Liquid Gel Pack Market Size

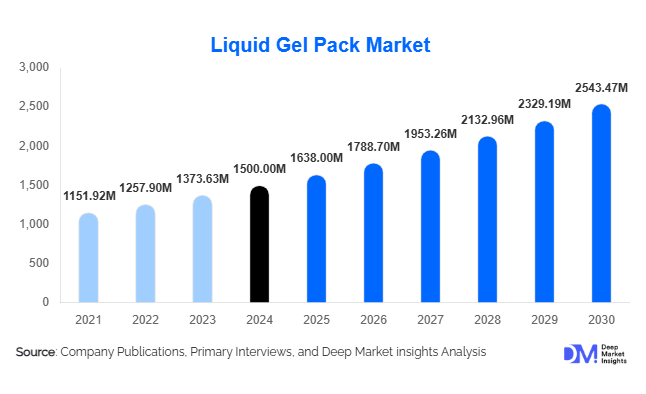

According to Deep Market Insights, the global liquid gel pack market size was valued at USD 1,500 million in 2025 and is projected to grow from USD 1,638 million in 2026 to reach USD 2,543.47 million by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The market growth is primarily driven by the rising demand for temperature-controlled transportation solutions across the pharmaceutical, food & beverage, and e-commerce sectors. Increasing consumer awareness about product safety, the surge in online grocery and meal kit deliveries, and advancements in packaging technologies are further supporting this growth trajectory.

Key Market Insights

- Pharmaceutical and biotech applications dominate demand, as strict regulations require precise temperature control during the transport of vaccines, biologics, and other sensitive medications.

- Integration of smart sensors and monitoring technologies into liquid gel packs is enhancing reliability and offering real-time temperature tracking for critical shipments.

- Eco-friendly and biodegradable gel packs are gaining traction due to growing sustainability awareness and environmental regulations.

- North America holds a significant share of the market, with the U.S. leading due to a mature healthcare infrastructure and strong pharmaceutical logistics demand.

- Asia-Pacific is the fastest-growing region, driven by expanding pharmaceutical sectors, e-commerce, and increasing adoption of temperature-sensitive product distribution in China and India.

- Technological adoption in packaging, such as RFID-enabled monitoring and improved gel formulations, is reshaping industry standards and improving operational efficiency.

Liquid Gel Pack Market latest trends

Eco-Friendly and Sustainable Solutions

With global focus on sustainability, manufacturers are increasingly producing liquid gel packs using biodegradable and recyclable materials. Companies are integrating environmental considerations into product design, appealing to both business and environmentally conscious consumers. This trend is reshaping procurement strategies in industries such as pharmaceuticals and food logistics, where eco-compliance and green packaging solutions are becoming mandatory. Many players are also exploring reusable gel packs to reduce waste while maintaining cost-effectiveness.

Smart Technology Integration

Liquid gel packs are now being enhanced with smart sensors and IoT-enabled monitoring systems that provide real-time temperature tracking during shipment. This is particularly critical in pharmaceutical logistics, where minor deviations can compromise product safety. The adoption of digital monitoring systems not only ensures compliance with regulations but also builds confidence among end-users regarding product quality. This trend is expected to grow as data-driven supply chains expand globally.

Liquid Gel Pack Market key drivers

Growth in E-Commerce and Cold Chain Logistics

The rapid expansion of e-commerce, particularly for perishable foods and pharmaceuticals, is driving the demand for liquid gel packs. Consumers increasingly rely on home delivery of temperature-sensitive goods, which necessitates reliable cold chain solutions. The growing popularity of meal kits, online grocery platforms, and pharmaceutical delivery services further boosts the need for advanced temperature-controlled packaging.

Regulatory Compliance in Pharmaceuticals

Stringent regulations for transporting temperature-sensitive medications are creating consistent demand for liquid gel packs. Compliance with guidelines set by authorities such as the FDA, EMA, and WHO requires robust cold chain packaging, positioning gel packs as a standard solution for pharmaceutical logistics globally.

Material and Packaging Innovations

Advances in gel formulations and durable outer casing materials such as PET have improved thermal stability and product lifespan. These innovations have enhanced the efficiency of liquid gel packs, making them more cost-effective and reliable for long-distance shipments. Improved design and performance characteristics have further encouraged adoption across multiple industries.

Liquid Gel Pack Market restraints

High Manufacturing Costs

Producing high-quality liquid gel packs requires specialized materials and processes, which increases costs. Small and medium-sized enterprises face challenges in competing with established manufacturers offering technologically advanced solutions at scale. Cost sensitivity among some end-users can limit adoption, especially in emerging markets.

Competition from Alternative Solutions

Dry ice, phase change materials, and other cold chain alternatives provide competition to liquid gel packs. Industries may choose alternative methods depending on shipment duration, temperature requirements, and cost considerations. This competitive pressure can restrict market penetration in certain segments.

Liquid Gel Pack Market key opportunities

Expansion in Emerging Markets

Asia-Pacific and Latin America are emerging as high-growth regions for liquid gel packs. Rapid urbanization, expanding pharmaceutical industries, and increasing e-commerce penetration provide a strong opportunity for market players. Companies entering these markets can capitalize on increasing domestic demand for temperature-controlled packaging in healthcare, food, and logistics sectors.

Integration of Smart Packaging

Embedding sensors, RFID, and IoT technology into gel packs can provide real-time temperature monitoring and data analytics. This capability is especially valuable for pharmaceutical shipments and high-value perishable goods, enhancing reliability and customer trust. Adoption of smart packaging also aligns with the trend of digital transformation in logistics.

Focus on Sustainability

Growing awareness of environmental impact and stricter regulatory requirements are encouraging manufacturers to develop biodegradable, recyclable, and reusable gel packs. Companies that lead in eco-friendly innovations can differentiate themselves in a competitive market while supporting global sustainability initiatives.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1500 Million |

| Market Size in 2026 | USD 1638 Million |

| Market Size in 2031 | USD 2543.47 Million |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Cold gel packs dominate the market, representing approximately 60% of the 2025 market share. Their widespread use in medical, pharmaceutical, and food applications is due to their ability to maintain low temperatures reliably. Reusable cold packs are gaining traction as cost-effective and environmentally friendly solutions, while hot gel packs serve niche applications in therapeutic and medical segments.

Application Insights

The pharmaceutical segment is the largest application, contributing around 40% of the 2025 market. Strict regulatory requirements for temperature-controlled drug transport make gel packs essential. The food and beverage industry is the second-largest application, where gel packs maintain freshness during distribution. Logistics and e-commerce applications are emerging rapidly due to online grocery and meal kit delivery services, creating new growth opportunities.

End-Use Insights

Pharmaceutical companies are the largest end-users due to strict cold chain compliance requirements, followed by the food & beverage industry. The fastest-growing end-use segments include e-commerce grocery delivery and biotechnology shipments, which are increasingly reliant on temperature-sensitive packaging solutions. Export-driven demand is significant in regions like North America and Europe, where pharmaceutical exports require reliable cold chain systems.

Explore more data points, trends and opportunities Download Free Sample Report

Liquid Gel Pack Market Segmentations

By Product Type

- Cold Gel Packs

- Hot Gel Packs

- Reusable Gel Packs

- Single-Use Gel Packs

By Application

- Pharmaceuticals & Biologics

- Food & Beverage

- Logistics & E-commerce

- Therapeutic & Medical Applications

By Material Type

- Polyethylene (PE)

- Polyethylene Terephthalate (PET)

- Non-toxic Gel Formulations (e.g., Sodium Polyacrylate)

By Distribution Channel

- Direct Manufacturer Sales

- Online Retail & E-commerce

- Wholesale & Distributors

- Specialty Packaging Retailers

Regional Insights

North America

North America is a dominant market, with the U.S. accounting for over 35% of the global liquid gel pack demand in 2025. Growth is fueled by a mature pharmaceutical sector, advanced logistics infrastructure, and high adoption of e-commerce and temperature-sensitive packaging solutions. Canada also contributes significantly, particularly in pharmaceutical cold chain logistics.

Europe

Germany and the U.K. lead the European market, representing approximately 25% of the global share in 2025. Strict regulatory compliance and well-established pharmaceutical supply chains drive demand. Europe is also witnessing the rapid adoption of eco-friendly and smart packaging solutions, further boosting growth.

Asia-Pacific

China and India are the fastest-growing markets, driven by expanding healthcare infrastructure, increased e-commerce penetration, and rising consumer demand for perishable goods. Adoption of temperature-sensitive packaging in pharmaceuticals and logistics is accelerating market growth, with high CAGR rates projected through 2031.

Latin America

Brazil and Mexico are emerging markets for liquid gel packs due to growing pharmaceutical industries, e-commerce expansion, and increasing cold chain awareness. Demand remains moderate but is expected to grow steadily as infrastructure improves.

Middle East & Africa

The UAE and South Africa are key markets, supported by increasing healthcare investments and logistics infrastructure development. Demand is driven by pharmaceutical distribution and export activities, with the region seeing gradual growth in the adoption of temperature-controlled packaging solutions.

Key Players in the Liquid Gel Pack Market

- Cold Chain Technologies

- Pelican BioThermal

- Sonoco Products Company

- Va-Q-Tec AG

- Sealed Air Corporation

- Pregis

- Storopack

- Thermo King

- Cryopak

- Javapack

- Signode Industrial Group

- Paragon Innovations

- Temperature Control Systems

- BlueSky Pack

- Nordic Cold Chain Solutions