LED Lenser Market Size

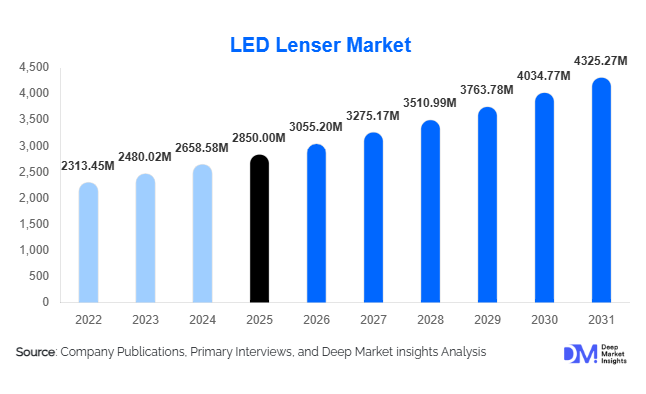

According to Deep Market Insights, the global LED Lenser market size was valued at USD 2,850 million in 2025 and is projected to grow from USD 3,055.20 million in 2026 to reach USD 4,325.27 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for high-performance portable lighting solutions across outdoor recreation, industrial safety, and emergency response applications. The transition toward energy-efficient LED-based lighting, coupled with advancements in rechargeable battery technology and smart lighting features, is further accelerating market expansion. Additionally, rising participation in adventure tourism and stringent workplace safety regulations across industries such as mining, construction, and oil & gas are reinforcing the demand for durable and high-lumen lighting tools globally.

Key Market Insights

- Rechargeable LED lighting devices are rapidly gaining dominance, driven by sustainability concerns and cost efficiency over time.

- Industrial and professional applications account for a significant share, supported by safety regulations and operational requirements.

- North America leads the global market, with strong demand from the outdoor recreation and industrial sectors.

- Asia-Pacific is the fastest-growing region, fueled by industrialization and rising consumer spending.

- Medium-lumen (300–1000 lumens) devices dominate, offering a balance between performance and affordability.

- Technological advancements, including smart connectivity and improved battery efficiency, are reshaping product innovation.

What are the latest trends in the LED Lenser market?

Shift Toward Smart and Connected Lighting

The LED Lenser market is witnessing a strong shift toward smart and connected lighting solutions. Manufacturers are integrating IoT-enabled features such as Bluetooth connectivity, mobile app control, and adaptive brightness settings. These innovations allow users to monitor battery performance, customize light intensity, and enhance operational efficiency in real time. Smart lighting is particularly gaining traction in industrial and emergency applications, where precision and reliability are critical. Additionally, integration with broader digital ecosystems is opening new opportunities for connected workplaces, making smart LED lighting a key differentiator among premium products.

Growing Preference for Lightweight and Rechargeable Devices

Consumers and professionals alike are increasingly favoring lightweight, portable, and rechargeable LED lighting devices. Lithium-ion battery technology has significantly improved energy density and charging efficiency, enabling longer usage durations and reduced maintenance costs. This trend is especially prominent in outdoor recreation and industrial sectors, where mobility and convenience are essential. Manufacturers are focusing on ergonomic designs, compact form factors, and multi-functional features to cater to evolving user preferences, further driving the adoption of rechargeable LED Lenser products globally.

What are the key drivers in the LED Lenser market?

Rising Demand for Industrial Safety and Compliance

Industries such as construction, mining, and oil & gas are increasingly adopting high-performance LED lighting solutions to meet stringent safety regulations. Proper illumination is critical for reducing workplace accidents and ensuring operational efficiency, making LED Lenser products indispensable in hazardous environments. Regulatory mandates and safety standards are further driving adoption across industrial applications.

Increasing Popularity of Outdoor and Adventure Activities

The growing global interest in outdoor activities such as camping, hiking, and trekking is significantly boosting demand for portable lighting solutions. Consumers are investing in durable, high-lumen devices that can withstand harsh environmental conditions. This trend is particularly strong in developed markets, where outdoor recreation is a major lifestyle component.

What are the restraints for the global market?

High Initial Product Costs

Advanced LED Lenser products with high lumen output and smart features often come at a premium price. This can limit adoption in price-sensitive markets, particularly in developing regions where cost remains a key purchasing factor.

Intense Competition from Low-Cost Manufacturers

The market faces strong competition from low-cost manufacturers, particularly in Asia, offering budget alternatives. This puts pressure on established brands to maintain competitive pricing while preserving product quality and innovation.

What are the key opportunities in the LED Lenser industry?

Expansion in Emerging Markets

Rapid industrialization and urbanization in emerging economies such as India, Brazil, and Southeast Asian countries present significant growth opportunities. Increasing infrastructure development and rising disposable incomes are driving demand for both industrial and consumer lighting solutions. Companies that establish localized production and distribution networks can capitalize on these expanding markets.

Integration of Smart Technologies

The adoption of smart lighting technologies offers a major opportunity for market players. Features such as IoT connectivity, remote monitoring, and energy optimization are creating new value propositions, particularly for industrial and professional users. This trend is expected to drive premium product adoption and increase profit margins.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2850 Million |

| Market Size in 2026 | USD 3055.20 Million |

| Market Size in 2031 | USD 4325.27 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Handheld flashlights dominate the LED Lenser market, accounting for approximately 38% of the global market share in 2025. Their sustained leadership is driven by their versatility and adaptability across multiple applications, including residential, industrial, and tactical operations. High-lumen outputs, ergonomic designs, and long-lasting batteries have made handheld flashlights the preferred choice for both professional and consumer use. Headlamps are gaining strong traction, particularly in outdoor recreation and industrial sectors, due to their hands-free functionality, adjustable beam focus, and lightweight design, which enhance usability in rugged and hazardous environments. Lanterns and area lights are primarily utilized in camping, emergency scenarios, and temporary lighting applications, while specialized lighting tools such as inspection lights and work lights are witnessing consistent demand in industrial maintenance, construction, and repair activities, where precision and durability are critical. Overall, product innovation, energy efficiency, and ergonomic design remain the key drivers for growth within each product segment.

Application Insights

Industrial and professional applications lead the market with around 34% share in 2025. This dominance is fueled by stringent safety regulations, operational continuity requirements, and workplace compliance mandates across sectors such as mining, construction, oil & gas, and manufacturing. Portable LED lighting enhances worker safety in low-visibility or high-risk environments and reduces accident-related downtime, making it indispensable. Outdoor and recreational applications are rapidly expanding due to the surge in adventure tourism, hiking, camping, and recreational sports, which are driving demand for compact, high-lumen, and rechargeable devices. Emergency and rescue services also represent a critical application segment, where performance reliability and battery endurance are paramount. Military and law enforcement applications require tactical, high-durability, and multi-functional lighting solutions. Across applications, the combination of robust design, energy efficiency, and technological enhancements such as adjustable brightness and smart connectivity is accelerating adoption globally.

Distribution Channel Insights

Offline retail channels dominate the market, accounting for approximately 57% of total sales in 2025. Consumers frequently prefer inspecting high-value lighting devices in person to evaluate build quality, brightness, and ergonomic design before purchase. Specialty outdoor stores, industrial suppliers, and electronics chains serve as critical touchpoints for customer engagement. However, online retail is growing rapidly, driven by convenience, competitive pricing, extensive product variety, and D2C platforms offering direct access to premium and specialized models. E-commerce enables real-time comparison, home delivery, and bundled offers, which are particularly appealing for younger and tech-savvy consumers. The rising penetration of mobile apps, online reviews, and social media marketing further strengthens the online distribution channel, making it a vital avenue for market expansion.

End-User Insights

Individual consumers represent the largest end-user segment, contributing around 46% of the market share in 2025. This growth is driven by increasing adoption of portable lighting for personal use, outdoor recreation, and emergency preparedness. Commercial and industrial enterprises form a significant segment, primarily driven by workplace safety mandates, operational efficiency, and compliance with regulatory standards. Government and defense organizations contribute to the demand for tactical and emergency lighting applications, emphasizing reliability, durability, and adaptability under extreme conditions. The integration of smart features and rechargeable solutions is further driving adoption across all end-user categories, as organizations and individuals seek long-term value, energy efficiency, and operational flexibility.

Explore more data points, trends and opportunities Download Free Sample Report

LED Lenser Market Segmentations

By Product Type

- Handheld Flashlights

- Headlamps

- Lanterns & Area Lights

- Specialized Lighting Tools

By Application

- Industrial & Professional Use

- Outdoor & Recreational Activities

- Emergency & Rescue Services

- Military & Law Enforcement

- Residential & Personal Use

By Distribution Channel

- Online Retail

- Specialty Outdoor Stores

- Hardware & Industrial Supply Stores

- Electronics Retail Chains

By End-User

- Individual Consumers

- Commercial & Industrial Enterprises

- Government & Defense Organizations

Regional Insights

North America

North America holds the largest share of the LED Lenser market, accounting for approximately 32% in 2025. The United States is the dominant contributor, supported by strong participation in outdoor recreational activities, high consumer spending, and widespread industrial infrastructure. Key drivers include stringent workplace safety regulations across construction, mining, and oil & gas industries, which mandate high-quality portable lighting for operational safety. Additionally, increasing adventure tourism and outdoor hobbies, combined with the technological adoption of smart LED devices, are fueling consumer demand. Canada is contributing to growth through government and industrial initiatives emphasizing energy-efficient and durable lighting solutions for both residential and professional applications.

Europe

Europe accounts for around 28% of the global market, led by Germany, the UK, and France. Germany acts as a major manufacturing hub, providing both domestic supply and exports to other regions. Market growth is driven by strict energy efficiency regulations, industrial safety standards, and high adoption of advanced LED technologies. The rise in outdoor recreational activities, such as trekking and adventure sports, particularly in the UK and France, is also increasing consumer demand for lightweight and high-lumen lighting devices. Sustainability initiatives, such as reduced energy consumption mandates and eco-friendly product development, further support market expansion across European countries.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 8.5%. China and India are the primary contributors, driven by rapid industrialization, expanding construction activities, and growing consumer spending. Increasing investments in infrastructure development, including industrial parks, smart cities, and renewable energy projects, are driving demand for durable, high-performance lighting solutions. Rising awareness of workplace safety regulations, combined with the popularity of outdoor adventure sports and domestic tourism, is further supporting the adoption of LED Lenser products. Government incentives for local manufacturing, import substitution policies, and increasing e-commerce penetration also serve as growth enablers in the region.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico. Construction activities, urban infrastructure development, and rising participation in outdoor tourism are major drivers of LED Lenser demand. Increasing adoption of energy-efficient lighting solutions by industrial and commercial enterprises, combined with growing consumer awareness of durable and high-lumen portable lighting devices, is contributing to market expansion. Government investments in public infrastructure, particularly in safety-compliant lighting solutions, further support growth in this region.

Middle East & Africa

The Middle East & Africa region is witnessing moderate growth, supported by infrastructure projects, oil & gas activities, and government-led industrial development. The UAE and Saudi Arabia are key contributors, with high demand from industrial enterprises, defense organizations, and commercial sectors. Drivers include large-scale construction projects, energy-efficiency initiatives, and rising adoption of durable, high-performance lighting devices for both outdoor and industrial applications. In Africa, mining, oil exploration, and government safety initiatives are creating sustained demand for portable LED lighting, while increasing adoption of e-commerce platforms is making these products more accessible to a wider consumer base.

Key Players in the LED Lenser Market

- LED Lenser GmbH & Co. KG

- Streamlight Inc.

- SureFire LLC

- Mag Instrument Inc.

- Energizer Holdings Inc.

- Pelican Products Inc.

- Coast Products Inc.

- Dorcy International Inc.

- Fenix Lighting LLC

- Olight Technology Co., Ltd.

- Princeton Tec

- Black Diamond Equipment Ltd.

- Nitecore (Sysmax Innovations)

- Petzl Group

- Anker Innovations