Luxury Handbags Market Size

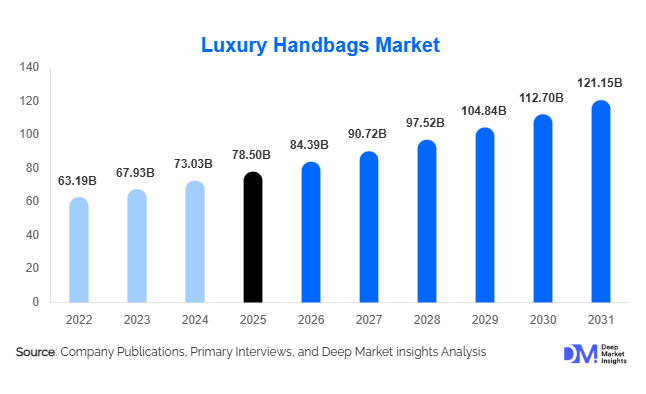

According to Deep Market Insights, the global luxury handbags market size was valued at USD 78.5 billion in 2025 and is projected to grow from USD 84.39 billion in 2026 to reach USD 121.15 billion by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The luxury handbags market growth is primarily driven by rising global affluence, increasing demand for premium fashion accessories, and strong brand positioning by heritage luxury houses. Additionally, the growing influence of social media, celebrity endorsements, and aspirational consumption patterns among millennials and Gen Z consumers is significantly contributing to market expansion.

Key Market Insights

- Leather handbags dominate the market, accounting for nearly 65% share due to their premium quality, durability, and timeless appeal.

- Direct-to-consumer (DTC) channels are rapidly expanding, driven by brand-controlled retail experiences and higher profit margins.

- Europe leads the global market, supported by a strong manufacturing heritage and global luxury brand headquarters.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes and expanding middle-class populations.

- Women consumers account for the majority of demand, contributing over 70% of total market revenue.

- Sustainability and resale markets are emerging as key trends, influencing product design and purchasing behavior.

What are the latest trends in the luxury handbags market?

Rise of Sustainable and Ethical Luxury

Sustainability has become a defining trend in the luxury handbags market, with consumers increasingly prioritizing ethically sourced materials and environmentally responsible production processes. Luxury brands are investing in vegan leather, recycled materials, and transparent supply chains to meet evolving consumer expectations. Additionally, circular economy models, including resale and refurbishment programs, are gaining traction, enabling brands to extend product lifecycles while enhancing brand loyalty. Companies are also adopting carbon-neutral manufacturing practices and eco-certifications to strengthen their sustainability credentials.

Digital Transformation and Omnichannel Expansion

The integration of digital technologies is reshaping the luxury handbags market. Brands are leveraging augmented reality (AR), artificial intelligence (AI), and virtual showrooms to enhance customer engagement and personalization. Online luxury sales are growing rapidly, particularly among younger consumers, who prefer seamless digital experiences. Omnichannel strategies combining physical boutiques with e-commerce platforms are enabling brands to deliver consistent and immersive shopping journeys. Social media and influencer marketing are also playing a crucial role in driving brand awareness and purchase decisions.

What are the key drivers in the luxury handbags market?

Growing Global Affluence

The increasing number of high-net-worth individuals and affluent middle-class consumers worldwide is a major driver of the luxury handbags market. Rising disposable incomes, particularly in emerging economies such as China and India, are enabling more consumers to invest in premium accessories. Luxury handbags are increasingly viewed as status symbols and investment assets, further driving demand across diverse consumer segments.

Influence of Social Media and Celebrity Endorsements

Social media platforms and celebrity endorsements have significantly amplified the visibility and desirability of luxury handbags. Influencers and fashion icons play a key role in shaping consumer preferences, with limited-edition collections and collaborations driving urgency and exclusivity. Digital platforms also enable brands to engage directly with consumers, enhancing brand loyalty and accelerating sales growth.

Product Innovation and Premiumization

Continuous innovation in design, materials, and craftsmanship is driving the growth of the luxury handbags market. Brands are introducing customizable products, smart features, and sustainable materials to differentiate themselves in a competitive landscape. Premiumization strategies, including limited-edition releases and exclusive collections, are further enhancing brand value and attracting high-spending consumers.

What are the restraints for the global market?

High Product Costs

The premium pricing of luxury handbags limits market accessibility to a relatively small consumer base. Economic uncertainties and inflationary pressures can impact discretionary spending, leading to fluctuations in demand. High production costs, including expensive raw materials and skilled craftsmanship, further contribute to elevated retail prices.

Proliferation of Counterfeit Products

The widespread availability of counterfeit luxury handbags poses a significant challenge to market growth. Counterfeit products undermine brand equity, reduce revenues, and erode consumer trust. The increasing sophistication of counterfeit manufacturing and online distribution channels makes it difficult for brands to combat this issue effectively.

What are the key opportunities in the luxury handbags industry?

Expansion into Emerging Markets

Emerging markets such as India, Vietnam, and Indonesia present significant growth opportunities for luxury handbag brands. Rapid urbanization, rising disposable incomes, and increasing exposure to global fashion trends are driving demand in these regions. Companies that adopt localized strategies and expand their retail presence can capitalize on this growing consumer base.

Growth of Circular and Resale Economy

The expanding resale and rental markets for luxury handbags are creating new revenue streams for brands. Certified pre-owned platforms and buy-back programs are gaining popularity, allowing consumers to access luxury products at lower price points while promoting sustainability. This trend is also enhancing brand loyalty and extending product lifecycles.

Technological Integration in Retail

The adoption of advanced technologies such as AI-driven personalization, blockchain authentication, and AR-based virtual try-ons is transforming the luxury shopping experience. These innovations enable brands to offer personalized services, improve supply chain transparency, and enhance customer engagement, creating competitive advantages in the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 78.5 Billion |

| Market Size in 2026 | USD 84.39 Billion |

| Market Size in 2031 | USD 121.15 Billion |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Tote bags continue to lead the luxury handbags market, accounting for approximately 28% of the total market share in 2025. This dominance is primarily driven by their high functional utility, versatility across professional and casual settings, and increasing preference among working professionals and urban consumers. The growing participation of women in the workforce and demand for multi-functional accessories have significantly strengthened the adoption of tote bags globally. Additionally, brands are innovating with lightweight materials, modular compartments, and minimalist aesthetics, further enhancing their appeal.

Crossbody bags and shoulder bags are witnessing strong growth momentum due to their convenience, portability, and alignment with fast-paced urban lifestyles. These segments are particularly popular among millennials and Gen Z consumers who prioritize mobility and compact designs. Meanwhile, clutches and evening bags cater to niche, high-value segments driven by luxury events, weddings, and formal occasions, often commanding premium pricing due to intricate craftsmanship and limited-edition designs. Luxury backpacks are an emerging category, gaining traction among younger consumers and business travelers seeking a combination of comfort, practicality, and premium styling.

Material Insights

Leather remains the dominant material segment, contributing approximately 65% of the global market share in 2025. Its leadership is driven by superior durability, premium texture, and strong association with traditional luxury craftsmanship. Full-grain and top-grain leather products are particularly valued for their longevity and ability to retain aesthetic appeal over time, making them preferred choices for high-end consumers. The perception of leather handbags as long-term investments further reinforces their market dominance.

Exotic materials such as crocodile, ostrich, and python skins cater to ultra-luxury segments, where exclusivity and rarity are key purchasing drivers. However, increasing regulatory scrutiny and ethical concerns are moderating their growth. In contrast, vegan leather and advanced synthetic materials are emerging as fast-growing segments, driven by sustainability trends and shifting consumer preferences toward eco-conscious products. Textile-based handbags, including canvas and jacquard, are also gaining traction, particularly in entry-level luxury segments, due to their affordability, lightweight nature, and adaptability to seasonal fashion trends.

Distribution Channel Insights

Direct-to-consumer (DTC) channels dominate the luxury handbags market, accounting for approximately 45% of total sales. This segment’s leadership is driven by brands’ strategic focus on maintaining control over pricing, customer experience, and brand positioning. Brand-owned boutiques and official websites offer exclusive collections, customization options, and personalized services, which significantly enhance customer loyalty and margins.

Multi-brand retail stores and department stores continue to play a critical role, particularly in mature markets such as North America and Europe, where consumers value curated selections and physical shopping experiences. However, online luxury platforms are the fastest-growing distribution channel, fueled by increasing digital adoption, improved logistics, and the growing influence of social commerce. The integration of AI-driven recommendations, virtual try-ons, and seamless omnichannel experiences is further accelerating the shift toward online channels.

Consumer Insights

Women remain the dominant consumer segment, contributing over 72% of total market revenue in 2025. This leadership is driven by the strong cultural and fashion significance of handbags in women’s wardrobes, as well as higher purchase frequency compared to other demographics. Luxury handbags are often perceived as both fashion statements and status symbols, reinforcing consistent demand within this segment.

The men’s segment is expanding steadily, supported by evolving fashion norms and increasing acceptance of luxury accessories among male consumers. Growth is particularly notable in urban markets where professional and lifestyle trends encourage the adoption of premium accessories. Additionally, gender-neutral and unisex designs are emerging as a key trend, appealing to younger, fashion-forward consumers who value inclusivity and versatility in product offerings.

Usage Insights

Everyday and workwear handbags dominate the usage segment, accounting for approximately 40% of the market. Their leadership is driven by high usage frequency, practicality, and alignment with professional lifestyles. Consumers increasingly prefer handbags that combine functionality with premium aesthetics, leading to strong demand for structured designs with ample storage capacity.

Occasion-based handbags, including clutches and evening bags, cater to premium and niche segments, often characterized by higher margins and lower volume sales. These products are driven by demand from social events, weddings, and luxury gatherings. Meanwhile, travel and utility handbags are gaining popularity among frequent travelers and professionals, supported by the growth of global tourism and business travel. Features such as durability, lightweight construction, and multi-functionality are key drivers in this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Luxury Handbags Market Segmentations

By Product Type

- Tote Bags

- Shoulder Bags

- Satchels

- Clutches & Evening Bags

- Crossbody Bags

- Luxury Backpacks

- Others

By Material

- Leather

- Vegan Leather / Synthetic Materials

- Textile-Based

- Exotic Materials

By Distribution Channel

- Direct-to-Consumer

- Multi-brand Retail Stores

- Online Luxury Platforms

- Duty-Free & Travel Retail

By Consumer Demographics

- Women

- Men

- Unisex / Gender-neutral

By Usage

- Everyday / Workwear

- Travel & Utility

- Occasion / Evening

Regional Insights

Europe

Europe leads the global luxury handbags market, accounting for approximately 35% of total revenue in 2025. The region’s dominance is driven by its strong heritage in luxury craftsmanship, with countries such as France and Italy serving as global hubs for design, manufacturing, and brand headquarters. The presence of established luxury houses, combined with high export volumes, significantly contributes to regional growth.

Key growth drivers in Europe include strong inbound tourism, particularly from Asia and North America, which boosts retail sales in major fashion capitals such as Paris and Milan. Additionally, the region benefits from a well-established supply chain, skilled labor, and government support for luxury manufacturing. Increasing demand for sustainable and ethically produced luxury goods is also shaping product innovation and consumer preferences in the region.

Asia-Pacific

Asia-Pacific accounts for around 30% of the global market and is the fastest-growing region, with a CAGR exceeding 9%. China remains the largest market, driven by a rapidly expanding affluent population, strong domestic consumption, and government policies encouraging local spending. The shift from overseas luxury purchases to domestic consumption is further boosting regional sales.

India is emerging as a high-growth market due to rising disposable incomes, urbanization, and increasing exposure to global luxury brands. Southeast Asian countries such as Vietnam and Indonesia are also witnessing strong growth, supported by expanding middle-class populations. Japan, while mature, continues to contribute stable demand driven by high purchasing power and brand loyalty. Digital adoption, social media influence, and the expansion of luxury retail infrastructure are key growth drivers across the region.

North America

North America holds approximately 20% of the global market share, with the United States being the primary contributor. The region’s growth is driven by high consumer spending, a strong culture of premium consumption, and the presence of major luxury brands. The U.S. market, in particular, benefits from a large base of high-net-worth individuals and aspirational consumers.

Key drivers include the rapid adoption of e-commerce and omnichannel retail strategies, which have significantly enhanced accessibility and customer engagement. Additionally, the influence of celebrity culture and social media plays a crucial role in shaping consumer preferences. The growing demand for sustainable luxury products and resale platforms is also contributing to market expansion in North America.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of the global market, led by the UAE and Saudi Arabia. The region’s growth is driven by high per capita income, a strong luxury consumption culture, and significant investments in retail infrastructure, including luxury malls and shopping destinations. Luxury tourism is a major driver, with cities such as Dubai serving as global shopping hubs, attracting international consumers. Additionally, government initiatives aimed at economic diversification, such as Saudi Arabia’s Vision 2031, are supporting the expansion of the luxury retail sector. The presence of tax-free shopping and high spending by affluent local populations further strengthens demand in the region.

Latin America

Latin America contributes approximately 7% of the global luxury handbags market, with Brazil and Mexico being the key markets. While growth remains moderate compared to other regions, increasing brand penetration and rising consumer awareness are supporting market expansion. Key growth drivers include gradual economic recovery, increasing urbanization, and the expansion of international luxury brands into the region. Additionally, the growing influence of digital platforms and social media is enhancing consumer exposure to global fashion trends. However, challenges such as currency volatility and import duties continue to impact pricing and demand dynamics in the region.