Mahogany Market Size

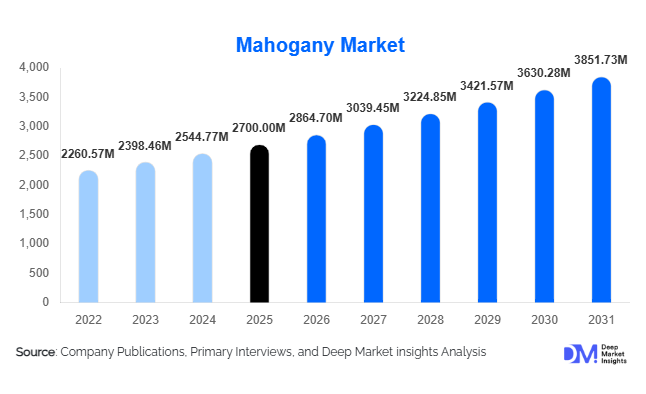

According to Deep Market Insights, the global mahogany market size was valued at USD 2,700 million in 2025 and is projected to grow from USD 2,864.70 million in 2026 to reach USD 3,851.73 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The mahogany market growth is primarily driven by increasing demand for premium hardwood in furniture manufacturing, rising investments in luxury housing and interior décor, and the global shift toward sustainable and certified wood sourcing practices.

Key Market Insights

- Plantation-grown mahogany is gaining dominance, supported by sustainability regulations and declining reliance on natural forests.

- Furniture manufacturing remains the largest application, accounting for over 40% of total demand due to premiumization trends.

- Asia-Pacific dominates the global market, driven by strong manufacturing bases and export-oriented production.

- Residential construction is the largest end-use segment, fueled by urbanization and rising disposable incomes.

- Direct B2B sales channels lead distribution, ensuring cost efficiency and consistent quality for large-scale buyers.

- Technological advancements in engineered wood products are expanding accessibility and optimizing raw material utilization.

What are the latest trends in the mahogany market?

Shift Toward Sustainable and Certified Wood

The mahogany market is increasingly shaped by sustainability concerns, with a strong shift toward certified wood sourced from managed plantations. Regulatory frameworks and environmental awareness are pushing manufacturers and consumers to prioritize legally sourced and eco-certified mahogany. Certifications such as FSC are becoming essential for global trade, especially in Europe and North America. This trend is encouraging investments in plantation forestry, ensuring long-term supply stability while reducing environmental impact. Companies are also integrating traceability systems into supply chains, enhancing transparency and compliance with international regulations.

Rise of Engineered Mahogany Products

Technological advancements are driving the adoption of engineered mahogany products such as veneers, plywood, and laminated boards. These products offer cost efficiency, improved material utilization, and consistent quality, making them suitable for mid-range applications. Engineered solutions are particularly gaining traction in urban housing and commercial interiors where cost optimization is critical. Additionally, innovations in finishing technologies are enabling manufacturers to replicate the aesthetics of solid mahogany, expanding the market to a broader consumer base while maintaining premium appeal.

What are the key drivers in the mahogany market?

Growing Demand for Premium Furniture

The global furniture industry continues to expand, with increasing consumer preference for high-quality, durable, and aesthetically appealing products. Mahogany’s superior grain, durability, and workability make it a preferred material for premium furniture manufacturing. Export-driven furniture production in Asia-Pacific countries is further boosting demand, as international markets increasingly favor high-end wooden products.

Expansion of the Construction and Interior Design Sector

Rapid urbanization and rising real estate investments are driving demand for luxury construction materials. Mahogany is widely used in flooring, paneling, doors, and decorative elements due to its resistance to decay and elegant appearance. The growth of luxury housing projects in emerging economies is significantly contributing to market expansion, as developers prioritize premium materials for differentiation.

What are the restraints for the global market?

Stringent Environmental Regulations

Strict regulations governing logging and the trade of hardwood species pose significant challenges to the mahogany market. International agreements aimed at preventing deforestation limit the availability of natural forest mahogany, increasing compliance costs and supply constraints. Companies must invest in certification and sustainable sourcing practices to remain competitive in global markets.

High Raw Material Costs and Price Volatility

Mahogany is a premium hardwood with a relatively limited supply, leading to high costs and price fluctuations. Variability in supply from natural forests and plantations impacts pricing, making it less accessible for cost-sensitive applications. This has encouraged the use of alternative materials and engineered wood products, posing a challenge to traditional mahogany demand.

What are the key opportunities in the mahogany industry?

Expansion of Plantation Forestry

Investments in plantation-grown mahogany present a major opportunity for ensuring a sustainable supply and reducing dependence on natural forests. Regions such as Southeast Asia, Latin America, and Africa are witnessing increased plantation development supported by government initiatives and private investments. Companies integrating plantation ownership into their value chain can achieve cost advantages and long-term supply security.

Growth in Luxury Housing and Interior Markets

Rising disposable incomes and changing consumer preferences are driving demand for premium interior materials. Mahogany’s association with luxury and durability makes it highly attractive for high-end residential and commercial projects. Emerging markets such as India, China, and the Middle East are creating new growth avenues for manufacturers offering customized and high-value products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2700 Million |

| Market Size in 2026 | USD 2864.70 Million |

| Market Size in 2031 | USD 3851.73 Million |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Solid mahogany wood continues to dominate the global market, accounting for approximately 46% of the total market share in 2025. This leadership position is primarily driven by its superior durability, rich grain aesthetics, and high structural integrity, making it the preferred choice for premium furniture, luxury interiors, and architectural applications. The segment’s growth is further supported by increasing consumer preference for authentic, high-value hardwood products, particularly in developed markets such as North America and Europe. Additionally, export-oriented furniture manufacturers in the Asia-Pacific region rely heavily on solid mahogany to meet international quality standards, reinforcing its global demand.

Mahogany veneers and plywood are gaining significant traction, particularly in cost-sensitive markets, due to their ability to deliver the visual appeal of mahogany at a lower price point. This segment is expanding rapidly in commercial construction and modular furniture applications where affordability and scalability are critical. Meanwhile, engineered mahogany products, including laminated boards and MDF with mahogany finishes, are emerging as the fastest-growing category. Their growth is driven by advancements in manufacturing technologies, improved material efficiency, and increasing adoption in mid-range residential and commercial projects, enabling broader market penetration beyond traditional luxury segments.

Application Insights

Furniture manufacturing remains the largest application segment, contributing approximately 44% of total global demand. The segment’s dominance is underpinned by the rising global appetite for premium and export-quality furniture, particularly from markets in North America and Europe. Mahogany’s workability, resistance to warping, and aesthetic appeal make it highly suitable for crafting high-end furniture pieces, including cabinets, tables, and decorative items. The continued expansion of export-driven furniture industries in countries such as Vietnam, China, and Indonesia further strengthens this segment’s leading position.

Interior décor applications, including flooring, wall paneling, and cabinetry, are witnessing steady growth due to increasing investments in residential and commercial construction. The shift toward luxury interior design, especially in urban housing and hospitality sectors, is driving demand for visually appealing and durable materials like mahogany. Additionally, niche applications such as musical instruments and marine construction continue to provide specialized growth opportunities, supported by mahogany’s acoustic properties and moisture resistance.

Distribution Channel Insights

Direct B2B sales dominate the mahogany market, accounting for nearly 70% of the total market share. This dominance is driven by large-scale furniture manufacturers, construction companies, and OEMs that prefer direct procurement from suppliers to ensure consistent quality, bulk pricing advantages, and reliable supply chains. Long-term contracts and strategic sourcing partnerships further strengthen this channel, particularly in export-oriented industries.

Distributors and timber merchants continue to play a crucial role in regional markets, especially in fragmented and developing economies where smaller manufacturers rely on intermediaries for supply. These channels provide flexibility in procurement and access to diverse product ranges. Meanwhile, online platforms and digital marketplaces are gradually gaining traction, driven by increasing demand for customization and direct customer engagement. The adoption of e-commerce in the wood industry is enabling manufacturers to reach a broader customer base, particularly in the small-scale and bespoke furniture segments.

End-Use Industry Insights

The residential sector leads the mahogany market, accounting for approximately 48% of total demand in 2025. This dominance is driven by increasing housing construction, renovation activities, and growing consumer preference for premium interior materials. Rising disposable incomes and urbanization in emerging economies are further accelerating demand for mahogany-based furniture and décor products in residential applications.

The commercial sector, particularly hospitality, retail, and office spaces, is the fastest-growing segment, supported by rising investments in luxury infrastructure and premium interior design. Hotels, resorts, and high-end retail outlets are increasingly adopting mahogany for its aesthetic appeal and durability, enhancing customer experience and brand value. Industrial and specialized applications, including marine construction and musical instruments, represent a smaller but steadily growing segment. These niche applications benefit from mahogany’s unique properties, such as moisture resistance and acoustic performance, ensuring consistent demand despite their limited market share.

Explore more data points, trends and opportunities Download Free Sample Report

Mahogany Market Segmentations

By Product Type

- Solid Mahogany Wood

- Mahogany Veneers & Plywood

- Engineered Mahogany Products

- Finished Mahogany Components

By Application

- Furniture Manufacturing

- Interior Décor

- Musical Instruments

- Marine Applications

- Luxury Construction

By Distribution Channel

- Direct B2B Sales

- Distributors & Timber Merchants

- Online Platforms

By End-Use Industry

- Residential Sector

- Commercial Sector

- Industrial & Specialized Applications

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global mahogany market with approximately 38% share in 2025, driven by its strong manufacturing base and export-oriented industries. Countries such as China, India, Vietnam, and Indonesia are key contributors. China leads global furniture production, supported by large-scale manufacturing infrastructure and strong export demand. India’s rapidly expanding housing sector and increasing middle-class income levels are boosting domestic consumption of mahogany products. Vietnam has emerged as a major exporter of mahogany-based furniture, benefiting from favorable trade agreements and competitive labor costs.

The region’s growth is primarily driven by low-cost manufacturing, expanding export markets, government support for wood processing industries, and increasing urbanization. Additionally, the availability of plantation-grown mahogany in Southeast Asia ensures a stable supply chain, further strengthening the region’s dominance. Asia-Pacific is also the fastest-growing region, with a CAGR exceeding 7%, supported by rising domestic consumption and global trade integration.

North America

North America accounts for approximately 26% of the global market, with the United States being the largest consumer. The region’s demand is driven by high spending on home renovation, premium furniture, and luxury interior design. The U.S. housing market, particularly the remodeling segment, plays a critical role in sustaining mahogany demand.

Growth in this region is supported by strong consumer purchasing power, preference for high-quality hardwood products, and increasing demand for sustainable and certified wood. North America relies heavily on imports from Asia and Latin America, making it a key destination for global exporters. Additionally, the growing trend toward eco-friendly construction materials is encouraging the adoption of certified plantation-grown mahogany.

Europe

Europe holds around 22% market share, led by Germany, Italy, and the United Kingdom. The region is characterized by stringent environmental regulations and a strong emphasis on sustainable sourcing. Demand for mahogany is driven by high standards for quality, craftsmanship, and environmental compliance, particularly in furniture manufacturing and interior design.

The region’s growth is driven by strict regulatory frameworks, high demand for certified wood products, and strong design-oriented furniture industries. European consumers show a strong preference for eco-friendly and ethically sourced materials, which is encouraging the adoption of plantation-grown mahogany. Additionally, the presence of established luxury furniture manufacturers supports consistent demand.

Latin America

Latin America contributes approximately 8% to the global market, with Brazil and Peru playing significant roles as both producers and consumers. The region benefits from abundant natural forest resources and favorable climatic conditions for plantation forestry.

Growth in Latin America is driven by increasing investments in plantation development, export opportunities, and government initiatives supporting sustainable forestry. The region serves as a critical supplier of raw mahogany to global markets, particularly North America and Europe. Additionally, improving processing capabilities and infrastructure is enhancing the region’s competitiveness in value-added products.

Middle East & Africa

The Middle East and Africa account for approximately 6% of the global market. Demand in the Middle East is primarily driven by luxury construction projects in countries such as the UAE and Saudi Arabia, where mahogany is widely used in high-end interiors and architectural applications. Africa, on the other hand, plays a key role as a source of raw mahogany.

The region’s growth is supported by increasing luxury real estate development, rising tourism infrastructure investments, and expanding plantation forestry initiatives in Africa. Additionally, government efforts to promote sustainable logging practices and attract foreign investments in forestry are contributing to market expansion. While the market size remains relatively smaller, the region presents strong long-term growth potential due to its resource base and infrastructure development.

Key Players in the Mahogany Market

- Weyerhaeuser Company

- West Fraser Timber Co.

- Stora Enso

- UFP Industries

- Canfor Corporation

- Interfor Corporation

- Georgia-Pacific LLC

- Boise Cascade Company

- Samling Group

- Danzer Group

- Precious Woods Holding

- Aljoma Lumber

- Boral Timber

- Vicwood Industry Co.

- Swedwood Group