Lunch Box Market Size

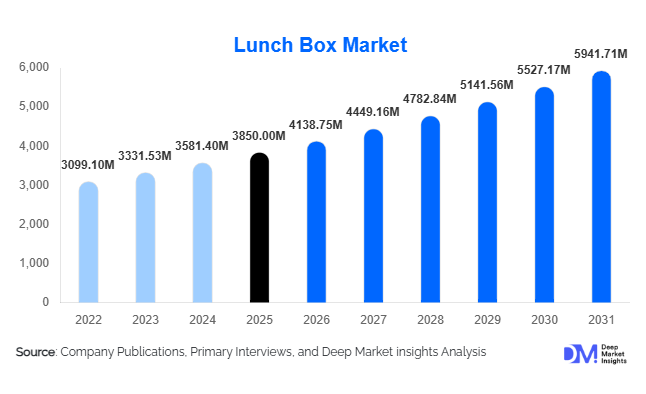

According to Deep Market Insights, the global lunch box market size was valued at USD 3,850 million in 2025 and is projected to grow from USD 4,138.75 million in 2026 to reach USD 5,941.71 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The market growth is primarily driven by increasing health consciousness, rising demand for home-cooked meals, and the expansion of urban working populations globally. Additionally, evolving consumer preferences toward sustainable materials, innovative product designs, and convenience-oriented food storage solutions are accelerating demand across both developed and emerging markets.

Key Market Insights

- Growing preference for home-cooked meals is significantly driving demand for portable and durable lunch box solutions.

- Sustainable and eco-friendly materials such as stainless steel, glass, and bamboo are gaining strong traction over plastic alternatives.

- Asia-Pacific dominates the global market, supported by large population bases and strong cultural inclination toward packaged meals.

- Working professionals represent the largest consumer segment, accounting for over 40% of total demand globally.

- Online retail channels are rapidly expanding, offering wider product variety and customization options.

- Technological innovations, including insulated and electric lunch boxes, are reshaping product differentiation.

What are the latest trends in the lunch box market?

Shift Toward Sustainable and Reusable Materials

Consumers are increasingly prioritizing sustainability, leading to a significant shift away from single-use plastics toward reusable and eco-friendly lunch boxes. Materials such as stainless steel, glass, and bamboo are witnessing rising adoption due to their durability and minimal environmental impact. Governments across regions are also enforcing stricter regulations on plastic usage, further accelerating this trend. Manufacturers are responding by introducing BPA-free, recyclable, and biodegradable product lines. Premium brands are leveraging sustainability as a key differentiator, offering high-quality products with certifications and eco-labels. This trend is particularly strong in Europe and North America, where environmental awareness is high.

Rise of Smart and Functional Lunch Boxes

Innovation in product functionality is transforming the lunch box market. Electric lunch boxes with heating capabilities, vacuum-insulated containers, and leak-proof compartmentalized designs are gaining popularity among urban consumers. These products cater to busy lifestyles, allowing users to store, organize, and reheat meals conveniently. Technological enhancements such as temperature retention and multi-compartment designs are appealing to health-conscious individuals and professionals. The integration of smart features, including app-controlled heating and timers, is expected to gain traction, particularly among tech-savvy consumers.

What are the key drivers in the lunch box market?

Increasing Health Consciousness

The growing awareness of healthy eating habits is a major driver for the lunch box market. Consumers are increasingly opting for home-prepared meals to ensure nutritional quality and hygiene, reducing reliance on outside food. This shift is particularly evident among urban populations and working professionals, driving consistent demand for high-quality lunch boxes.

Growth in the Working Population and the Student Base

The rising number of working professionals and students globally is significantly contributing to market growth. Daily commuting and structured routines necessitate portable food storage solutions, making lunch boxes an essential product category. Emerging economies such as India and China are witnessing particularly strong growth due to demographic expansion and urbanization.

Expansion of E-Commerce Channels

The rapid growth of online retail platforms has enhanced product accessibility and consumer reach. E-commerce enables manufacturers to showcase diverse product offerings, competitive pricing, and customization options. This has boosted sales, particularly in premium and niche segments, and is expected to remain a key growth driver.

What are the restraints for the global market?

Price Sensitivity in Emerging Markets

Despite growing demand for premium products, a significant portion of consumers in developing regions remains price-sensitive. This limits the adoption of high-end lunch boxes and constrains profit margins for manufacturers aiming to scale premium offerings.

Volatility in Raw Material Prices

Fluctuations in the prices of raw materials such as plastics, metals, and glass pose challenges for manufacturers. These variations impact production costs and pricing strategies, potentially affecting profitability and market stability.

What are the key opportunities in the lunch box market?

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific, Latin America, and Africa present significant growth opportunities. Rapid urbanization, increasing disposable incomes, and rising awareness about hygiene are driving demand. Local manufacturing initiatives and government support are further enhancing market penetration in these regions.

Integration of Advanced Technologies

The development of electric and smart lunch boxes presents opportunities for differentiation and premiumization. Features such as self-heating, temperature control, and IoT integration can attract modern consumers and expand usage scenarios, particularly in urban markets.

Customization and Branding Opportunities

Personalized lunch boxes and corporate gifting solutions are emerging as lucrative opportunities. Companies can leverage customization to cater to specific consumer preferences, including school children, fitness enthusiasts, and professionals. Partnerships with meal-prep services and food delivery platforms can further expand market reach.

Product Type Insights

Compartmentalized lunch boxes dominate the global market, accounting for approximately 34% of total demand in 2025. This segment’s leadership is primarily driven by increasing consumer preference for portion-controlled and nutritionally balanced meals, especially among working professionals, students, and fitness-conscious individuals. The rising awareness around diet planning, calorie management, and multi-cuisine consumption has further accelerated the adoption of multi-compartment designs. Additionally, these products reduce food mixing and enhance convenience, making them highly suitable for daily use.

Insulated and thermal lunch boxes are witnessing strong growth, supported by rising demand for temperature-controlled food storage. This segment is particularly popular in regions with long commuting hours, such as Asia-Pacific, where maintaining food freshness is critical. Technological advancements in vacuum insulation and heat retention are further strengthening this category. Traditional single-compartment lunch boxes continue to hold relevance in price-sensitive markets, particularly in developing economies where affordability remains a key purchasing factor. Meanwhile, electric and self-heating lunch boxes are emerging as a premium segment, driven by urban consumers seeking convenience and functionality. These products are gaining traction in North America, Europe, and urban Asia, supported by increasing adoption of smart lifestyle products.

Material Insights

Plastic lunch boxes hold the largest market share at approximately 38% in 2025, primarily due to their low cost, lightweight nature, and mass availability. This segment continues to dominate in emerging markets where affordability and accessibility are critical drivers. However, concerns regarding health safety and environmental impact are gradually limiting long-term growth. Stainless steel lunch boxes are rapidly gaining market share and are expected to be the fastest-growing material segment, driven by their durability, non-toxic properties, and eco-friendly appeal. Increasing regulatory restrictions on plastic usage and rising consumer awareness around sustainability are accelerating this shift.

Glass lunch boxes are gaining popularity in developed markets due to their chemical-free and premium positioning, particularly among health-conscious consumers. However, their higher cost and fragility limit widespread adoption. Silicone and bamboo-based lunch boxes are emerging as niche but high-potential segments, catering to environmentally conscious consumers. These materials are benefiting from the global push toward sustainable and biodegradable alternatives, particularly in Europe and North America.

Distribution Channel Insights

Offline retail channels dominate the lunch box market with approximately 58% share in 2025, supported by strong presence across supermarkets, hypermarkets, and specialty kitchenware stores. Consumers often prefer offline channels for evaluating product quality, durability, and usability before purchase, especially in mid-range and premium segments. However, online retail channels are witnessing rapid growth and are expected to gain significant market share over the forecast period. This growth is driven by increasing internet penetration, convenience, competitive pricing, and access to a wider product range. E-commerce platforms also enable easy comparison, customer reviews, and customization options, making them highly attractive to younger consumers.

Direct-to-consumer (D2C) models are gaining traction, with brands investing in digital platforms to build stronger customer relationships, enhance brand loyalty, and improve margins. Subscription-based models and bundled offerings with meal-prep services are also emerging as innovative distribution strategies.

End-Use Insights

Household and personal use accounts for nearly 65% of the global lunch box market, driven by daily consumption needs across all demographics. The increasing preference for home-cooked meals, cost savings, and healthier eating habits continues to support this segment’s dominance. The institutional segment, including schools, offices, and healthcare facilities, represents a stable demand base. Bulk procurement by educational institutions and corporate organizations contributes significantly to consistent sales volumes.

The travel and outdoor segment is the fastest-growing, driven by rising participation in fitness activities, hiking, and recreational travel. Consumers in this segment demand durable, leak-proof, and insulated products that can withstand outdoor conditions. This segment is expected to grow at a CAGR exceeding 8%, outpacing the overall market growth. Additionally, emerging applications such as meal-prep services and fitness-focused nutrition plans are creating new demand avenues, particularly in urban markets.

| By Product Type | By Material | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global lunch box market with approximately 42% share in 2025, making it the largest and fastest-growing regional market. Countries such as China, India, and Japan are major contributors, driven by large population bases, strong cultural preference for home-cooked meals, and increasing urban workforce participation. The region’s growth is strongly supported by rapid urbanization, an expanding middle-class population, and a high number of daily commuters who rely on portable meal solutions. Cultural habits of carrying home-prepared food, especially in countries like India and Japan, continue to reinforce consistent demand. Additionally, increasing awareness of hygiene and food safety, along with the expansion of local manufacturing supported by government initiatives such as “Make in India,” is accelerating market penetration. India, in particular, is among the fastest-growing markets, with growth exceeding 9% CAGR, driven by rising disposable incomes, evolving lifestyles, and growing adoption of modern kitchenware products.

North America

North America holds around 22% market share, with the United States being the dominant contributor. The region is characterized by strong demand for premium, insulated, and eco-friendly lunch boxes, reflecting higher consumer spending capacity and lifestyle preferences. Growth in this region is primarily driven by high consumer awareness regarding sustainability and health, leading to increased adoption of BPA-free and reusable products. Additionally, the demand for convenience-oriented solutions such as electric and self-heating lunch boxes is rising among working professionals. The strong presence of e-commerce platforms and direct-to-consumer brands further enhances product accessibility and variety. Higher disposable incomes and a willingness to invest in technologically advanced and aesthetically designed products continue to support the expansion of the market in North America.

Europe

Europe accounts for approximately 18% of the global market, with Germany, the UK, and France being key markets. The region’s growth is heavily influenced by sustainability and regulatory compliance, with strict policies limiting single-use plastics and promoting eco-friendly alternatives. Consumers in Europe exhibit a strong preference for reusable, durable, and environmentally responsible products, driving demand for materials such as stainless steel, glass, and bamboo. Additionally, the increasing trend of meal prepping and healthy eating habits is contributing to higher adoption of compartmentalized lunch boxes. The market is further supported by demand for premium, aesthetically appealing designs and high-quality products. Overall, Europe represents a mature yet steadily growing market with a strong focus on sustainability-driven innovation.

Latin America

Latin America is experiencing steady growth in the lunch box market, particularly in Brazil and Mexico, supported by expanding middle-class populations and increasing awareness of healthy eating habits. The region’s growth is driven by rising urbanization, increasing workforce participation, and improving access to affordable consumer goods. Additionally, the growing influence of global lifestyle trends, including health-conscious eating and meal preparation, is positively impacting demand. Expansion of retail and e-commerce infrastructure is further improving product availability and accessibility. However, the market remains price-sensitive, with strong demand concentrated in affordable plastic and mid-range lunch box segments.

Middle East & Africa

The Middle East & Africa region represents an emerging market with strong growth potential. Key countries such as the UAE and South Africa are driving demand, supported by improving retail infrastructure, rising consumer spending, and increasing urbanization. The region is also witnessing growth due to a rising expatriate population, which influences demand for portable food storage solutions. Increasing awareness of food safety and hygiene is encouraging the adoption of reusable lunch boxes, while the expansion of modern retail formats and shopping malls is enhancing product visibility. In Gulf countries, rising demand for premium and imported products is further contributing to market growth. Although the market is still developing, improving economic conditions, lifestyle changes, and increasing disposable incomes are expected to support steady expansion over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Lunch Box Market

- Tupperware Brands Corporation

- Thermos LLC

- Newell Brands

- Tiger Corporation

- Zojirushi Corporation

- LocknLock Co. Ltd.

- Sistema Plastics

- Bentgo (Fit & Fresh Inc.)

- Milton (Hamilton Housewares)

- Borosil Ltd.

- IKEA

- Signoraware

- Stanley (PMI Worldwide)

- CamelBak Products LLC

- Hydro Flask