LED Lamps Market Size

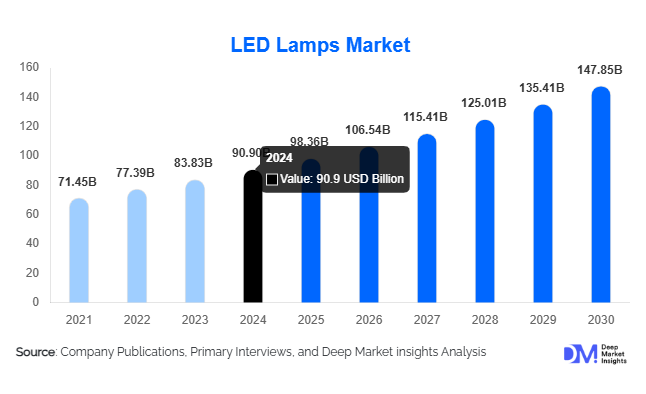

According to Deep Market Insights, the global LED lamps market was valued at USD 90.90 billion in 2025 and is projected to grow from USD 98.36 billion in 2026 to reach USD 147.85 billion by 2031, expanding at a CAGR of 8.32% during the forecast period (2026–2031). The LED lamps market growth is primarily driven by global energy-efficiency regulations, declining LED manufacturing costs, rapid urbanization, and the accelerating replacement of conventional lighting technologies such as incandescent, halogen, and CFL lamps.

Key Market Insights

- Retrofit LED lamps dominate global demand, accounting for over 60% of installations due to government-mandated lighting replacements.

- Asia-Pacific leads global production and consumption, supported by large-scale manufacturing hubs and rapid urban infrastructure growth.

- Commercial applications represent the largest end-use segment, driven by offices, retail chains, and hospitality expansion.

- Smart and connected LED lamps are the fastest-growing product category, supported by smart home and IoT integration.

- Price commoditization continues in standard LED lamps, while premium pricing remains stable for smart and specialty LEDs.

- Public infrastructure investments, including street lighting and smart city projects, are sustaining long-term demand.

LED Lamps Market latest trends

Rapid Adoption of Smart & Connected LED Lamps

Smart LED lamps integrated with IoT platforms, mobile applications, and voice assistants are rapidly gaining market traction. These products allow users to control brightness, color temperature, energy consumption, and scheduling remotely, making them particularly attractive in residential and commercial buildings. Growing adoption of smart home ecosystems across North America, Europe, and parts of Asia-Pacific is driving premiumization within the LED lamps market. Manufacturers are increasingly embedding sensors, AI-driven lighting optimization, and cloud connectivity, enabling energy savings and enhanced user experience.

Expansion of Specialty LED Applications

Beyond general illumination, LED lamps are increasingly used in horticulture, UV disinfection, healthcare lighting, and human-centric lighting. Horticultural LEDs are supporting controlled-environment agriculture and vertical farming, while UV LED lamps are gaining adoption for water, air, and surface sterilization. These applications command higher margins and are reducing dependence on commoditized lighting segments.

LED Lamps Market key drivers

Global Energy Efficiency Regulations

Governments worldwide are enforcing strict energy-efficiency standards and phasing out inefficient lighting technologies. Policies such as minimum energy performance standards and carbon reduction targets are accelerating LED lamp adoption across residential, commercial, and industrial sectors. These regulations have created mandatory replacement demand, particularly in developed economies.

Declining Manufacturing Costs and Technological Advancements

Advances in LED chip efficiency, automated assembly, and economies of scale have reduced production costs significantly. This has improved affordability, enabling mass adoption in price-sensitive markets such as India, Southeast Asia, Africa, and Latin America. Continuous improvements in luminous efficacy and lifespan are further strengthening value propositions.

Urbanization and Infrastructure Development

Rapid urbanization, particularly in emerging economies, is driving demand for residential housing, commercial spaces, and public infrastructure. LED lamps are increasingly preferred due to their durability, low maintenance requirements, and energy savings, making them ideal for large-scale installations.

LED Lamps Market restraints

Margin Pressure from Price Competition

The LED lamps market is highly competitive, with intense price wars in standard bulb categories. This commoditization has compressed profit margins, particularly for manufacturers without scale advantages or differentiated offerings.

Raw Material and Supply Chain Volatility

Fluctuating prices of aluminum, semiconductor components, and rare earth materials can disrupt cost structures. Supply chain disruptions, especially in chip manufacturing, can also impact production timelines and pricing stability.

LED Lamps Market key opportunities

Government-Led Public Lighting Projects

Large-scale public lighting upgrades, including streetlights, highways, railways, and airports, present long-term growth opportunities. Developing economies are investing heavily in LED-based infrastructure to reduce energy consumption and operational costs.

Smart Cities and Building Automation

The global push toward smart cities is creating strong demand for connected LED lighting integrated with building management systems. These projects enable centralized control, predictive maintenance, and energy optimization, offering higher margins for solution providers.

Emerging Markets and Untapped Rural Demand

Electrification initiatives and rural housing programs in Asia-Pacific, Africa, and Latin America are expanding LED lamp adoption in previously underserved regions. Affordable LED products tailored for these markets represent a significant volume opportunity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 90.90 Billion |

| Market Size in 2026 | USD 98.36 Billion |

| Market Size in 2031 | USD 147.85 Billion |

| CAGR | 8.32% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

A-type LED lamps continue to dominate the global LED lamps market, accounting for approximately 34% of total demand in 2025. Their leadership is primarily driven by direct form-factor compatibility with traditional incandescent bulbs, enabling seamless one-to-one replacement without fixture modification. This compatibility has made A-type lamps the preferred choice in large-scale residential retrofitting programs and government-led efficiency initiatives, particularly in developed markets.

Tube LED lamps represent the second-largest product category, driven by strong adoption across commercial and industrial environments. Office buildings, educational institutions, warehouses, and healthcare facilities are rapidly replacing fluorescent tube lighting with LED alternatives to reduce maintenance costs and energy consumption. The long operational lifespan and higher lumen efficiency of tube LEDs make them especially attractive for continuous-use environments.

Power Rating Insights

The 5W–10W power rating segment leads the LED lamps market with nearly 38% share in 2025, as it offers an optimal balance between energy efficiency, lumen output, and affordability. Lamps in this range are widely adopted across residential living spaces, offices, retail stores, and hospitality environments, where moderate brightness and low operating costs are prioritized. Below-5W LED lamps are predominantly used for decorative, accent, and mood lighting applications, including architectural highlights, ambient residential lighting, and hospitality interiors. Growth in this segment is closely linked to rising demand for design-oriented lighting solutions.

LED lamps rated above 20W are increasingly deployed in industrial facilities, warehouses, outdoor lighting, and public infrastructure projects. These high-wattage lamps benefit from superior brightness and durability, making them suitable for high-ceiling and large-area illumination. Growth in this segment is supported by expanding industrial activity and government investments in LED-based street and area lighting.

Distribution Channel Insights

Offline retail remains the largest distribution channel for LED lamps globally, supported by electrical specialty stores, wholesalers, contractors, and institutional procurement networks. This channel continues to dominate due to consumer preference for immediate availability, professional consultation, and contractor-driven bulk purchasing for commercial and infrastructure projects.

However, e-commerce and direct-to-consumer (D2C) channels are the fastest-growing distribution segments. Consumers increasingly rely on online platforms for price comparison, product reviews, energy-efficiency labeling, and home delivery. The growth of smart LED lamps has further accelerated online sales, as digitally native consumers prefer purchasing connected devices through e-commerce platforms. Manufacturers are responding by strengthening their digital presence, launching brand-owned websites, and partnering with major online marketplaces. This shift is also enabling better margin control, data-driven customer engagement, and direct marketing strategies.

End-Use Insights

Commercial applications account for approximately 36% of global LED lamp demand in 2025, making it the largest end-use segment. Offices, retail outlets, hotels, shopping malls, and healthcare facilities are major adopters, driven by high operating hours, energy cost optimization needs, and regulatory compliance requirements. Commercial users benefit significantly from reduced electricity consumption and lower maintenance costs, accelerating LED replacement cycles.

Residential demand is steadily increasing, supported by rising awareness of energy efficiency, declining LED prices, and growing adoption of smart home technologies. Government subsidy programs and mass replacement initiatives in developing economies are further boosting residential penetration. Industrial and outdoor infrastructure segments benefit from long-term replacement demand and large-scale government investments. LED lamps are increasingly used in factories, warehouses, street lighting, highways, and public spaces due to their durability, high luminous efficiency, and lower total cost of ownership.

Explore more data points, trends and opportunities Download Free Sample Report

LED Lamps Market Segmentations

By Product Type

- A-Type LED Lamps

- Tube LED Lamps (T5, T8, T12 Replacements)

- Decorative & Filament LED Lamps

- Smart & Connected LED Lamps

- Specialty LED Lamps

By Power Rating

- Below 5W

- 5W–10W

- 10W–20W

- Above 20W

By Distribution Channel

- Offline Retail (Electrical Stores, Hypermarkets)

- Wholesale & Contractor Sales

- E-commerce & Direct-to-Consumer (D2C)

By End Use

- Residential

- Commercial (Offices, Retail, Hospitality)

- Industrial (Factories, Warehouses)

- Outdoor & Infrastructure (Street Lighting, Public Spaces)

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global LED lamps market with approximately 42% share in 2025, making it both the largest production and consumption hub. China leads due to its massive manufacturing capacity, integrated LED supply chain, and strong domestic demand. India, Japan, and South Korea follow, supported by urban expansion and technological adoption. Key regional growth drivers include rapid urbanization, large-scale housing development, government electrification programs, and cost-competitive manufacturing. India is the fastest-growing country in the region, with a CAGR exceeding 13%, driven by nationwide LED distribution schemes, smart city initiatives, and infrastructure modernization.

North America

North America accounts for approximately 21% of global LED lamp demand, led by the United States. Growth in the region is driven by strict energy-efficiency regulations, widespread commercial retrofitting, and strong adoption of smart and connected lighting solutions. The U.S. market benefits from aggressive replacement of legacy lighting across commercial buildings and public infrastructure. Canada contributes steadily through public sector investments, sustainability-focused building codes, and energy conservation programs.

Europe

Europe holds nearly 19% market share, with Germany, the United Kingdom, and France leading regional adoption. Growth is primarily driven by stringent sustainability mandates, EU Ecodesign regulations, and carbon neutrality targets. European consumers and businesses show a strong preference for high-quality, energy-efficient, and environmentally certified lighting products. Renovation of aging building stock and public infrastructure modernization are further accelerating LED lamp penetration.

Latin America

Latin America is witnessing gradual but steady growth, led by Brazil and Mexico. Public lighting modernization programs, urban development projects, and rising electricity costs are key drivers of LED adoption in the region. Government-backed energy efficiency initiatives and international funding support are encouraging municipalities to replace conventional lighting with LEDs, improving long-term market prospects.

Middle East & Africa

The Middle East benefits from large-scale infrastructure development, smart city investments, and high per-capita energy consumption. Countries such as the UAE and Saudi Arabia are driving demand through mega projects, commercial real estate expansion, and sustainability-focused urban planning. In Africa, market growth is supported by electrification programs, donor-funded LED street lighting projects, and rising urban populations. While adoption levels vary across countries, long-term demand fundamentals remain strong due to the need for reliable and energy-efficient lighting solutions.

Key Players in the LED Lamps Market

- Signify

- ams OSRAM

- Acuity Brands

- Panasonic

- Samsung Electronics

- Havells

- Opple Lighting

- Cree LED

- Zumtobel Group

- NVC Lighting

- Legrand

- Fagerhult

- Eaton

- Sharp

- MLS Lighting