Luxury Footwear Market Size

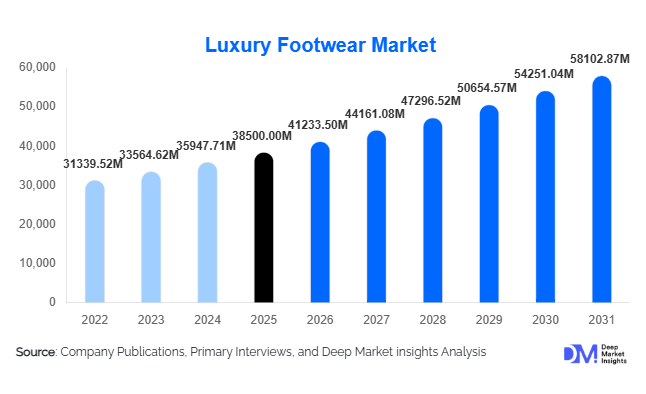

According to Deep Market Insights, the global luxury footwear market size was valued at USD 38,500 million in 2025 and is projected to grow from USD 41,233.50 million in 2026 to reach USD 58,102.87 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The luxury footwear market growth is primarily driven by increasing global affluence, rising demand for premium fashion products, and the rapid expansion of digital retail channels that enhance accessibility to luxury brands.

Key Market Insights

- Luxury footwear is increasingly influenced by athleisure trends, with premium sneakers emerging as a dominant category globally.

- Asia-Pacific is the fastest-growing market, driven by rising disposable incomes and expanding middle-class populations in China and India.

- Europe remains the largest market, supported by heritage luxury brands and strong export-oriented production.

- Direct-to-consumer (DTC) channels are rapidly expanding, enabling brands to improve margins and customer engagement.

- Sustainability and ethical sourcing are becoming critical purchase drivers, especially among younger consumers.

- Limited-edition collaborations and celebrity endorsements are boosting brand desirability and driving premium pricing.

What are the latest trends in the luxury footwear market?

Rise of Luxury Sneakers and Athleisure

The growing influence of casual fashion has led to a surge in demand for luxury sneakers and athleisure footwear. Consumers increasingly prioritize comfort without compromising on style, prompting luxury brands to expand their sneaker portfolios. Collaborations between luxury houses and sportswear brands are becoming common, creating high-demand limited-edition products. This trend is particularly strong among millennials and Gen Z consumers, who prefer versatile footwear suitable for both casual and semi-formal settings. As a result, sneakers now account for a significant share of luxury footwear sales globally.

Sustainable and Vegan Footwear Innovation

Sustainability has become a defining trend in the luxury footwear market. Brands are adopting eco-friendly materials such as vegan leather, recycled textiles, and bio-based polymers to meet consumer expectations. Transparency in sourcing and ethical production practices is gaining importance, with companies investing in sustainable supply chains. This trend is also supported by regulatory pressures and growing environmental awareness, making sustainability a key differentiator in the competitive landscape.

What are the key drivers in the luxury footwear market?

Rising Global Affluence and Aspirational Buying

The increasing number of high-net-worth individuals and the expanding middle-class population are driving demand for luxury footwear. Aspirational consumers, particularly in emerging markets, are contributing significantly to market growth by purchasing entry-level luxury products. This shift has broadened the customer base beyond traditional elite segments.

Expansion of E-commerce and Omnichannel Retail

The growth of online retail platforms has transformed the luxury shopping experience. Brands are leveraging digital channels to reach global consumers, offering personalized experiences through AI-driven recommendations and virtual try-ons. Omnichannel strategies that integrate physical stores with online platforms are enhancing customer engagement and driving sales growth.

What are the restraints for the global market?

High Price Sensitivity in Emerging Markets

Despite growing demand, high product prices remain a barrier for widespread adoption in developing regions. While aspirational consumers are increasing, affordability constraints limit penetration of ultra-luxury products, particularly in price-sensitive markets.

Proliferation of Counterfeit Products

The presence of counterfeit luxury footwear poses a significant challenge to market growth. Fake products not only impact brand reputation but also lead to revenue losses. The rise of online marketplaces has further exacerbated this issue, making it difficult for brands to control distribution channels effectively.

What are the key opportunities in the luxury footwear industry?

Expansion in Emerging Markets

Emerging economies such as China, India, and Southeast Asian countries present significant growth opportunities. Increasing urbanization, rising disposable incomes, and a growing appetite for premium products are driving demand. Brands can capitalize on this by introducing localized designs and entry-level luxury offerings tailored to regional preferences.

Digital Transformation and Direct-to-Consumer Models

The shift toward direct-to-consumer sales channels enables brands to improve margins and strengthen customer relationships. Investments in digital platforms, data analytics, and personalized marketing strategies are helping companies enhance customer engagement and drive repeat purchases.

Sustainable Product Development

The growing demand for eco-friendly products presents an opportunity for innovation in materials and manufacturing processes. Brands that prioritize sustainability can attract environmentally conscious consumers and differentiate themselves in the competitive market.

Product Type Insights

Casual luxury footwear, particularly sneakers, dominates the global market, accounting for approximately 32% of the total market share in 2025. The leadership of this segment is primarily driven by the structural shift in global fashion toward comfort, versatility, and everyday luxury. The growing influence of streetwear culture, celebrity collaborations, and limited-edition drops has significantly elevated sneakers from functional footwear to high-value fashion statements. Additionally, the integration of premium materials and craftsmanship into casual designs has blurred the line between luxury and sportswear, further accelerating demand.

Formal footwear continues to maintain stable demand, particularly among business professionals and affluent consumers seeking timeless elegance. However, its growth is comparatively moderate due to the global shift toward relaxed dress codes in corporate environments. Boots and sandals play an important role in regional and seasonal demand, with boots seeing higher adoption in North America and Europe, while luxury sandals and slides are gaining popularity in warmer regions such as the Middle East and Asia-Pacific. The athleisure luxury segment is emerging as one of the fastest-growing categories, driven by increasing health awareness, hybrid lifestyles, and the demand for multifunctional footwear suitable for both casual and semi-formal settings.

End-User Insights

Women remain the dominant consumer segment in the luxury footwear market, contributing approximately 55% of the global market share in 2025. This leadership is supported by a broader product portfolio, higher fashion sensitivity, and more frequent purchase cycles compared to other segments. Luxury brands consistently prioritize women’s collections in terms of design innovation, seasonal launches, and marketing investments, further strengthening segment dominance.

The men’s segment is witnessing faster growth, fueled by increasing fashion consciousness, rising disposable incomes, and the growing acceptance of luxury fashion among male consumers. The expansion of premium sneaker culture and formal-casual hybrid footwear has particularly boosted demand in this segment. Meanwhile, the children’s luxury footwear segment, although relatively niche, is gaining momentum among high-net-worth families. This growth is driven by premiumization trends, brand-conscious parenting, and the increasing availability of luxury mini-collections that replicate adult designs.

Material Insights

Leather continues to dominate the luxury footwear market, accounting for approximately 68% of the total market share in 2025. Its leadership is attributed to superior durability, premium aesthetics, and long-standing associations with craftsmanship and heritage luxury. High-quality variants such as full-grain leather, suede, and patent leather are widely used by leading brands to maintain exclusivity and justify premium pricing.

However, non-leather materials are witnessing accelerated growth due to evolving consumer preferences and sustainability concerns. Vegan leather, recycled fabrics, and bio-based materials are increasingly being adopted as brands align with environmental regulations and consumer demand for ethical products. This shift is particularly prominent among younger demographics, who prioritize sustainability alongside style. As a result, innovation in alternative materials is expected to play a crucial role in shaping future market dynamics.

Distribution Channel Insights

Offline retail channels continue to dominate the luxury footwear market, holding approximately 60% of the total market share in 2025. The dominance of physical retail is driven by the experiential nature of luxury shopping, where personalized service, brand ambiance, and product trials play a critical role in purchase decisions. Flagship stores, luxury malls, and boutique outlets remain key touchpoints for high-value transactions.

However, online channels are rapidly gaining traction and represent the fastest-growing distribution segment. The increasing adoption of e-commerce platforms, combined with advancements in digital technologies such as virtual try-ons, AI-driven recommendations, and seamless return policies, is transforming consumer purchasing behavior. Luxury brands are increasingly adopting omnichannel strategies to integrate online and offline experiences, ensuring consistent brand engagement across multiple touchpoints. Direct-to-consumer platforms are also enabling brands to improve margins and gain better control over customer relationships.

| By Product Type | By End User | By Material | By Price Range | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Europe

Europe leads the global luxury footwear market, accounting for approximately 35% of the total market share in 2025. The region’s dominance is driven by its strong heritage in luxury craftsmanship, with countries such as Italy, France, and the United Kingdom serving as global hubs for premium footwear manufacturing and design. Italy, in particular, remains a key exporter due to its expertise in leather craftsmanship and high-quality production. Additionally, the presence of leading luxury fashion houses, established brand equity, and strong intra-regional demand support market growth. Tourism also plays a significant role, with international travelers contributing substantially to luxury retail sales across major European cities.

North America

North America holds around 28% of the global market share, with the United States being the primary contributor. The region’s growth is driven by high disposable incomes, a well-established luxury retail ecosystem, and strong consumer affinity for premium brands. The increasing influence of celebrity culture and social media marketing further boosts demand for luxury footwear. Additionally, the rapid expansion of e-commerce and direct-to-consumer channels has enhanced accessibility to luxury products. The growing popularity of athleisure and premium sneakers is a key driver in this region, particularly among younger consumers.

Asia-Pacific

Asia-Pacific accounts for approximately 25% of the global market and is the fastest-growing region, with a CAGR of around 9%. China and India are the primary growth engines, supported by rising middle-class incomes, rapid urbanization, and increasing exposure to global fashion trends. In China, strong demand is driven by brand-conscious consumers and a robust digital retail ecosystem. India is emerging as a high-potential market due to its expanding affluent population and increasing penetration of luxury brands. Additionally, favorable government policies, growing retail infrastructure, and the influence of social media are accelerating market expansion across the region.

Middle East & Africa

The Middle East & Africa region contributes approximately 7% of the global market share, with the UAE and Saudi Arabia leading demand. Growth in this region is driven by high per capita income, strong preference for luxury goods, and a well-developed retail infrastructure featuring premium malls and luxury shopping destinations. The influx of international tourists, particularly in cities like Dubai, further boosts demand. Additionally, cultural preferences for premium and designer products, along with increasing investments in retail and tourism sectors, are supporting sustained market growth.

Latin America

Latin America holds a smaller share of approximately 5% of the global market, with Brazil and Mexico as the key contributors. The region’s growth is supported by increasing urbanization, rising disposable incomes, and growing awareness of global luxury brands. Although economic volatility remains a challenge, the expansion of organized retail and e-commerce platforms is improving market accessibility. Additionally, a growing young population with rising fashion consciousness is expected to drive future demand for luxury footwear in this region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|