Luxury Gift Packaging Market Size

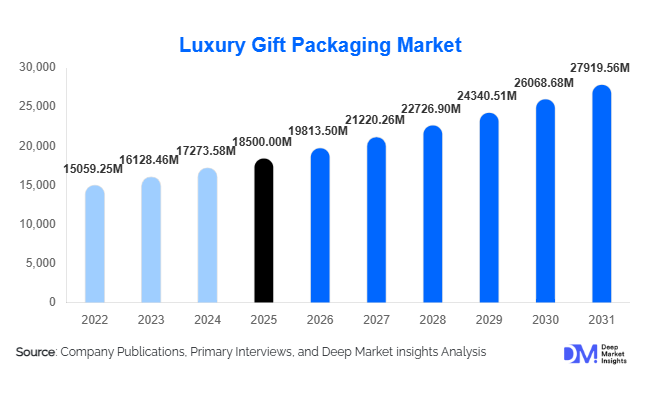

According to Deep Market Insights, the global luxury gift packaging market size was valued at USD 18,500 million in 2025 and is projected to grow from USD 19,813.50 million in 2026 to reach USD 27,919.56 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The market growth is primarily driven by increasing premiumization across consumer goods, rising demand for aesthetically appealing packaging, and the expanding influence of gifting culture across personal and corporate segments.

Key Market Insights

- Luxury packaging is evolving into a brand experience tool, enhancing product value through design, materials, and unboxing appeal.

- Sustainable luxury packaging is gaining traction, with increased use of recyclable paperboard, biodegradable materials, and reusable designs.

- Asia-Pacific dominates the market, supported by strong demand from China and India due to rising disposable incomes and gifting traditions.

- The Middle East is the fastest-growing region, driven by high luxury consumption and a premium gifting culture.

- Customization and personalization trends are accelerating adoption, especially in corporate gifting and premium retail.

- Advanced printing technologies, including digital printing and foil stamping, are enabling cost-effective premium finishes.

What are the latest trends in the luxury gift packaging market?

Sustainable and Eco-Friendly Packaging Innovations

Sustainability has become a defining trend in the luxury gift packaging market. Brands are increasingly adopting recyclable paperboard, biodegradable coatings, and reusable packaging formats to align with environmental regulations and consumer expectations. Premium brands are innovating with molded pulp packaging, plant-based inks, and minimalistic designs that reduce waste while maintaining a luxury aesthetic. Many companies are also introducing refillable packaging and multi-use gift boxes, enhancing product lifecycle value and reducing environmental impact. This shift is particularly strong in Europe and North America, where regulatory frameworks and consumer awareness are highest.

Personalization and Smart Packaging Integration

Customization is rapidly transforming the luxury packaging landscape. Brands are leveraging digital printing technologies to offer personalized packaging with names, messages, and limited-edition designs. Additionally, smart packaging solutions such as QR codes, NFC tags, and augmented reality features are being integrated to enhance consumer engagement. These technologies enable brands to provide interactive experiences, product authentication, and storytelling, making packaging an extension of the product itself. This trend is particularly popular among younger consumers and in e-commerce-driven luxury retail.

What are the key drivers in the luxury gift packaging market?

Growth in Global Luxury Goods Consumption

The increasing consumption of luxury goods across cosmetics, fashion, jewelry, and premium food sectors is a major driver of the market. Rising disposable incomes, urbanization, and aspirational lifestyles in emerging economies are fueling demand for premium products, which require high-quality packaging to match brand positioning. Luxury packaging plays a critical role in enhancing perceived value and influencing purchasing decisions.

Expansion of E-commerce and Premium Unboxing Experience

The rapid growth of e-commerce has made packaging a crucial touchpoint in the customer journey. Premium packaging enhances the unboxing experience, which has become a key marketing factor, especially on social media platforms. Brands are investing in innovative designs and materials to create memorable experiences that drive customer loyalty and brand recognition.

What are the restraints for the global market?

High Cost of Premium Materials and Production

Luxury gift packaging involves high-quality materials such as rigid paperboard, metal, glass, and specialty coatings, which significantly increase production costs. Advanced printing and finishing techniques further add to expenses, limiting adoption among smaller brands and reducing price competitiveness.

Sustainability Compliance Challenges

While sustainability is a key trend, transitioning to eco-friendly materials without compromising luxury aesthetics remains challenging. Manufacturers face difficulties in balancing cost, durability, and visual appeal while adhering to stringent environmental regulations.

What are the key opportunities in the luxury gift packaging industry?

Rising Demand in Emerging Markets

Emerging economies such as China, India, and the UAE present significant growth opportunities due to increasing disposable incomes and strong gifting cultures. International luxury brands entering these markets are investing heavily in premium packaging to cater to local preferences and enhance brand appeal.

Integration of Smart and Interactive Packaging

The adoption of smart technologies such as QR codes, NFC, and augmented reality offers new opportunities for consumer engagement. These features enable brands to provide product information, authentication, and immersive experiences, transforming packaging into a digital marketing tool.

Material Type Insights

Paper and paperboard dominate the luxury gift packaging market, accounting for approximately 42% of the total share in 2025. This leadership is primarily driven by the material’s superior balance of premium aesthetics, structural rigidity, and sustainability compliance. Luxury brands increasingly prefer rigid paperboard for high-end boxes due to its ability to support advanced finishing techniques such as embossing, foil stamping, and lamination. Additionally, growing environmental regulations and consumer preference for recyclable packaging have further strengthened the adoption of paper-based materials globally.

Plastic and acrylic packaging continue to hold relevance in niche applications, particularly in cosmetics and electronics, where product visibility, durability, and moisture resistance are critical. Meanwhile, metal and glass packaging are extensively used in premium beverages, fragrances, and specialty foods, offering a sense of exclusivity and long-term usability. Materials such as wood, fabric, and leather cater to ultra-luxury and artisanal segments, where craftsmanship, reusability, and brand storytelling act as key demand drivers, especially in limited-edition and high-value gifting.

Packaging Type Insights

Luxury boxes represent the largest segment, holding nearly 48% of the global market share, driven by their widespread application across high-value industries such as jewelry, electronics, cosmetics, and premium gifting. The dominance of this segment is attributed to its structural integrity, customization flexibility, and ability to enhance perceived product value. Formats such as magnetic closure boxes, drawer-style boxes, and rigid hinged boxes are particularly popular due to their premium feel and reusability.

Bags and wrapping solutions also contribute significantly, especially in retail environments and seasonal gifting occasions. However, the fastest growth is being observed in customized and personalized packaging, where brands are leveraging unique designs, branding elements, and consumer-specific features to differentiate themselves. This trend is strongly supported by the rise of e-commerce and corporate gifting, where packaging plays a crucial role in customer experience and brand recall.

Printing & Decoration Technology Insights

Foil stamping and embossing technologies collectively account for around 30% of the market share, as they are essential in delivering the tactile and visual richness associated with luxury packaging. These techniques enable brands to create distinctive textures, metallic finishes, and high-end detailing, which significantly enhance shelf appeal and consumer perception.

Digital printing is emerging as the fastest-growing segment, driven by its ability to support short-run production, rapid prototyping, and cost-effective customization. This is particularly beneficial for limited-edition products and personalized gifting solutions. Additionally, UV coatings and lamination technologies are widely adopted to improve durability, gloss, and resistance to environmental factors, ensuring that packaging maintains its premium appearance throughout the product lifecycle.

End-Use Industry Insights

The cosmetics and personal care segment leads the market with approximately 28% share, driven by the global expansion of premium skincare, fragrance, and beauty products. Packaging in this segment is a critical differentiator, influencing consumer purchase decisions through design, texture, and branding. The increasing demand for clean beauty and luxury skincare products is further amplifying the need for high-quality, sustainable packaging solutions.

The food and beverages segment, particularly premium confectionery, gourmet foods, and alcoholic beverages, is among the fastest-growing end-use categories. Growth is fueled by seasonal gifting trends, festive demand, and the premiumization of consumables. Jewelry, fashion, and electronics industries also contribute significantly, as these sectors rely heavily on packaging to enhance product value, protect delicate items, and create memorable unboxing experiences.

Distribution Channel Insights

Direct B2B channels dominate the market with approximately 55% share, as luxury brands prefer close collaboration with packaging manufacturers to ensure design precision, material quality, and brand consistency. This channel enables high levels of customization and supports long-term partnerships between brands and suppliers.

Retail and e-commerce channels are witnessing steady growth, particularly for standardized and small-batch packaging solutions. The rise of online platforms has enabled easier access to customized packaging services, especially for small and medium-sized enterprises and direct-to-consumer brands. Additionally, digital platforms are facilitating design visualization and rapid ordering, further accelerating adoption in this segment.

| By Material Type | By Packaging Type | By Printing & Decoration Technology | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global luxury gift packaging market with approximately 38% share in 2025, driven by a combination of strong manufacturing capabilities and rising domestic consumption. China alone contributes over 20% of global demand, supported by its large luxury consumer base, expanding middle class, and dominance in packaging production. Key growth drivers in the region include rapid urbanization, increasing disposable incomes, strong cultural emphasis on gifting, and the expansion of e-commerce platforms. India is emerging as a high-growth market due to festive gifting traditions, rising premium consumption, and government initiatives supporting domestic manufacturing. Japan and South Korea contribute through innovation and high-quality packaging standards.

North America

North America accounts for around 25% of the global market, with the United States being the primary contributor. The region’s growth is driven by high consumer spending on luxury goods, a strong presence of global premium brands, and a mature e-commerce ecosystem. Additionally, the increasing importance of branding and unboxing experiences in direct-to-consumer sales is fueling demand for premium packaging solutions. Sustainability trends and regulatory pressures are also encouraging the adoption of eco-friendly luxury packaging across industries.

Europe

Europe holds approximately 22% market share, led by countries such as France, Italy, and Germany. The region’s growth is supported by its strong heritage in luxury goods, high concentration of premium brands, and advanced packaging design capabilities. Sustainability is a key driver, with strict environmental regulations and consumer preference for eco-friendly products pushing innovation in recyclable and biodegradable packaging. Additionally, Europe’s leadership in fashion, cosmetics, and premium beverages continues to drive consistent demand for high-end packaging solutions.

Middle East & Africa

The Middle East is the fastest-growing region, with a CAGR exceeding 8%, driven by countries such as the UAE and Saudi Arabia. Growth is fueled by high disposable incomes, strong luxury consumption, and a deeply rooted gifting culture, particularly during festivals and special occasions. The region also benefits from a growing retail and tourism sector, which boosts demand for premium packaging. In Africa, growth is supported by export-oriented manufacturing and increasing participation in global supply chains, particularly in packaging production hubs.

Latin America

Latin America accounts for around 7% of the global market, with Brazil and Mexico leading demand. The region’s growth is driven by urbanization, an expanding middle-class population, and increasing adoption of premium consumer goods. Additionally, the rise of modern retail formats and e-commerce platforms is supporting the demand for visually appealing and high-quality packaging. While still emerging, the region presents opportunities for growth as consumer preferences shift toward premiumization and branded gifting experiences.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Luxury Gift Packaging Market

- DS Smith Plc

- Smurfit Kappa Group

- WestRock Company

- International Paper Company

- Mondi Group

- Stora Enso

- Huhtamaki Oyj

- Amcor Plc

- Crown Holdings

- Mayr-Melnhof Karton AG

- Rengo Co., Ltd.

- Graphic Packaging Holding Company

- Sealed Air Corporation

- AR Packaging Group

- Packlane