Luxury Hotels Market Size

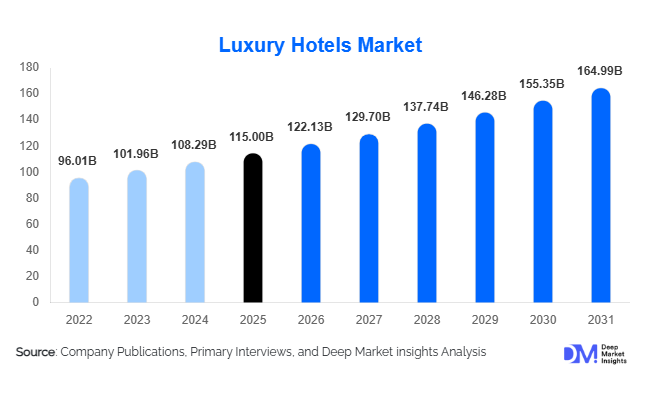

According to Deep Market Insights, the global luxury hotels market size was valued at USD 115.0 billion in 2025 and is projected to grow from USD 122.13 billion in 2025 to reach USD 164.99 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The luxury hotels market growth is primarily driven by rising global affluence, increasing demand for experiential and wellness-focused travel, expansion of international tourism infrastructure, and rapid adoption of digital hospitality technologies across premium hotel chains worldwide.

Key Market Insights

- Luxury hospitality is shifting toward experience-led offerings, including wellness retreats, cultural immersion, and personalized services.

- Resort luxury hotels dominate global demand, driven by leisure tourism and destination-based travel experiences.

- Asia-Pacific is the fastest-growing region, supported by rising middle-class income and outbound tourism expansion.

- Chain-affiliated luxury hotels lead the market, benefiting from global brand recognition and loyalty ecosystems.

- Direct booking channels are increasing in share, reducing dependency on OTAs, and improving profit margins.

- Sustainability and eco-luxury concepts are becoming mainstream, influencing both investment and consumer preferences.

What are the latest trends in the luxury hotels market?

Rise of Wellness and Experiential Luxury Hospitality

Luxury hotels are increasingly integrating wellness, mindfulness, and experiential tourism into core offerings. Spa retreats, yoga programs, organic dining, and holistic healing experiences are becoming standard across premium resorts. Travelers now prioritize emotional well-being, cultural immersion, and nature-based experiences over traditional accommodation-only stays. This shift is particularly strong in resort destinations and eco-luxury properties, where hotels are redesigning infrastructure around sustainability and lifestyle enhancement. The trend is also driving higher average daily rates (ADR) and longer guest stays.

Technology-Driven Personalization and Smart Hotels

The adoption of advanced technologies is transforming luxury hospitality. AI-powered concierge systems, IoT-enabled smart rooms, facial recognition check-ins, and predictive analytics are enhancing guest experience and operational efficiency. Hotels are leveraging big data to deliver hyper-personalized services, improving customer loyalty and revenue per guest. Digital ecosystems, mobile-first booking platforms, and blockchain-based loyalty programs are further strengthening brand competitiveness in the luxury segment.

What are the key drivers in the luxury hotels market?

Expanding High-Net-Worth Population

The increasing number of high-net-worth individuals (HNWIs) globally is a major demand driver. This segment contributes significantly to premium and ultra-luxury hotel bookings, favoring exclusive stays, personalized services, and high-end experiential travel. Growth in wealth concentration across Asia-Pacific and the Middle East is accelerating demand for luxury hospitality services.

Growth in Global Tourism Infrastructure

Improved air connectivity, tourism-friendly visa policies, and large-scale infrastructure development projects are expanding international travel accessibility. Governments across emerging economies are investing heavily in tourism corridors, airport expansion, and hospitality zones, directly supporting luxury hotel development and occupancy growth.

Shift Toward Experiential Travel

Modern travelers are increasingly prioritizing experiences over material goods. Luxury hotels are responding with curated cultural programs, culinary tourism, adventure-based stays, and wellness-centric packages. This evolution is significantly increasing customer engagement and supporting premium pricing models across global hotel chains.

What are the restraints for the global market?

High Capital and Operational Costs

Luxury hotels require substantial investment in premium real estate, high-end amenities, and skilled workforce management. Operational expenses, including maintenance of luxury standards, significantly impact profitability and limit new market entry.

Economic Volatility and Geopolitical Risks

Luxury travel is highly sensitive to global economic fluctuations, inflation, and geopolitical instability. Currency volatility and reduced discretionary spending during downturns can negatively affect international travel demand and occupancy rates.

What are the key opportunities in the luxury hotels industry?

Expansion in Emerging Luxury Tourism Markets

Emerging economies such as India, China, the UAE, and Saudi Arabia present strong growth opportunities due to rising affluence and government-backed tourism initiatives. Large-scale projects such as smart cities and tourism mega-developments are creating high-demand luxury hospitality hubs.

Integration of Advanced Digital Technologies

Hotels investing in AI, IoT, and data-driven personalization are gaining a competitive advantage. These technologies enhance customer experience, optimize pricing strategies, and improve operational efficiency, enabling higher margins and repeat bookings.

Growth of Eco-Luxury and Wellness Segments

The increasing demand for sustainable and wellness-focused travel is creating new revenue streams. Eco-certified resorts, carbon-neutral operations, and wellness retreats are attracting high-spending travelers seeking responsible luxury experiences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 115.0 Billion |

| Market Size in 2026 | USD 122.13 Billion |

| Market Size in 2031 | USD 164.99 Billion |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bottled water continues to dominate the global hydration products market, accounting for approximately 42% of total market share in 2024. Its leadership is primarily driven by its essential nature, universal accessibility, and strong consumer perception as a safe and reliable hydration source. Rapid urbanization and concerns over drinking water quality in emerging economies further reinforce its dominance. However, the segment is gradually evolving with the rise of functional bottled water, enriched with electrolytes, vitamins, and minerals, catering to health-conscious consumers seeking added wellness benefits.

Sports drinks and electrolyte-based hydration products represent the fastest-growing segment, driven by increasing participation in fitness activities, gym culture, and endurance sports. The growing emphasis on performance hydration, recovery, and energy replenishment has significantly expanded demand. Additionally, product innovation in low-sugar and natural formulations is accelerating adoption across younger demographics. Plant-based hydration beverages such as coconut water and aloe vera drinks are also witnessing strong growth due to their natural positioning, clean-label appeal, and perceived health benefits, particularly in North America and Europe. The global shift toward preventive healthcare, fitness-led lifestyles, and functional nutrition is the primary driver accelerating demand across sports drinks and functional hydration categories.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape with approximately 38% market share, owing to their extensive product assortment, strong retail penetration, and consumer preference for physical product comparison before purchase. These channels remain particularly strong in both developed and emerging markets due to their accessibility and promotional pricing strategies.

However, online retail is the fastest-growing distribution channel, driven by digital transformation, increasing smartphone penetration, and rising preference for convenience-based shopping. Subscription-based hydration delivery services and direct-to-consumer (D2C) brand strategies are further reshaping purchasing behavior. Pharmacies and specialty stores also play a critical role in distributing medical-grade hydration products, electrolyte solutions, and premium wellness beverages, especially in urban markets. The expansion of e-commerce ecosystems, coupled with personalized subscription models and digital health awareness, is significantly accelerating online hydration product sales globally.

End-Use Insights

General consumers represent the largest end-use segment, contributing nearly 60% of total market demand in 2024. This dominance is attributed to the widespread daily consumption of bottled water and packaged hydration products across households, workplaces, and urban populations. Rising awareness of hydration’s role in overall health has further strengthened this segment’s growth.

The sports and fitness segment is the fastest-growing end-use category, expanding at over 8% annually. Growth is fueled by increasing gym memberships, rising participation in endurance sports, and the global fitness movement. Healthcare applications, particularly oral rehydration solutions (ORS), are also contributing significantly due to rising incidences of dehydration-related conditions and increasing focus on preventive healthcare systems. The global expansion of fitness culture and preventive healthcare awareness is the primary factor driving strong demand for functional hydration products across sports and medical applications.

Explore more data points, trends and opportunities Download Free Sample Report

Luxury Hotels Market Segmentations

By Property Type

- Business Luxury Hotels

- Resort Luxury Hotels

- Boutique Luxury Hotels

- Heritage & Palace Hotels

- Wellness & Spa Retreats

- Eco-Luxury Hotels

By Customer Type

- Corporate Travelers

- Leisure Travelers

- High-Net-Worth Individuals (HNWIs)

- Ultra-High-Net-Worth Individuals (UHNWIs)

- Group & Event Travelers (MICE)

By Booking Channel

- Direct Booking (Hotel Websites & Apps)

- Online Travel Agencies (OTAs)

- Travel Management Companies (TMCs)

- Offline Travel Agents

By Ownership & Management Model

- Chain-affiliated Luxury Hotels

- Independent Luxury Hotels

- Franchise-based Luxury Hotels

- Management Contract-based Hotels

Regional Insights

Asia-Pacific

Asia-Pacific leads the global hydration products market with approximately 35% share in 2024, making it the largest regional contributor. China and India are the primary growth engines, supported by large population bases, rapid urbanization, and rising disposable incomes. India is among the fastest-growing country markets due to increasing bottled water consumption, expanding retail infrastructure, and growing health consciousness among urban consumers. Rapid urban population growth, increasing heat stress conditions, expanding middle-class income levels, and strong demand for affordable packaged hydration solutions are driving regional expansion.

North America

North America accounts for approximately 28% of the global market share, led by the United States. The region is characterized by high consumption of sports drinks, premium hydration products, and functional beverages. Strong fitness culture, advanced retail penetration, and continuous product innovation are key growth contributors. Rising health consciousness, strong gym and fitness culture, high adoption of functional beverages, and demand for low-sugar premium hydration products are driving sustained growth in the region.

Europe

Europe represents around 22% of the global market, with Germany, the United Kingdom, and France being major demand centers. The region shows a strong preference for sustainable, organic, and clean-label hydration products. Strict environmental regulations and consumer awareness regarding packaging waste are shaping product innovation. Strong sustainability regulations, high demand for eco-friendly packaging, and increasing preference for natural and organic beverages are driving market expansion in Europe.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth due to extreme climatic conditions, high temperatures, and water scarcity challenges. Countries such as the UAE and Saudi Arabia are major consumers of bottled water and electrolyte-based hydration solutions, supported by strong tourism and expatriate populations. Water scarcity, extreme climatic conditions, rising tourism inflow, and increasing dependency on packaged hydration solutions are key factors driving regional demand.

Latin America

Latin America is an emerging hydration products market, led by Brazil and Mexico. Rising urbanization, increasing disposable incomes, and growing awareness of sports and fitness nutrition are driving demand for bottled water and flavored hydration beverages. Expanding urban populations, improving retail infrastructure, and rising adoption of sports and flavored hydration drinks are fueling market growth across the region.

Key Players in the Luxury Hotels Market

- Marriott International

- Hilton Worldwide

- InterContinental Hotels Group (IHG)

- Accor

- Hyatt Hotels Corporation

- Four Seasons Hotels & Resorts

- Mandarin Oriental Hotel Group

- Rosewood Hotel Group

- Shangri-La Hotels & Resorts

- Jumeirah Group