Leather Belts Market Size

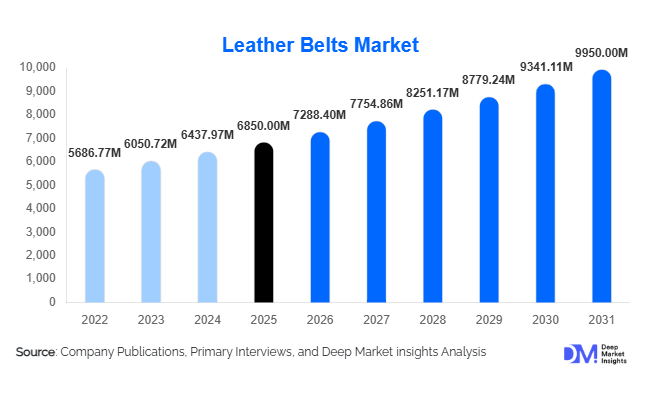

According to Deep Market Insights, the global leather belts market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7,288.40 million in 2026 to reach USD 9,950 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The leather belts market growth is primarily driven by the expansion of the global apparel industry, rising fashion consciousness among consumers, and increasing disposable incomes across emerging economies. Leather belts continue to serve as both functional accessories and fashion statements, with demand spanning formal, casual, and luxury segments.

The market is witnessing a gradual shift toward sustainable materials, including vegan and plant-based leather alternatives, as environmental awareness grows. Additionally, e-commerce expansion has significantly enhanced product accessibility, enabling both global brands and artisanal manufacturers to reach broader audiences. While genuine leather dominates due to its durability and premium appeal, innovation in synthetic materials and customization trends are reshaping consumer preferences. Despite challenges such as fluctuating raw material prices and regulatory pressures on leather processing, the market is expected to maintain steady growth through technological advancements and diversification in product offerings.

Key Market Insights

- Genuine leather belts dominate the market, accounting for approximately 62% share due to durability and premium positioning.

- Casual belts are the leading product segment, driven by increasing global adoption of relaxed dress codes.

- Asia-Pacific leads the global market, supported by strong manufacturing capabilities and rising domestic demand.

- Online retail is the fastest-growing distribution channel, fueled by convenience, discounts, and product variety.

- Vegan and sustainable leather alternatives are gaining traction, particularly among environmentally conscious consumers.

- Mid-range pricing segment dominates, balancing affordability and quality for mass consumers.

What are the latest trends in the leather belts market?

Shift Toward Sustainable and Vegan Materials

The leather belts market is experiencing a notable shift toward sustainability, with manufacturers increasingly adopting vegan and plant-based leather alternatives. Materials derived from sources such as cactus, pineapple fibers, and mushrooms are gaining popularity as eco-friendly substitutes. This trend is driven by growing environmental awareness, stricter regulations on leather processing, and consumer preference for ethical products. Brands are leveraging sustainability as a key differentiator, introducing eco-certified belts and transparent supply chains. Premium pricing for sustainable products is also becoming acceptable among younger consumers, further accelerating adoption. As a result, companies investing in sustainable innovation are well-positioned to capture emerging demand segments.

Digital Transformation in Retail and Customization

E-commerce platforms and digital tools are transforming how leather belts are marketed and sold. Online marketplaces and direct-to-consumer websites are enabling brands to reach global audiences while offering competitive pricing. Additionally, customization features such as personalized belt sizes, buckle designs, and engraving options are gaining traction. Technologies like augmented reality (AR) are enhancing the online shopping experience by allowing customers to visualize products before purchase. AI-driven demand forecasting and inventory management are also improving operational efficiency. This digital transformation is particularly appealing to younger, tech-savvy consumers who prioritize convenience and personalization.

What are the key drivers in the leather belts market?

Expansion of the Global Apparel Industry

The steady growth of the global apparel industry is a major driver for the leather belts market. As belts are essential complementary accessories for both formal and casual wear, increasing clothing consumption directly translates into higher belt demand. The rise of fast fashion and seasonal collections has further amplified this trend, encouraging consumers to purchase multiple belt styles to match different outfits.

Rising Disposable Income and Fashion Awareness

Increasing disposable income, particularly in emerging economies, is driving higher spending on fashion accessories. Consumers are increasingly viewing belts as style statements rather than purely functional items. This shift is evident in the growing demand for premium and designer belts, as well as the popularity of branded products among younger demographics. Social media and influencer marketing are also playing a significant role in shaping consumer preferences.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in the prices of raw materials, particularly genuine leather, pose a significant challenge for manufacturers. Factors such as livestock availability, tanning costs, and environmental compliance expenses can impact production costs and profit margins. This volatility often leads to price fluctuations in the final product, affecting consumer demand.

Regulatory and Environmental Constraints

Stringent environmental regulations related to leather processing and waste management are creating operational challenges for manufacturers. Compliance with these regulations requires significant investment in cleaner technologies and sustainable practices. Smaller players, in particular, may struggle to meet these requirements, potentially limiting market growth.

What are the key opportunities in the leather belts industry?

Expansion in Emerging Markets

Emerging economies in the Asia-Pacific, Africa, and Latin America present significant growth opportunities for the leather belts market. Rapid urbanization, rising middle-class populations, and increasing exposure to global fashion trends are driving demand for accessories. Countries such as India, Indonesia, and Brazil are witnessing strong growth in retail infrastructure and e-commerce adoption, creating favorable conditions for market expansion.

Integration of Advanced Manufacturing Technologies

The adoption of advanced manufacturing technologies such as automation, AI-driven production planning, and sustainable tanning processes is creating opportunities for efficiency and cost optimization. These technologies not only improve product quality but also reduce environmental impact. Companies investing in innovation can gain a competitive edge by offering high-quality products at competitive prices while meeting regulatory requirements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6850 Million |

| Market Size in 2026 | USD 7288.40 Million |

| Market Size in 2031 | USD 9950 Million |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Casual belts dominate the global leather belts market with approximately 38% share, primarily driven by the global shift toward relaxed dress codes, lifestyle changes, and the growing prevalence of casual workplace environments. Consumers increasingly view belts as fashion statements rather than purely functional items, fueling demand for diverse colors, designs, and finishes. Formal belts maintain steady demand, particularly in corporate and business settings, reflecting the sustained need for professional attire. Luxury belts cater to high-income consumers seeking premium materials, craftsmanship, and strong brand identity, benefiting from rising disposable incomes and the status-driven appeal of designer accessories. Emerging segments such as utility and sports belts are witnessing incremental growth due to rising awareness of workplace safety and fitness trends, where functional belts are increasingly required for industrial, tactical, and athletic applications. Overall, the diversification of product types allows manufacturers to target a broad spectrum of consumer needs, from mass-market affordability to high-end premium offerings, ensuring steady market expansion across regions.

Material Type Insights

Genuine leather remains the dominant material segment, accounting for around 62% of the market, due to its durability, premium appeal, and long lifecycle, which positions it as the preferred choice for both formal and luxury segments. Synthetic leather, including PU and PVC, is widely used in economy and mid-range segments, offering affordability, versatile aesthetics, and ease of maintenance. Vegan and plant-based leather alternatives are the fastest-growing material segment, propelled by increasing environmental consciousness, sustainability trends, and stricter regulatory frameworks governing animal-based products. Hybrid materials combining leather with textiles are also gaining traction, offering unique aesthetics, cost advantages, and flexibility in casual and fashion-forward designs. The rise of sustainable consumer preferences, particularly among millennials and Gen Z, is accelerating adoption of alternative materials, creating new opportunities for manufacturers to innovate while reducing environmental impact.

Distribution Channel Insights

Offline retail channels continue to hold a dominant position, accounting for approximately 60% of the market. This dominance is driven by consumers’ preference for tactile product evaluation, brand credibility, and immediate purchase availability, particularly in department stores, specialty stores, and brand outlets. However, online retail is the fastest-growing distribution channel, fueled by expanding internet penetration, mobile commerce adoption, convenience, and access to competitive pricing. E-commerce platforms, including marketplaces and brand-owned websites, enable global reach and facilitate direct-to-consumer sales, allowing smaller and niche manufacturers to compete with established brands. The digital channel also supports enhanced customization, personalized recommendations, and virtual try-on features, which are influencing purchase decisions and expanding market penetration, particularly in urban and tech-savvy consumer segments.

End-Use Insights

The men’s segment dominates the leather belts market with around 55% share, as belts are integral to both formal and casual menswear. Increasing fashion awareness and disposable incomes among male consumers are driving demand for mid-range and premium belts. The women’s segment is gaining momentum as belts are increasingly adopted as stylish accessories to complement dresses, coats, and casual attire. The kids’ segment, although smaller, is growing steadily due to rising demand for branded apparel and accessories for children. The primary end-use sector remains the apparel industry, encompassing formal, casual, and luxury wear. Additionally, industrial, tactical, and sports applications are emerging as niche end-use segments, particularly in regions with growing workplace safety awareness, fitness culture, and recreational sports adoption. Export-oriented manufacturing in countries like China and India further supports demand across global end-use sectors.

Explore more data points, trends and opportunities Download Free Sample Report

Leather Belts Market Segmentations

By Product Type

- Casual Belts

- Formal Belts

- Luxury Belts

- Utility & Sports Belts

By Material Type

- Genuine Leather

- Synthetic Leather

- Vegan/Plant-Based Leather

- Hybrid Leather-Textile Materials

By Distribution Channel

- Offline Retail

- Online Retail

By End-Use

- Men’s Apparel

- Women’s Apparel

- Kids’ Apparel

- Industrial & Sports Applications

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global leather belts market with approximately 34% share in 2025, led by China and India. China functions as a major manufacturing and export hub, benefiting from cost-effective production, large-scale infrastructure, and strong international supply chains. India is witnessing rising domestic demand driven by urbanization, increasing disposable income, and rapid growth of organized retail and e-commerce platforms. The casual and mid-range belt segments are particularly strong in this region due to shifting lifestyles, expanding office culture, and young consumers’ preference for trendy accessories. Key growth drivers include large-scale manufacturing capabilities, increasing consumer fashion awareness, and government support for textile and leather industries through initiatives promoting exports and industrial clusters.

North America

North America accounts for around 26% of the global market, with the United States as the primary contributor. The region is characterized by high disposable incomes, strong fashion consciousness, and mature retail infrastructure. Demand is especially strong in luxury and mid-range belt segments due to preference for premium brands and designer labels. Online retail adoption is high, allowing consumers to access global brands with ease. Regional growth drivers include consumer demand for luxury and branded accessories, established e-commerce penetration, lifestyle-driven fashion trends, and the sustained influence of corporate and casual dress norms on product demand.

Europe

Europe holds approximately 24% share, led by Italy, Germany, and France. Italy is globally recognized for luxury leather craftsmanship, especially in premium and designer belt segments. Germany and France contribute to mid-range and casual belt demand due to strong fashion awareness and high disposable incomes. European consumers are increasingly adopting sustainable and ethically produced belts, driving growth in vegan and plant-based materials. Regional growth drivers include strong brand heritage, consumer preference for high-quality craftsmanship, regulatory support for sustainable manufacturing, and rising demand for premium and ethically sourced products.

Latin America

Latin America accounts for about 8% of the market, with Brazil and Mexico as key contributors. Growth is supported by expanding retail sectors, increasing disposable income, and rising interest in global fashion trends. Demand for casual and mid-range belts is particularly strong among urban populations, while premium belt adoption is increasing in affluent segments. Regional growth drivers include urbanization, rising e-commerce adoption, increasing brand awareness, and gradual expansion of organized retail networks.

Middle East & Africa

The Middle East & Africa region holds around 8% share and is the fastest-growing market, with a CAGR of approximately 7.5%. The UAE, Saudi Arabia, and South Africa are leading contributors, with strong demand for luxury and branded belts driven by high disposable incomes and a growing retail and tourism ecosystem. Casual and fashion belts are increasingly adopted by younger urban consumers, while premium and designer belts appeal to high-net-worth individuals. Regional growth drivers include rising disposable incomes, expansion of shopping malls and luxury retail outlets, increasing tourism and cross-border trade, and growing fashion consciousness among youth demographics.

Key Players in the Leather Belts Market

- VF Corporation

- Kering

- LVMH

- Hermès International

- Capri Holdings

- Fossil Group

- PVH Corp.

- Levi Strauss & Co.

- Hugo Boss

- Burberry Group

- Richemont

- Tapestry Inc.

- Prada Group

- Titan Company Limited

- Woodland (Aero Group)