Lip and Face Primer Market Size

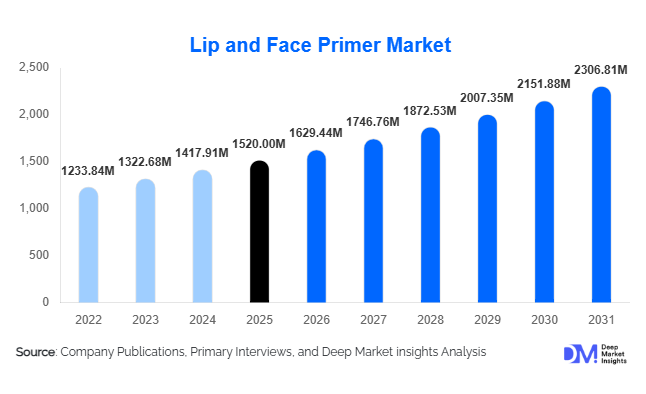

According to Deep Market Insights, the global lip and face primer market size was valued at USD 1,520 million in 2025 and is projected to grow from USD 1,629.44 million in 2026 to reach USD 2,306.81 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). Market growth is primarily driven by rising consumer demand for long-lasting makeup, increasing convergence between skincare and cosmetics, and the rapid expansion of digital beauty retail channels. Primers have evolved from niche professional products into mainstream essentials, particularly among millennials and Gen Z consumers seeking pore-blurring, oil-control, hydrating, and color-correcting solutions.

Key Market Insights

- Face primers dominate the category, accounting for nearly 78% of global revenue in 2025 due to multifunctional benefits and higher average selling prices.

- Masstige products lead pricing tiers, balancing affordability with premium positioning and contributing approximately 38% of market share.

- North America holds the largest regional share (32%), led by strong per capita cosmetics spending in the United States.

- Asia-Pacific is the fastest-growing region, expanding at over 8.5% CAGR, driven by rising middle-class incomes and social media influence.

- E-commerce accounts for around 34% of total sales, reflecting the rapid digitalization of beauty purchases.

- Clean, vegan, and dermatologically tested formulations are reshaping product innovation strategies across leading brands.

What are the latest trends in the lip and face primer market?

Skinification of Makeup Products

One of the most prominent trends is the integration of skincare ingredients into primers. Brands are launching formulations enriched with hyaluronic acid, niacinamide, SPF, peptides, and antioxidants to provide hydration and protective benefits alongside makeup longevity. This “skinification” approach is appealing to consumers seeking multifunctional products that simplify daily routines. As a result, hybrid primer-serum products are gaining shelf space across premium and masstige segments. Dermatologically tested and non-comedogenic claims are increasingly highlighted, enhancing trust and driving repeat purchases.

Clean Beauty and Vegan Formulations

Consumers are showing growing preference for silicone-free, paraben-free, cruelty-free, and vegan-certified primers. Regulatory pressures in Europe and increasing awareness in North America are accelerating reformulation efforts. Indie brands focusing on botanical extracts and sustainable packaging are capturing niche market share, prompting larger players to expand clean-label portfolios. Sustainable sourcing, recyclable tubes, and refillable packaging are emerging as differentiators, particularly in premium and luxury segments.

What are the key drivers in the lip and face primer market?

Rising Demand for Long-Lasting Makeup

Modern consumers seek makeup products that offer extended wear in diverse climates and long work schedules. Primers enhance foundation and lipstick durability by minimizing oil breakthrough and smoothing texture. This functional benefit is driving widespread adoption beyond professional makeup artists into everyday routines, particularly among urban working populations.

Growth of Digital Beauty Retail

E-commerce platforms, brand-owned websites, and social commerce integrations have significantly expanded market accessibility. Influencer-led tutorials and product demonstrations have normalized primer usage, driving conversion rates. AI-based personalization tools and virtual try-ons are further enhancing online purchase confidence, especially among younger consumers.

What are the restraints for the global market?

Price Sensitivity in Emerging Economies

Premium and luxury primers often carry high price tags, limiting penetration in cost-sensitive markets. Although masstige products are bridging the gap, affordability remains a barrier in parts of Asia, Africa, and Latin America.

Volatility in Raw Material Prices

Key ingredients such as silicones, specialty polymers, and cosmetic-grade emollients are subject to petrochemical price fluctuations. This impacts manufacturing costs and compresses margins, particularly for mid-sized brands lacking scale advantages.

What are the key opportunities in the lip and face primer industry?

Expansion into Emerging Markets

Rapid urbanization and increasing disposable incomes in India, Brazil, Indonesia, and Saudi Arabia are expanding the cosmetics consumer base. Localization strategies, climate-adapted formulations, and inclusive shade ranges can unlock significant incremental revenue.

D2C and Subscription-Based Beauty Models

Direct-to-consumer brands are leveraging data analytics, influencer collaborations, and subscription boxes to build loyal communities. Personalized primer recommendations based on skin type and lifestyle preferences present scalable growth opportunities for both startups and established players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1520 Million |

| Market Size in 2026 | USD 1629.44 Million |

| Market Size in 2031 | USD 2306.81 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Face primers dominate the global lip and face primer market, accounting for approximately 78% of total revenue in 2025, primarily due to their multifunctional benefits and integration into everyday makeup routines. The leading driver for this segment is the growing consumer demand for long-lasting, high-performance makeup solutions that address multiple skin concerns simultaneously. Face primers offer mattifying, pore-minimizing, hydrating, illuminating, and color-correcting properties, making them versatile across skin types and climates. Silicone-based primers remain highly preferred for their superior pore-blurring and smooth finish, particularly in premium and professional segments. Meanwhile, water-based and gel-based primers are gaining momentum among younger consumers who prefer lightweight, breathable, and non-comedogenic formulations aligned with the clean beauty movement.

Lip primers, while accounting for a smaller share of the overall market, are experiencing steady growth driven by increasing global lipstick consumption and the popularity of matte and long-wear lip products. The rising demand for smudge-proof, feather-resistant lip color, particularly in humid and high-temperature regions, continues to support innovation within this segment. Stick and pencil formats are popular for precision application, while liquid and cream variants are growing in the masstige and premium categories.

Ingredient Positioning Insights

Conventional/synthetic formulations hold approximately 60% of the global market share in 2025, supported by their cost efficiency, formulation stability, and established consumer trust. The primary driver of this leading segment is performance reliability, particularly in silicone-enhanced formulations that deliver immediate smoothing and oil-control benefits. Mass and masstige brands continue to rely on conventional bases to maintain competitive pricing and scalable production.

However, natural, organic, and vegan-certified primers are expanding at a faster CAGR compared to conventional products. Growth in this segment is fueled by heightened consumer awareness regarding ingredient transparency, environmental sustainability, and skin sensitivity concerns. Dermatologically tested and hypoallergenic primers are increasingly favored among consumers with reactive or acne-prone skin, particularly in North America and Europe where regulatory scrutiny is strong. Premium brands are investing in botanical extracts, mineral-based blurring agents, and biodegradable packaging to strengthen differentiation and justify higher price points.

Distribution Channel Insights

E-commerce leads the distribution landscape, accounting for approximately 34% of global sales in 2025, making it the fastest-growing channel in the market. The key growth driver for this segment is the rapid digitalization of beauty retail, supported by influencer marketing, social commerce integrations, and AI-powered personalization tools. Consumers increasingly rely on online reviews, tutorials, and virtual try-on technologies before making purchase decisions. Direct-to-consumer (D2C) strategies adopted by both global conglomerates and indie brands have significantly enhanced profit margins and brand loyalty.

Specialty beauty retailers remain critical for premium product sales, offering experiential shopping environments and personalized consultations. Supermarkets and hypermarkets contribute to volume-driven mass-market sales, particularly in emerging economies where price sensitivity remains high. Pharmacies and drugstores play an important role in dermatologically positioned and sensitive-skin primer sales.

End-Use Insights

Individual consumers account for over 85% of total demand in 2025, driven by widespread retail adoption and growing daily usage of makeup products. The leading driver for this segment is the normalization of primer usage within standard beauty routines, influenced by social media tutorials and professional makeup trends. Professional salons and makeup studios represent a smaller but faster-growing segment, expanding at approximately 8–9% CAGR. Growth is supported by increasing bridal events, fashion shows, influencer-driven content production, and entertainment industry requirements. Film and media industries in the U.S., South Korea, and India generate consistent bulk procurement demand, particularly for high-performance and HD-compatible primers. Export-driven manufacturing hubs such as South Korea, France, and the United States continue to supply global markets, strengthening cross-border trade flows.

Explore more data points, trends and opportunities Download Free Sample Report

Lip and Face Primer Market Segmentations

By Product Type

- Face Primer

- Lip Primer

By Ingredient Positioning

- Conventional/Synthetic Formulation

- Natural & Organic Formulation

- Vegan/Cruelty-Free Certified

- Dermatologically Tested/Clinical-Grade

By Price Tier

- Mass Market

- Masstige (Premium-Mass Hybrid)

- Premium

- Luxury/Prestige

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Beauty Retailers

- Pharmacies & Drugstores

- E-Commerce (Brand Websites & Marketplaces)

- Direct Selling/Independent Consultants

By End User

- Individual Consumers (Retail)

- Professional Salons & Makeup Studios

- Film, Television & Fashion Industry

Regional Insights

North America

North America holds approximately 32% of the global market share in 2025, with the United States accounting for nearly 26%. Regional growth is primarily driven by high per capita beauty spending, strong brand penetration, and early adoption of premium and clean beauty products. The U.S. market benefits from advanced e-commerce infrastructure, influencer-driven product launches, and robust R&D investments by leading cosmetic companies. Rising demand for vegan and cruelty-free formulations further accelerates innovation. Canada demonstrates steady growth supported by expanding clean-label product adoption and increasing demand for dermatologically tested cosmetics.

Europe

Europe accounts for approximately 27% of global revenue, led by France, Germany, Italy, and the United Kingdom. Regional growth is driven by strict cosmetic regulations that encourage high-quality and safe formulations, enhancing consumer trust. Europe’s well-established beauty manufacturing ecosystem supports continuous product innovation and export expansion. Premium and luxury segments perform strongly in Western Europe, while Eastern Europe is witnessing increased masstige adoption due to rising disposable incomes. Sustainability regulations and eco-label certifications are major growth drivers within the region.

Asia-Pacific

Asia-Pacific represents nearly 30% of the global market and is the fastest-growing region, expanding at over 8.5% CAGR. China (approximately 12% share), Japan, South Korea, and India are the primary contributors. Growth drivers include rising middle-class incomes, strong influence of K-beauty and J-beauty trends, rapid urbanization, and social media-driven beauty awareness. South Korea remains a key innovation hub for hybrid skincare-makeup primers, while India’s expanding retail infrastructure and increasing female workforce participation are accelerating masstige product adoption. Growing cross-border e-commerce in China further strengthens regional momentum.

Latin America

Latin America contributes around 5% of global revenue, with Brazil and Mexico as leading markets. Regional growth is supported by increasing urbanization, expanding organized retail channels, and rising beauty consciousness among younger consumers. Social media influence and growing demand for long-wear makeup in tropical climates drive primer adoption. Economic stabilization and expanding middle-income populations are expected to further support growth in the coming years.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of the global market, led by Saudi Arabia and the UAE. Growth drivers include rising disposable incomes, strong luxury retail presence, and increasing female workforce participation. High demand for long-lasting makeup suitable for hot and humid climates significantly supports primer adoption. In Africa, improving retail penetration and growing urban populations are gradually expanding the addressable consumer base. Tourism-driven retail sales in the UAE also contribute to premium product demand within the region.

Key Players in the Lip and Face Primer Market

- L'Oréal Group

- Estée Lauder Companies Inc.

- Shiseido Company, Limited

- Unilever PLC

- Coty Inc.

- Procter & Gamble Co.

- Amorepacific Corporation

- e.l.f. Beauty Inc.

- Huda Beauty

- Revlon Inc.

- Chanel SA

- Dior (LVMH)

- KOSÉ Corporation

- Clarins Group

- Elizabeth Arden Inc.