity apparel.