Luxury Luggage Market Size

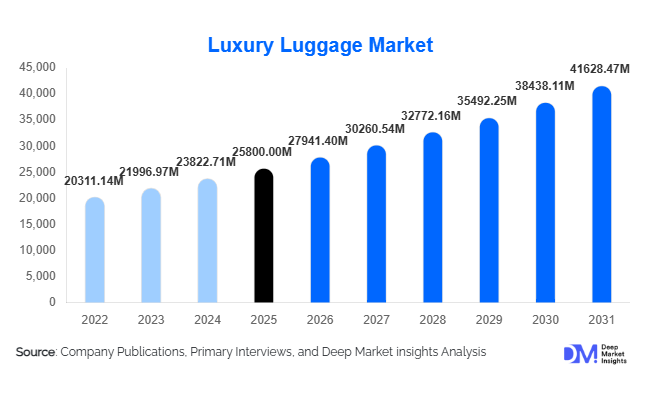

According to Deep Market Insights, the global luxury luggage market size was valued at USD 25,800 million in 2025 and is projected to grow from USD 27,941.40 million in 2026 to reach USD 41,628.47 million by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The luxury luggage market growth is primarily driven by the resurgence of global travel, increasing disposable income among affluent consumers, and the rising demand for premium lifestyle accessories that combine functionality with status appeal. The market is also benefiting from innovations in materials such as lightweight polycarbonate and aluminum alloys, along with the integration of smart technologies, including GPS tracking and biometric locks.

Key Market Insights

- Luxury luggage demand is increasingly driven by experiential travel trends, with consumers prioritizing premium travel accessories as part of lifestyle branding.

- Direct-to-consumer channels are gaining prominence, enabling brands to offer personalized experiences and maintain pricing control.

- Europe dominates the global market, supported by heritage luxury brands and strong tourism inflows.

- Asia-Pacific is the fastest-growing region, driven by rising affluence and outbound travel from China and India.

- Technological integration, including smart locks and tracking systems, is reshaping product innovation.

- Sustainability is emerging as a key differentiator, with brands adopting eco-friendly materials and ethical production practices.

What are the latest trends in the luxury luggage market?

Smart and Connected Luggage Solutions

Luxury luggage brands are increasingly integrating smart technologies into their products to enhance convenience and security. Features such as GPS tracking, biometric locks, USB charging ports, and app-based controls are becoming standard in premium offerings. These innovations cater to tech-savvy travelers who value both functionality and exclusivity. Smart luggage also enables real-time tracking and remote locking, reducing the risk of loss or theft during transit. As digital ecosystems expand, brands are focusing on seamless integration with smartphones and travel apps, enhancing the overall travel experience while maintaining luxury aesthetics.

Sustainable and Ethical Luxury Manufacturing

Sustainability is becoming a central theme in the luxury luggage market. Consumers are increasingly demanding environmentally responsible products, prompting manufacturers to adopt recycled materials, vegan leather alternatives, and carbon-neutral production processes. Brands are also emphasizing transparency in sourcing and manufacturing, aligning with global ESG standards. Limited-edition collections made from sustainable materials are gaining popularity, particularly among younger consumers. This shift toward eco-conscious luxury is not only improving brand perception but also creating new opportunities for innovation in material science and product design.

What are the key drivers in the luxury luggage market?

Growth in Global Travel and Tourism

The recovery and expansion of global travel have significantly boosted demand for luxury luggage. Increasing international tourist arrivals and the rise of experiential travel are driving consumers to invest in high-quality travel accessories. Frequent travelers, especially business and leisure segments, are prioritizing durable and premium luggage solutions that enhance convenience and reflect their lifestyle.

Rising Affluent Consumer Base

The growing population of high-net-worth individuals and aspirational middle-class consumers is a major driver of market growth. Emerging economies, particularly in the Asia-Pacific and the Middle East, are witnessing rapid wealth accumulation, leading to increased spending on luxury goods. Consumers are increasingly viewing luxury luggage as a status symbol, contributing to strong demand across core and ultra-luxury segments.

What are the restraints for the global market?

High Product Pricing

Luxury luggage products are priced significantly higher than mass-market alternatives, limiting their accessibility to a broader consumer base. This price sensitivity is particularly evident in emerging markets, where affordability remains a key constraint despite rising incomes.

Counterfeit Products and Grey Markets

The proliferation of counterfeit luxury luggage products poses a significant challenge to authentic brands. Fake products not only impact revenues but also dilute brand value and consumer trust. The expansion of online marketplaces has further amplified this issue, making it difficult for brands to control distribution and maintain exclusivity.

What are the key opportunities in the luxury luggage industry?

Expansion in Emerging Markets

Emerging economies such as China, India, and the UAE present significant growth opportunities due to rising disposable incomes and increasing outbound travel. These markets are still underpenetrated, allowing brands to expand their presence through localized strategies and premium retail experiences.

Technology Integration and Product Innovation

The integration of advanced technologies into luggage design offers substantial opportunities for differentiation. Smart luggage solutions that enhance convenience, security, and connectivity are expected to attract high-value customers and drive premium pricing strategies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 25800 Million |

| Market Size in 2026 | USD 27941.40 Million |

| Market Size in 2031 | USD 41628.47 Million |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Suitcases dominate the luxury luggage market, accounting for nearly 48% of the total market share in 2025. This leadership position is primarily driven by their indispensable role in both short-haul and long-haul travel, making them the most frequently purchased luxury luggage category. Continuous innovation in lightweight construction, impact-resistant shells, and modular storage systems has further strengthened their adoption. Premium brands are also introducing smart suitcases with integrated tracking and charging capabilities, enhancing their value proposition. Additionally, increasing international travel frequency and airline baggage standardization have reinforced the preference for structured suitcase formats.

Travel bags, including duffels and garment bags, serve niche but growing segments, particularly among luxury leisure travelers and fashion-conscious consumers seeking flexibility and style. Business and executive bags maintain steady demand due to rising corporate travel and the need for professional aesthetics. Meanwhile, specialty luxury travel goods such as cosmetic cases and jewelry organizers represent a smaller yet high-margin segment, driven by personalization trends, gifting demand, and the expansion of luxury lifestyle ecosystems.

Material Type Insights

Polycarbonate-based luggage leads the market with approximately 34% share, driven by its superior balance of lightweight properties, durability, and modern design appeal. The material’s resistance to impact and scratches makes it highly suitable for frequent travelers, while its flexibility allows for innovative shapes and finishes. The growing demand for lightweight travel solutions, particularly among international travelers facing strict baggage weight limits, has significantly contributed to this segment’s dominance.

Leather luggage continues to command strong demand in the ultra-luxury segment, where craftsmanship, heritage, and exclusivity are key purchasing factors. High-end consumers often prefer leather for its timeless appeal and premium feel. Hybrid materials combining aluminum, leather, and advanced synthetics are gaining traction as brands aim to differentiate through design innovation and enhanced durability. Additionally, the emergence of sustainable materials, including recycled polycarbonate and vegan leather alternatives, is reshaping material preferences, especially among environmentally conscious consumers.

Price Tier Insights

The core luxury segment (USD 800–2,000) holds the largest share at around 46%, as it effectively balances aspirational affordability with premium brand value. This segment is driven by affluent middle-class consumers and frequent travelers who seek high-quality products without entering ultra-luxury price points. Strong brand positioning, seasonal collections, and product innovations continue to support growth in this category.

Accessible luxury products are expanding rapidly, fueled by younger consumers and first-time luxury buyers who are increasingly influenced by digital marketing and social media. This segment acts as an entry point into luxury brands. On the other hand, ultra-luxury luggage caters to high-net-worth individuals, offering bespoke designs, rare materials, and limited-edition collections. Growth in this segment is supported by rising global wealth concentration and increasing demand for exclusivity and personalization.

Distribution Channel Insights

Direct retail channels account for approximately 38% of total sales, driven by consumer preference for immersive brand experiences, authenticity assurance, and personalized services. Flagship stores and boutique outlets allow brands to showcase their heritage, craftsmanship, and premium positioning, which is critical in the luxury segment. In-store experiences, including customization services and exclusive product launches, further enhance customer engagement.

Online channels are witnessing the fastest growth, supported by the digital transformation of luxury retail and increasing consumer confidence in e-commerce platforms. Brands are investing heavily in direct-to-consumer (D2C) strategies, offering seamless digital experiences, virtual consultations, and omnichannel integration. Duty-free and travel retail channels are also rebounding strongly with the recovery of global air travel, benefiting from impulse purchases and high spending by international travelers, particularly in major airport hubs.

End-Use Insights

Individual consumers dominate the market with nearly 72% share, driven by the combined demand from leisure and business travel segments. The rapid recovery of tourism and the growing popularity of experiential travel are significantly boosting purchases in this category. Consumers increasingly view luxury luggage as both a functional necessity and a status symbol, reinforcing demand across multiple travel occasions.

Corporate buyers contribute steadily through executive gifting programs and employee travel needs, particularly in multinational organizations. Institutional buyers, including luxury hotels and airlines, represent a niche but high-value segment, often requiring customized luggage solutions for premium services such as first-class travel kits and concierge offerings. The expansion of luxury hospitality and premium aviation services is expected to further support this segment’s growth.

Explore more data points, trends and opportunities Download Free Sample Report

Luxury Luggage Market Segmentations

By Product Type

- Suitcases

- Travel Bags

- Business & Executive Bags

- Specialty Luxury Travel Goods

By Material Type

- Leather-Based Luggage

- Premium Synthetic Materials

- Hybrid Materials

- Metal-Based Luggage

By Distribution Channel

- Direct Retail

- Online Channels

- Department & Specialty Stores

- Duty-Free & Travel Retail

By End-User

- Individual Consumers

- Corporate Buyers

- Institutional Buyers

Regional Insights

North America

North America holds approximately 28% of the global market share, with the United States accounting for the majority of regional demand. Growth in this region is driven by high disposable incomes, a well-established culture of frequent travel, and strong consumer affinity for premium and branded products. The presence of a large base of business travelers and the rapid adoption of smart luggage solutions further support market expansion. Additionally, the region benefits from advanced retail infrastructure and strong e-commerce penetration, enabling seamless access to luxury products. Increasing demand for sustainable and technologically advanced luggage is also shaping purchasing decisions among North American consumers.

Europe

Europe dominates the global market with around 32% share, supported by countries such as France, Italy, Germany, and the United Kingdom. The region’s leadership is primarily driven by its strong heritage in luxury craftsmanship and the presence of globally renowned luxury brands. High inbound tourism, particularly in key destinations such as Paris and Milan, significantly boosts retail sales of luxury luggage. European consumers exhibit a strong preference for quality, design, and sustainability, encouraging brands to innovate in eco-friendly materials and production processes. Additionally, the region’s well-developed duty-free and travel retail network contributes to consistent demand growth.

Asia-Pacific

Asia-Pacific accounts for approximately 26% of the market share and is the fastest-growing region, with a projected double-digit growth rate in key countries. China leads regional demand, contributing over 40% of APAC sales, followed by Japan, South Korea, and India. Growth in this region is driven by rapid urbanization, rising disposable incomes, and a surge in outbound tourism. The increasing number of high-net-worth individuals and aspirational consumers is significantly boosting demand for luxury goods. Additionally, strong digital adoption and the influence of social media are accelerating brand awareness and online sales. Government initiatives promoting tourism and improved air connectivity are further supporting regional growth.

Latin America

Latin America is an emerging market, with Brazil and Mexico leading demand. Growth in this region is primarily driven by expanding middle-class populations, increasing exposure to global luxury brands, and rising international travel. While economic volatility remains a challenge, urban consumers are increasingly adopting premium lifestyle products. The growth of shopping malls, duty-free retail, and online platforms is improving accessibility to luxury luggage. Additionally, demand is being supported by younger consumers who are influenced by global fashion trends and digital media.

Middle East & Africa

The Middle East & Africa region is experiencing robust growth, particularly in the UAE and Saudi Arabia, which serve as major luxury retail hubs. The region’s growth is driven by high-income populations, strong preference for luxury goods, and significant investments in tourism infrastructure. Mega projects, including luxury resorts and international airports, are enhancing the region’s appeal as a global travel destination. The presence of major duty-free shopping hubs, such as Dubai, further boosts luxury luggage sales. In Africa, growth is supported by increasing tourism and the gradual expansion of luxury retail networks, although the market remains relatively nascent compared to other regions.

Key Players in the Luxury Luggage Market

- Samsonite International

- Tumi Holdings

- Rimowa

- Louis Vuitton

- Gucci

- Prada

- Briggs & Riley

- Travelpro

- Victorinox

- Montblanc

- Delsey

- Porsche Design

- Globe-Trotter

- Bric’s

- Antler