LEGO Blocks Market Size

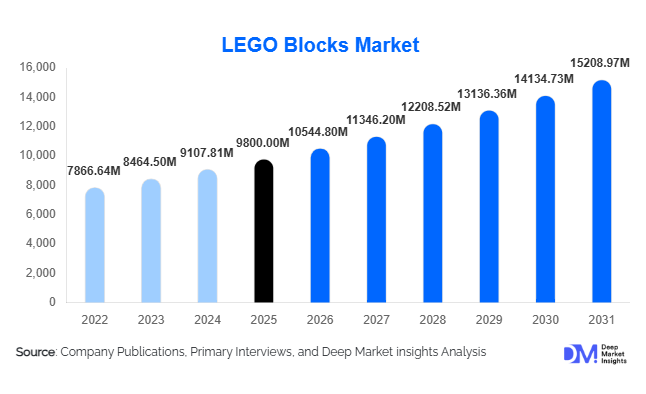

According to Deep Market Insights, the global LEGO blocks market size was valued at USD 9,800 million in 2025 and is projected to grow from USD 10,544.80 million in 2026 to reach USD 15,208.97 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The LEGO blocks market growth is primarily driven by increasing demand for educational and STEM-based toys, expansion of licensed themed sets, and rising engagement from adult consumers seeking creative and collectible building experiences.

Key Market Insights

- The LEGO blocks market is expanding beyond children to adult consumers, with premium and collector sets gaining strong traction globally.

- Educational and STEM-integrated building kits are driving institutional demand, particularly across schools and learning centers.

- North America dominates the global market, supported by high disposable income and strong brand loyalty.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class populations in China and India.

- Sustainability initiatives, including bio-based plastics, are reshaping product development and manufacturing strategies.

- E-commerce and digital engagement platforms are significantly enhancing product accessibility and consumer interaction.

What are the latest trends in the LEGO blocks market?

Expansion of Adult Consumer Segment (AFOL)

The adult fan of LEGO (AFOL) segment is emerging as a major growth driver, with increasing demand for complex, premium, and collectible sets. Adults are purchasing LEGO products for stress relief, creative expression, and as display collectibles. High-value sets priced above USD 300 are witnessing strong demand, particularly in North America and Europe. Manufacturers are responding by launching architecturally inspired models, pop-culture collaborations, and limited-edition releases, which not only increase average selling prices but also improve brand engagement and customer loyalty.

Integration of Digital and Interactive Experiences

Technological advancements are transforming the traditional building experience into an interactive ecosystem. Mobile applications, augmented reality (AR), and app-connected kits are enhancing user engagement by enabling virtual building instructions, real-time interaction, and gamification. These innovations are particularly appealing to tech-savvy younger consumers, bridging the gap between physical and digital play. Additionally, online communities and social sharing platforms are fostering a global ecosystem of LEGO enthusiasts, further strengthening brand engagement and repeat purchases.

What are the key drivers in the LEGO blocks market?

Rising Demand for Educational and STEM Toys

Parents and educators are increasingly prioritizing toys that combine entertainment with learning outcomes. LEGO blocks promote cognitive development, problem-solving, and spatial skills, making them highly suitable for STEM education. Governments and educational institutions are incorporating LEGO-based kits into curricula, significantly boosting demand in the institutional segment. This trend is particularly strong in Europe and Asia-Pacific, where education-driven toy adoption is accelerating.

Growth of Licensed and Themed Product Lines

Collaborations with global entertainment franchises are driving strong demand for themed LEGO sets. These products appeal to a wide demographic range, including children, teenagers, and adults. Licensed themes often command premium pricing and encourage repeat purchases, contributing significantly to overall revenue growth. The combination of storytelling and construction enhances consumer engagement and extends product lifecycle value.

What are the restraints for the global market?

High Product Pricing in Emerging Markets

The premium pricing of LEGO products poses a challenge in price-sensitive markets such as India, Brazil, and parts of Southeast Asia. While demand is growing, affordability constraints limit widespread adoption among middle-income consumers. Companies must address this challenge through localized pricing strategies and cost-effective product offerings to expand market penetration.

Environmental Concerns Related to Plastic Usage

The reliance on plastic materials, particularly ABS plastic, has raised environmental concerns among consumers and regulators. Increasing scrutiny around sustainability and waste management is pressuring manufacturers to adopt eco-friendly alternatives. Transitioning to bio-based and recycled materials requires significant investment and may impact production costs and profit margins in the short term.

What are the key opportunities in the LEGO blocks industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities due to rising disposable incomes, urbanization, and increasing awareness of educational toys. Localization of product offerings, pricing strategies, and distribution networks can enable companies to capture untapped demand in these regions. The rapid expansion of e-commerce platforms further enhances accessibility, making these markets highly attractive for new entrants and existing players.

Adoption of Sustainable Materials

The shift toward eco-friendly materials represents a key opportunity for differentiation and long-term growth. Manufacturers investing in bio-based plastics and recycled materials can align with evolving consumer preferences and regulatory requirements. Sustainability-focused innovation not only enhances brand perception but also enables companies to command premium pricing in environmentally conscious markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9800 Million |

| Market Size in 2026 | USD 10544.80 Million |

| Market Size in 2031 | USD 15208.97 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Themed LEGO sets dominate the global market, accounting for approximately 45% of total revenue in 2025, making them the leading product category. This dominance is primarily driven by strong consumer engagement through licensed franchises and proprietary themes that combine storytelling with creative construction. The integration of popular culture, movies, and entertainment properties enhances repeat purchases and brand loyalty, particularly among children and adult collectors. Additionally, continuous product innovation, frequent new launches, and seasonal releases sustain demand momentum in this segment.

Educational and STEM-focused sets represent the fastest-growing segment, supported by increasing adoption in schools, coding programs, and hands-on learning environments. Governments and institutions are actively promoting STEM education, which directly boosts demand for programmable and robotics-based LEGO kits. Meanwhile, collectible and limited-edition sets are gaining significant traction among adult consumers, contributing to higher average selling prices and profit margins. This segment benefits from the growing “adult fan of LEGO” (AFOL) community, where consumers seek premium, display-worthy models and exclusive designs.

Application Insights

Recreational applications continue to dominate the LEGO blocks market, accounting for nearly 60% of total demand, driven by the product’s core positioning as an entertainment and creativity-enhancing toy. The segment’s leadership is supported by strong global brand recognition, continuous innovation in themed sets, and high engagement among children and families. Seasonal demand, particularly during holidays and gifting occasions, further reinforces the dominance of recreational usage.

Educational applications are the fastest-growing segment, fueled by increasing integration into STEM curricula, coding education, and experiential learning programs. Schools and educational institutions are adopting LEGO-based learning systems to enhance problem-solving and analytical skills. Professional applications, including engineering prototyping, architecture modeling, and design simulations, are emerging as niche but high-value segments. Additionally, therapeutic applications—particularly in cognitive development, autism therapy, and mental wellness—are gaining traction, highlighting the expanding functional scope of LEGO products beyond traditional play.

Distribution Channel Insights

Offline retail channels remain dominant, capturing approximately 55% of the market share in 2025, led by toy stores, supermarkets, and specialty outlets. The leadership of this segment is driven by the tactile nature of LEGO products, where consumers prefer in-store experiences, product demonstrations, and immediate purchases. Strong retail partnerships, exclusive in-store launches, and brand-owned stores further strengthen offline dominance.

However, online channels are the fastest-growing distribution segment, supported by increasing digital adoption, convenience, and access to a wider product assortment. E-commerce platforms and direct-to-consumer brand websites are enabling global reach, particularly in emerging markets where physical retail infrastructure may be limited. Online channels also benefit from competitive pricing, bundled offers, and customer reviews, which influence purchase decisions. The shift toward omnichannel strategies, combining physical and digital retail, is becoming a key trend in market expansion.

Age Group Insights

The 7–12 years age group holds the largest share of the LEGO blocks market, accounting for around 30% of total revenue. This segment leads due to its strong engagement in creative building activities, cognitive development needs, and compatibility with educational applications. Products designed for this age group strike a balance between complexity and playability, making them highly appealing to both children and parents.

The adult segment (18+) is the fastest-growing category, driven by increasing demand for premium, complex, and collectible sets. Adults are engaging with LEGO as a hobby, stress-relief activity, and creative outlet, significantly expanding the market beyond traditional demographics. Younger age groups, including toddlers and preschoolers, contribute a steady demand through entry-level products focused on safety, basic motor skills, and early learning. This diversified age segmentation ensures consistent demand across lifecycle stages.

End-User Insights

Individual consumers dominate the LEGO blocks market, accounting for approximately 70% of total demand, driven by strong household consumption and gifting trends. The segment’s leadership is supported by brand loyalty, wide product availability, and continuous innovation catering to diverse age groups and preferences.

Educational institutions represent the fastest-growing end-user segment, driven by increasing adoption of LEGO-based learning tools in STEM education and experiential teaching methods. Governments and private institutions are investing in hands-on learning solutions, boosting demand for educational kits. Corporate and professional users, although a smaller segment, are gaining traction in applications such as team-building exercises, design thinking workshops, and engineering prototyping. This diversification of end-use applications is contributing to sustained market growth.

Explore more data points, trends and opportunities Download Free Sample Report

LEGO Blocks Market Segmentations

By Product Type

- Standard LEGO Sets

- Themed LEGO Sets

- Educational & STEM Sets

- Robotics & Programmable Kits

- Collectible & Limited-Edition Sets

- Bulk Brick Packs & Accessories

By Application

- Recreational/Entertainment

- Educational/Institutional

- Professional/Engineering Models

- Therapeutic & Cognitive Development

By Distribution Channel

- Offline Retail

- Online Retail

By Age Group

- Toddlers (1–3 years)

- Preschool (4–6 years)

- Children (7–12 years)

- Teenagers (13–17 years)

- Adults (18+ years)

By End-User

- Individual Consumers

- Educational Institutions

- Corporate/Professional Users

Regional Insights

North America

North America leads the LEGO blocks market, accounting for approximately 35% of global revenue in 2025, with the United States representing the largest contributor. The region’s dominance is driven by high disposable incomes, strong brand penetration, and a well-established toy retail ecosystem. A key growth driver in North America is the expanding adult consumer segment, with increasing demand for premium and collectible sets. Additionally, strong integration of LEGO products into educational curricula and STEM programs supports institutional demand. The presence of advanced e-commerce infrastructure and omnichannel retail strategies further enhances accessibility and sales growth in the region.

Europe

Europe holds around 30% of the global market share, with major contributions from Germany, the United Kingdom, and France. The region’s growth is driven by strong consumer preference for educational and sustainable toys. Government emphasis on early childhood education and STEM learning has significantly boosted demand for LEGO educational kits. Additionally, Europe is at the forefront of sustainability initiatives, encouraging the adoption of eco-friendly materials and production processes. High brand loyalty, coupled with a mature retail network and strong purchasing power, continues to support steady market growth across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR of over 9%, with China and India as key growth engines. China accounts for nearly 40% of regional demand, driven by rapid urbanization, rising middle-class income, and strong demand for educational toys. India is emerging as a high-growth market due to increasing awareness of STEM education, expanding e-commerce penetration, and a large young population. The region’s growth is further supported by government initiatives promoting education, increasing digital adoption, and the localization of product offerings to suit regional preferences. Expanding retail infrastructure and online marketplaces are also enhancing product accessibility.

Latin America

Latin America accounts for approximately 5–7% of the global LEGO blocks market, with Brazil and Mexico leading demand. Regional growth is driven by urbanization, improving retail infrastructure, and rising consumer awareness of educational toys. Increasing internet penetration and the expansion of e-commerce platforms are also supporting market accessibility. However, price sensitivity remains a key challenge, requiring companies to adopt localized pricing strategies and introduce affordable product variants to expand their consumer base.

Middle East & Africa

The Middle East & Africa region holds around 3–5% of the market, with key demand centers in the UAE and South Africa. Growth in this region is driven by rising disposable incomes, expansion of premium retail outlets, and increasing demand for high-quality branded toys. The Middle East, in particular, benefits from a strong luxury retail culture and high consumer spending on premium products. Additionally, growing tourism and the development of large-scale shopping destinations are boosting sales. In Africa, gradual economic development and increasing awareness of educational toys are supporting long-term growth potential.