Low-Flow Plumbing Fixtures Market Size

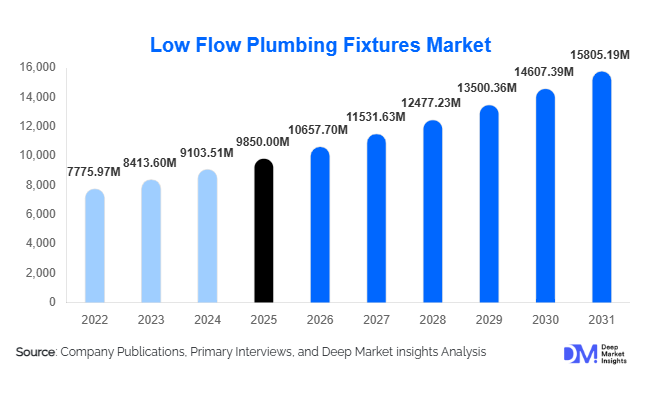

According to Deep Market Insights, the global low-flow plumbing fixtures market size was valued at USD 9,850 million in 2025 and is projected to grow from USD 10,657.70 million in 2026 to reach USD 15,805.19 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing global water scarcity concerns, stringent regulatory mandates on water efficiency, and rising adoption of sustainable building practices across residential and commercial infrastructure.

Key Market Insights

- Water conservation regulations are accelerating adoption, with governments mandating low-flow fixtures in new construction and renovation projects.

- Residential applications dominate demand, accounting for nearly 48% of the total market due to large-scale housing developments and retrofit installations.

- Asia-Pacific leads the global market, supported by rapid urbanization, infrastructure expansion, and government-led water efficiency programs.

- Sensor-based and smart fixtures are the fastest-growing segment, driven by hygiene awareness and digital water management adoption.

- Mid-range products account for the largest pricing segment, balancing affordability and performance, particularly in emerging markets.

- Direct/B2B distribution channels dominate, with project-based procurement in construction contributing the highest share.

What are the latest trends in the low-flow plumbing fixtures market?

Smart and IoT-Enabled Plumbing Systems

The market is witnessing a significant shift toward smart plumbing fixtures integrated with IoT capabilities. Smart faucets and showers equipped with sensors, timers, and usage analytics are enabling real-time water monitoring and leak detection. These systems are increasingly being deployed in commercial buildings, airports, and smart city projects. Mobile applications allow users to track consumption patterns, helping reduce water wastage and operational costs. The trend is particularly strong in developed markets where building automation systems are widely adopted.

Shift Toward Touchless and Hygienic Solutions

Post-pandemic hygiene concerns have accelerated the adoption of touchless plumbing fixtures, particularly in commercial and institutional settings. Sensor-based faucets and flush systems reduce physical contact, minimizing the risk of contamination. This trend is driving innovation in infrared and motion-sensing technologies. Hospitals, offices, and hospitality sectors are rapidly upgrading to touchless solutions, making this one of the fastest-growing segments in the market.

What are the key drivers in the low-flow plumbing fixtures market?

Regulatory Push for Water Efficiency

Governments across regions are implementing stringent water conservation regulations, such as mandatory low-flow standards in building codes. These policies are significantly boosting demand, particularly in developed markets where compliance is strictly enforced. Incentives, rebates, and certification programs are further encouraging adoption.

Rising Water Scarcity and Cost Savings

Increasing water scarcity in regions such as the Middle East, parts of Asia, and North America is driving the need for efficient water usage. Low-flow fixtures help reduce water consumption by up to 30–60%, offering substantial cost savings for households and businesses. This economic benefit is a key factor influencing purchasing decisions.

Growth in Green Building and Sustainable Construction

The expansion of green building initiatives and certifications such as LEED is boosting the integration of low-flow plumbing systems. Developers are incorporating these fixtures to meet sustainability goals and enhance property value, driving consistent demand across residential and commercial projects.

What are the restraints for the global market?

Higher Initial Costs of Advanced Fixtures

While low-flow fixtures offer long-term savings, the initial investment for advanced and smart systems remains relatively high. This can limit adoption in price-sensitive markets, particularly in developing regions where cost considerations dominate purchasing decisions.

Performance Perception Challenges

Despite technological improvements, some consumers still perceive low-flow fixtures as less effective in terms of water pressure and performance. This perception can hinder adoption, especially in markets where awareness of modern solutions is limited.

What are the key opportunities in the low-flow plumbing fixtures industry?

Expansion in Emerging Economies

Rapid urbanization and infrastructure development in countries such as India, China, and Brazil present significant growth opportunities. Government-led housing projects and smart city initiatives are mandating water-efficient solutions, creating a strong demand base for manufacturers and new entrants.

Retrofit Market in Developed Regions

A large installed base of traditional plumbing systems in North America and Europe offers substantial opportunities for retrofitting. Aging infrastructure and rising water costs are encouraging property owners to upgrade to low-flow fixtures, supported by government incentives and rebate programs.

Integration with Smart Building Ecosystems

The growing adoption of smart buildings provides opportunities for integrating low-flow fixtures with digital water management systems. Companies can leverage this trend by offering connected solutions that provide data analytics, predictive maintenance, and enhanced user experience.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9850 Million |

| Market Size in 2026 | USD 10657.70 Million |

| Market Size in 2031 | USD 15805.19 Million |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Low-flow toilets continue to dominate the global low-flow plumbing fixtures market, accounting for approximately 34% of the total market share in 2025. This dominance is primarily driven by stringent regulatory mandates across developed and developing economies, where water efficiency standards increasingly require the adoption of low-consumption sanitary systems. Toilets represent the highest water-consuming fixture in residential and commercial settings, making them a key focus area for conservation policies. The widespread adoption of dual-flush technology, which allows users to select water volume per flush, has significantly improved efficiency while maintaining performance, further accelerating demand.

Low-flow faucets and showerheads are also experiencing robust growth, particularly in residential housing and hospitality sectors, where water savings directly translate into reduced operational costs. Increasing consumer preference for aesthetically appealing, high-performance fixtures is further supporting adoption. Meanwhile, sensor-based faucets are gaining strong traction in commercial environments such as offices, malls, and airports, driven by hygiene requirements and reduced water wastage. Additionally, waterless and ultra-low flush urinals are increasingly being deployed in institutional and public infrastructure settings, where high footfall necessitates efficient water management. The continuous innovation in product design, combined with regulatory compliance and cost-saving benefits, is expected to sustain the leadership of low-flow toilets and drive balanced growth across other product categories.

Technology Insights

Sensor-based technology has emerged as one of the most dynamic segments within the market, holding approximately 22% market share in 2025 and exhibiting the fastest growth trajectory. This growth is primarily driven by heightened hygiene awareness, particularly in the post-pandemic era, and the increasing adoption of automation in commercial and institutional buildings. Touchless fixtures minimize human contact, reduce contamination risks, and optimize water usage through controlled flow mechanisms, making them highly attractive in high-traffic environments. Mechanical flow restriction technology continues to maintain a significant share due to its affordability, simplicity, and widespread applicability across residential segments. These systems are particularly prevalent in price-sensitive markets where cost considerations outweigh advanced functionality. Pressure compensation technology is another key enabler, ensuring consistent water flow regardless of supply pressure fluctuations, which is critical in regions with unstable water infrastructure.

In parallel, smart and IoT-enabled fixtures are emerging as a premium segment, gaining traction in developed markets and smart building ecosystems. These advanced systems provide real-time water usage data, leak detection, and remote control capabilities, enabling both consumers and facility managers to optimize water consumption. As digital infrastructure and smart city initiatives expand globally, the adoption of connected plumbing solutions is expected to accelerate, further reshaping the competitive landscape.

End-Use Insights

The residential segment remains the largest contributor to market demand, accounting for approximately 48% of the global market share in 2025. This leadership is driven by rapid urbanization, rising housing construction, and increasing retrofit activities aimed at replacing conventional fixtures with water-efficient alternatives. Government incentives, coupled with growing consumer awareness regarding water conservation and utility cost savings, are further reinforcing adoption in this segment. The commercial segment is the fastest-growing, supported by strong demand from offices, hospitality, healthcare, and retail sectors. High water usage in these facilities, combined with the need for operational efficiency and compliance with sustainability standards, is driving widespread deployment of low-flow and sensor-based fixtures. The hospitality industry, in particular, is adopting these solutions to enhance sustainability credentials and reduce operational costs.

Industrial and institutional applications are also gaining momentum, particularly in large-scale public infrastructure projects such as airports, metro stations, educational institutions, and government buildings. These environments require durable, high-efficiency systems capable of handling heavy usage, making low-flow fixtures a critical component of modern infrastructure planning.

Distribution Channel Insights

Direct/B2B sales channels dominate the market, contributing approximately 45% of total revenue in 2025. This dominance is largely driven by bulk procurement associated with large-scale construction projects, including residential complexes, commercial buildings, and public infrastructure developments. Manufacturers often engage directly with contractors, developers, and government bodies, enabling customized solutions and long-term supply agreements.

Retail channels continue to play a significant role, particularly in the residential retrofit and replacement market, where individual consumers purchase fixtures through home improvement stores and specialty outlets. However, the most notable shift is the rapid growth of e-commerce platforms, which are transforming purchasing behavior by offering extensive product selection, competitive pricing, and convenience. Online platforms are particularly popular among younger consumers and small contractors, and are expected to capture an increasing share of the market in the coming years.

Price Range Insights

The mid-range segment leads the market, accounting for approximately 46% of the total share, as it offers an optimal balance between affordability, durability, and performance. This segment is particularly dominant in emerging markets, where consumers seek reliable products without the premium price tag. Manufacturers are increasingly focusing on enhancing product features within this category to maintain competitiveness.

Premium products are witnessing strong growth in developed regions such as North America and Europe, driven by demand for advanced features including smart connectivity, sensor-based operation, and modern design aesthetics. These products cater to high-income consumers and commercial establishments seeking enhanced functionality and brand value. On the other hand, economy products continue to hold relevance in cost-sensitive markets, supported by large-scale government housing programs and basic infrastructure development projects.

Explore more data points, trends and opportunities Download Free Sample Report

Low Flow Plumbing Fixtures Market Segmentations

By Product Type

- Low-Flow Toilets

- Low-Flow Faucets

- Low-Flow Showerheads

- Low-Flow Urinals

- Flow Regulators & Aerators

By Technology

- Mechanical Flow Restriction

- Pressure Compensation Technology

- Sensor-Based Systems

- Smart/IoT-enabled Fixtures

By End-Use

- Residential

- Commercial

- Industrial & Institutional

By Distribution Channel

- Direct Sales (B2B)

- Retail Stores

- E-commerce Platforms

By Price Range

- Economy

- Mid-range

- Premium

Regional Insights

North America

North America accounted for approximately 28% of the global market share in 2025, with the United States contributing over 70% of regional demand. The region’s growth is primarily driven by stringent regulatory frameworks such as water efficiency standards and certification programs, which mandate the use of low-flow fixtures in both new construction and renovation projects. Additionally, the presence of a large installed base of conventional plumbing systems has created a strong retrofit market, further boosting demand. High consumer awareness, rising water costs, and the widespread adoption of smart home technologies are also key drivers supporting market expansion in this region.

Asia-Pacific

Asia-Pacific dominates the global market with approximately 32% share in 2025 and is the fastest-growing region, expanding at nearly 9.5% CAGR. The region’s growth is fueled by rapid urbanization, population growth, and large-scale infrastructure development. China leads the market due to massive residential and commercial construction activities, supported by government policies promoting water conservation. India is emerging as a high-growth market, driven by initiatives such as smart cities, affordable housing programs, and increasing awareness of water scarcity. Southeast Asian countries are also contributing to growth through expanding urban infrastructure and rising investments in sustainable development.

Europe

Europe holds approximately 24% of the global market, with Germany, the UK, and France leading regional demand. The region is characterized by stringent environmental regulations and a strong emphasis on sustainability, which are key drivers for the adoption of low-flow fixtures. The mature construction market in Europe has also led to a significant focus on retrofitting existing buildings with water-efficient systems. Additionally, high adoption of premium and smart fixtures is supported by strong consumer purchasing power and advanced infrastructure.

Middle East & Africa

The Middle East & Africa region is primarily driven by acute water scarcity, making water conservation a critical priority. Countries such as the UAE and Saudi Arabia are investing heavily in water-efficient infrastructure as part of broader sustainability and diversification strategies. Large-scale construction projects, including smart cities and tourism developments, are further supporting demand. In Africa, urbanization and gradual infrastructure development in key cities are driving adoption, although growth remains uneven due to economic constraints and limited awareness in certain regions.

Latin America

Latin America is experiencing steady growth, with Brazil and Mexico leading regional demand. The market is driven by increasing urbanization, improving construction activity, and growing awareness of water conservation. Government initiatives aimed at improving water infrastructure and reducing wastage are supporting adoption. Additionally, rising middle-class income levels and expansion of residential housing are contributing to sustained demand growth in the region.

Key Players in the Low-Flow Plumbing Fixtures Market

- Kohler Co.

- LIXIL Corporation

- TOTO Ltd.

- Masco Corporation

- Roca Sanitario S.A.

- Geberit AG

- American Standard Brands

- Villeroy & Boch

- Jaquar Group

- Hindware (HSIL Ltd.)

- Grohe AG

- Duravit AG

- Ideal Standard International

- Moen Incorporated

- Delta Faucet Company