Luxury Children’s Clothing Market Size

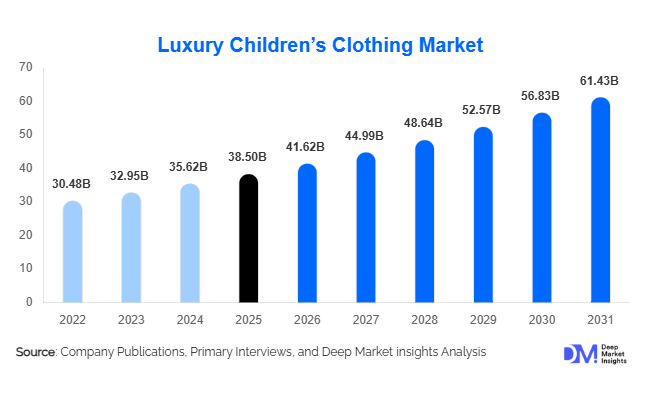

According to Deep Market Insights, the global luxury children’s clothing market size was valued at USD 38.5 billion in 2025 and is projected to grow from USD 41.62 billion in 2026 to reach USD 61.43 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The market growth is primarily driven by rising disposable incomes, increasing brand consciousness among millennial and Gen Z parents, and the growing premiumization of children’s fashion. Expanding digital retail ecosystems and strong demand from emerging economies are further accelerating global market expansion.

Key Market Insights

- Luxury children’s apparel dominates the market, accounting for over 60% share due to high demand for formal and occasion wear.

- Offline retail remains dominant, contributing nearly 58% of total sales, driven by preference for personalized shopping experiences.

- Europe leads the global market, supported by strong brand heritage and luxury fashion houses.

- Asia-Pacific is the fastest-growing region, fueled by rising affluence in China and India.

- Sustainability is becoming a key differentiator, with increasing demand for organic and ethically sourced materials.

- Digital transformation and DTC channels are reshaping consumer engagement and expanding global reach.

What are the latest trends in the luxury children’s clothing market?

Rise of Sustainable and Ethical Fashion

Sustainability has become a defining trend in the luxury children’s clothing market. Parents are increasingly prioritizing organic fabrics, non-toxic dyes, and environmentally responsible production processes. Luxury brands are responding by launching eco-friendly collections that emphasize transparency and ethical sourcing. Certifications, recyclable packaging, and circular fashion models such as resale and rental platforms are gaining traction. This trend is particularly strong in Europe and North America, where regulatory pressure and consumer awareness are highest, pushing brands toward greener practices.

Digitalization and Personalized Shopping Experiences

The integration of advanced technologies is transforming how consumers engage with luxury children’s fashion. AI-driven personalization, virtual try-ons, and exclusive online product drops are enhancing customer experience. Social media platforms and influencer marketing are playing a crucial role in shaping purchasing decisions. Brands are investing in omnichannel strategies, combining physical stores with seamless digital interfaces. This shift is enabling global reach while maintaining exclusivity, especially appealing to tech-savvy younger parents.

What are the key drivers in the luxury children’s clothing market?

Growing Disposable Income and Urbanization

Rising income levels, particularly in urban areas, are significantly boosting demand for premium children’s apparel. Dual-income households are increasingly willing to spend on high-quality and branded products for their children. Emerging economies are witnessing rapid growth in affluent middle-class populations, further expanding the consumer base.

Influence of Social Media and Celebrity Culture

Social media platforms and celebrity endorsements have elevated the visibility of luxury children’s brands. Influencers and celebrity families showcasing premium children’s fashion have normalized high-end consumption in this segment. This trend has amplified brand awareness and accelerated demand across global markets.

Product Innovation and Premiumization

Luxury brands are continuously innovating in design, materials, and exclusivity. Limited-edition collections, customization options, and seasonal launches are driving repeat purchases. High-quality fabrics and superior craftsmanship justify premium pricing, reinforcing brand loyalty among consumers.

What are the restraints for the global market?

High Price Sensitivity in Emerging Markets

Despite growing demand, luxury children’s clothing remains expensive, limiting its adoption among middle-income consumers. Price sensitivity is particularly evident in emerging markets, where discretionary spending is more constrained.

Short Product Lifecycle

Children outgrow clothing quickly, reducing the perceived value of high-priced apparel. This creates hesitation among consumers and challenges brands to innovate through durability, resale options, and rental models.

What are the key opportunities in the luxury children’s clothing industry?

Expansion in Emerging Markets

Asia-Pacific and the Middle East present significant growth opportunities due to rising affluence and expanding luxury consumer bases. Early market entry and localized product offerings can help brands capture untapped demand.

Growth of Direct-to-Consumer Channels

Digital platforms are enabling brands to directly connect with consumers, reducing reliance on intermediaries. AI-powered personalization and exclusive online collections are enhancing engagement and driving sales growth.

Premium Gifting and Occasion Wear Demand

The increasing popularity of luxury gifting for events such as weddings, birthdays, and festivals is creating a niche but lucrative segment. Brands can capitalize on this trend by offering curated collections and limited-edition designs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38.5 Billion |

| Market Size in 2026 | USD 41.62 Billion |

| Market Size in 2031 | USD 61.43 Billion |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Apparel dominates the luxury children’s clothing market with approximately 62% share in 2025, primarily driven by strong global demand for formal wear, occasion-specific outfits, and premium casual collections. The leading position of apparel is supported by the increasing frequency of social events such as weddings, celebrations, and school functions, where premium dressing is emphasized. Additionally, the trend of “mini-me” fashion, where children’s clothing mirrors adult luxury collections, has significantly boosted demand for designer apparel. Casual luxury wear is also expanding rapidly, reflecting a shift toward everyday premiumization, where parents seek comfort combined with brand value. Footwear, while representing a smaller share, is gaining traction due to brand extensions by major luxury houses into children’s categories, offering coordinated styling options. Accessories, including bags, headwear, and belts, are emerging as high-margin add-ons, particularly in gifting segments, where complete luxury ensembles are preferred.

Age Group Insights

The 6–12 years segment leads the market with around 34% share, driven by higher participation in social, academic, and extracurricular activities that require diverse and frequently updated wardrobes. This age group is also more influenced by peer trends, social media exposure, and brand visibility, making it a key revenue-generating segment for luxury brands. The teenage segment (13–16 years) is witnessing accelerated growth due to increasing fashion consciousness and early brand adoption, often influenced by digital platforms and celebrity culture. Meanwhile, the infant (0–2 years) and toddler (3–5 years) segments are largely driven by gifting trends, premiumization of baby care products, and parental preference for high-quality, safe, and organic materials. The emotional purchasing factor is particularly strong in these segments, supporting steady demand despite higher price points.

Distribution Channel Insights

Offline retail channels account for nearly 58% of the market, maintaining dominance due to the experiential nature of luxury shopping. Consumers prefer physical stores for personalized services, product authenticity verification, and immersive brand experiences. Flagship stores, luxury boutiques, and department stores play a crucial role in reinforcing brand identity and exclusivity. The leading position of offline retail is also supported by high-value purchases, where consumers seek assurance of quality and fit. However, online channels are rapidly expanding, driven by increasing digital adoption, especially among younger parents. E-commerce platforms and brand-owned websites are enabling global accessibility, offering curated collections and exclusive online launches. The integration of omnichannel strategies, such as click-and-collect, virtual consultations, and seamless inventory visibility, is becoming a key growth driver, bridging the gap between physical and digital retail.

End-Use Insights

Individual consumers dominate the market with over 85% share, driven by direct purchases from parents and families who prioritize quality, comfort, and brand value for their children. The leading position of this segment is reinforced by rising disposable incomes and increasing inclination toward premium lifestyle products. The gifting and events segment is the fastest-growing, supported by cultural and social practices where luxury children’s clothing is purchased for occasions such as weddings, birthdays, and festivals. This segment is particularly strong in Asia-Pacific and the Middle East, where gifting culture is deeply embedded. Institutional demand, including fashion shows, brand campaigns, and luxury events, remains niche but is steadily expanding as children’s fashion gains visibility in global fashion circuits and digital media platforms.

Explore more data points, trends and opportunities Download Free Sample Report

Luxury Children’s Clothing Market Segmentations

By Product Type

- Apparel

- Footwear

- Accessories

By Age Group

- Infants

- Toddlers

- Kids

- Teenagers

By Distribution Channel

- Offline Retail

- Online Retail

By Price Tier

- Ultra-Luxury

- Premium Luxury

By End-Use

- Individual Consumers

- Institutional Buyers

Regional Insights

North America

North America holds approximately 28% of the market share, with the United States as the primary contributor. Growth in this region is driven by high disposable income, a strong culture of premium consumption, and widespread adoption of e-commerce platforms. The presence of established luxury retail infrastructure and a mature consumer base supports consistent demand. Additionally, increasing preference for sustainable and ethically produced clothing is influencing purchasing decisions. The region also benefits from strong brand loyalty and high spending on children’s lifestyle products, further reinforcing its market position.

Europe

Europe dominates the global market with around 32% share in 2025, led by key countries such as France, Italy, and the UK. The region’s leadership is primarily driven by its deep-rooted luxury fashion heritage and the presence of globally renowned fashion houses. Tourism-driven retail sales significantly contribute to demand, particularly in fashion capitals like Paris and Milan. Additionally, strong regulatory frameworks promoting sustainability and product quality are encouraging innovation in eco-friendly children’s clothing. High brand consciousness among consumers and a well-established retail ecosystem continue to drive steady growth in this region.

Asia-Pacific

Asia-Pacific accounts for approximately 25% of the market and is the fastest-growing region, with a CAGR exceeding 9%. China leads regional demand, followed by India and Japan. Growth is primarily driven by rapid urbanization, rising disposable incomes, and the expansion of affluent middle-class populations. Increasing exposure to global fashion trends through digital platforms and social media is accelerating brand adoption. Additionally, strong gifting culture and a growing number of high-net-worth individuals are fueling demand for luxury children’s clothing. Government initiatives supporting retail expansion and e-commerce growth are further enhancing market accessibility.

Latin America

Latin America holds about 7% share, with Brazil and Mexico as key markets. Growth in this region is supported by increasing urbanization, rising disposable incomes among affluent consumers, and the gradual expansion of luxury retail presence. While the market is still developing, growing awareness of global fashion trends and the increasing influence of social media are driving demand for premium children’s apparel. Import-driven availability of luxury brands and expansion of high-end shopping malls are also contributing to market growth.

Middle East & Africa

The Middle East & Africa region contributes around 8% of the market, driven by high spending on luxury goods in countries such as the UAE and Saudi Arabia. The region’s growth is strongly influenced by a deeply rooted gifting culture, high per capita income, and preference for premium lifestyle products. Luxury malls and retail destinations in cities like Dubai serve as key demand hubs. Additionally, tourism and expatriate populations contribute significantly to sales. In Africa, growth is more gradual but supported by increasing urbanization and rising awareness of luxury brands. The region’s strong inclination toward occasion-based spending continues to drive demand for luxury children’s clothing.