Laundry Detergent Sheets Market Size

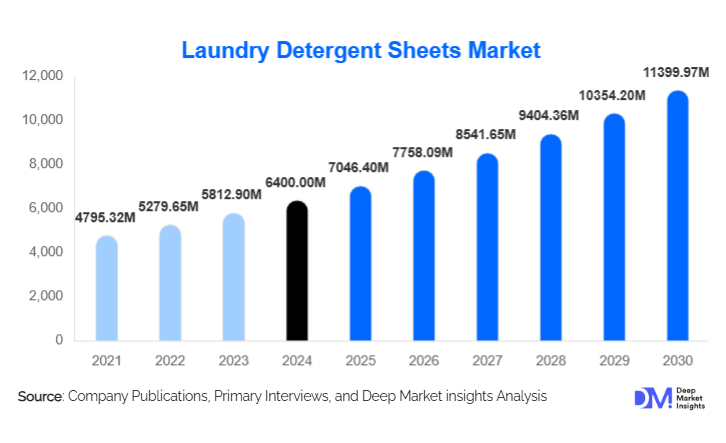

According to Deep Market Insights, the global laundry detergent sheets market size was valued at USD 6,400 million in 2025 and is projected to grow to USD 7,046.40 million in 2026, eventually reaching USD 11,399.97 million by 2031. The market is expected to expand at a strong CAGR of 10.1% during the forecast period (2026–2031). Growth is driven by increasing consumer preference for eco-friendly home care solutions, rising demand for lightweight and travel-friendly detergent formats, and global sustainability pressure encouraging brands to shift toward plastic-free packaging.

Key Market Insights

- Eco-friendly formats are rapidly replacing traditional liquid and powder detergents, driven by regulatory pressure against single-use plastics and rising consumer sustainability awareness.

- Online retail dominates distribution, supported by subscription-based laundry services, D2C brand launches, and digital-first sustainability brands.

- North America leads global consumption, propelled by high adoption of natural household cleaners and premium detergent formats.

- Asia-Pacific (APAC) is the fastest-growing regional market, led by urbanization, rising disposable incomes, and growing e-commerce penetration.

- Brands are integrating advanced formulations, including enzyme-based deep-clean technologies, hypoallergenic blends, and cold-water efficiency.

- Private-label and retail-exclusive detergent sheet brands are expanding rapidly as supermarkets introduce sustainable home-care product lines.

Laundry Detergent Sheets Market Trends

Plastic-Free and Zero-Waste Packaging Accelerating Adoption

Growing environmental concerns and legislative bans on plastic packaging are driving rapid adoption of detergent sheets. Major markets in North America, Europe, and parts of APAC are witnessing retail transitions toward zero-waste home-care products, with detergent sheets positioned as a leading sustainable alternative. Brands increasingly promote carbon-neutral and biodegradable packaging, integrating compostable paper cartons and plant-based films. Regulators are encouraging sustainable laundry solutions through extended producer responsibility (EPR) programs, accelerating category penetration. The trend is further supported by consumer preference for low-waste lifestyles and minimalistic household product formats.

Concentrated and Enzyme-Rich Formulations Improving Cleaning Performance

Advanced R&D investments are driving significant improvements in sheet-based detergent formulations. Enzyme-rich and plant-based surfactants are now commonly integrated to match or exceed the cleaning performance of liquid and powder detergents. Cold-water efficiency, stain-removal additives, antibacterial properties, and hypoallergenic blends are becoming essential differentiators. These innovations address earlier consumer concerns about cleaning effectiveness, expanding mainstream acceptance. Many brands are marketing dermatologically tested, baby-safe, and fragrance-free variants catering to sensitive-skin consumers, enabling broader market penetration across households with children and elderly populations.

Laundry Detergent Sheets Market Drivers

Growing Demand for Sustainable and Low-Waste Home Care Products

Consumers are increasingly seeking sustainable household solutions, and detergent sheets have become a flagship category within eco-friendly cleaning. Rising awareness about microplastics, plastic waste, and carbon emissions is encouraging consumers to shift away from traditional detergent bottles. Global retail brands and supermarkets are expanding green product portfolios, further propelling demand. The small carbon footprint associated with lightweight sheet formats, due to lower shipping weight, has become a major driver for logistics-heavy markets such as the U.S. and Europe.

Convenience, Portability, and Hygiene Benefits

Laundry detergent sheets offer spill-proof, travel-friendly, and pre-measured convenience, making them attractive for busy urban households, college students, and travelers. The convenience factor is driving popularity in both developed and emerging markets. Their low storage space requirements and easy usability appeal to consumers living in smaller apartments, especially in Asia-Pacific megacities. Additionally, the rising adoption of compact washing machines and smart laundry appliances is increasing compatibility with concentrated sheet detergents, supporting long-term market expansion.

Rapid Growth of E-Commerce and D2C Sustainability Brands

The rise of D2C eco-brands has significantly shaped the market. Subscription-based laundry sheet offerings, influencer marketing, and social-media-driven sustainability campaigns are accelerating global adoption. E-commerce platforms enable small eco brands to scale quickly, launching regional and international markets without heavy retail investments. Digital-first promotion strategies have expanded consumer awareness and reduced price sensitivity among young urban consumers willing to pay premiums for eco-friendly products.

Laundry Detergent Sheets Market Restraints

Perception of Lower Cleaning Power Compared to Traditional Detergents

Despite advancements in formulations, some consumers still perceive detergent sheets as less effective for heavy-duty laundry. In markets with high soil levels or cultural preferences for strong fragrances, such as parts of India, the Middle East, and Latin America, adoption remains slow. Heavy-commercial laundry users, such as hotels and hospitals, also show limited uptake due to stringent cleaning standards, acting as a restraint on market expansion.

Higher Price Point and Limited Retail Shelf Space

Detergent sheets are generally priced 20–35% higher than conventional detergents, restricting adoption among cost-sensitive households. Retail penetration remains limited outside North America and select European countries. Many supermarkets allocate minimal shelf space to eco-friendly alternatives, slowing broader consumer exposure. Increased cost of plant-based surfactants and biodegradable packaging materials also affects profit margins, pushing brands to rely heavily on online channels.

Laundry Detergent Sheets Market Opportunities

Expansion into Emerging Markets with Growing Middle-Class Populations

Rising income levels across Southeast Asia, India, Brazil, and Africa present major opportunities for global brands. Urbanization and exposure to global sustainability trends are accelerating adoption in these markets. With improving e-commerce logistics and wider smartphone penetration, detergent sheet brands can scale rapidly using digital-first business models. Local manufacturing partnerships and franchising models can help reduce import duties and support competitive pricing.

Integration of Smart Laundry Technology and Specialty Sheets

There is significant potential to innovate in specialty sheets for odor removal, color protection, fabric conditioner integration, and sensitive-skin applications. Companies are also exploring dissolvable antimicrobial sheets for premium markets. The rise of smart washing machines opens the door for optimized sheet formulations, enabling automatic dispensing and sensor-based cleaning modes. This technological integration will differentiate premium brands and attract tech-savvy households globally.

Institutional and Hospitality Sector Penetration

As sustainability becomes a central ESG mandate for hotels, resorts, student housing, and serviced apartments, detergent sheets provide a low-waste solution that aligns with corporate environmental goals. Hotels are increasingly adopting eco-friendly laundry programs, creating a new institutional demand segment. Bulk-format detergent sheets, biodegradable refill packs, and commercial-cleaning-grade formulations could unlock multi-million-dollar B2B submarkets by 2031.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6400 Million |

| Market Size in 2026 | USD 7046.40 Million |

| Market Size in 2031 | USD 11399.97 Million |

| CAGR | 10.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fresh-scented detergent sheets account for the largest share due to widespread household preference for lightly fragranced laundry products. Unscented and hypoallergenic sheets are rapidly growing, driven by rising skin-sensitivity concerns and demand from families with infants. Specialty sheets, such as color guard, fabric softener–infused, and antibacterial variants, are expanding as brands differentiate through value-added formulations. Multipurpose sheets that combine detergent and softener in a single strip are gaining traction among minimalist and budget-conscious consumers.

Application Insights

Household laundry dominates global consumption, accounting for the majority share of detergent sheet usage. Commercial applications, including hotels, student dormitories, vacation rentals, and co-living spaces, are growing steadily as hospitality businesses adopt low-waste cleaning solutions. Travel applications, including RVs, cruise ships, and aviation, display strong adoption potential due to portability and low storage weight. Outdoor campers and backpackers also increasingly favor detergent sheets for their compact format and biodegradability.

Distribution Channel Insights

Online retail and D2C channels hold the highest market share, driven by digital-first sustainability brands and subscription-based models. Supermarkets and hypermarkets are expanding detergent sheet space, particularly in North America and Europe, creating opportunities for mass-market growth. Specialty eco-stores and zero-waste shops are emerging as key niche channels. Wholesale clubs and warehouse retailers are beginning to stock family-sized refill packs, supporting bulk purchasing trends.

End-User Insights

Residential users form the core consumer group, supported by urbanization, smaller living spaces, and rising interest in sustainable home care. The institutional sector, including hospitality, education, and co-living, shows high growth potential as ESG compliance becomes mandatory across global industries. The commercial laundry sector is gradually adopting sheet-based detergents in eco-lodges, hostels, and boutique hotels, though cleaning-strength perception challenges still slow adoption in industrial laundromats.

Explore more data points, trends and opportunities Download Free Sample Report

Laundry Detergent Sheets Market Segmentations

By Product Type

- Fresh-Scented Laundry Detergent Sheets

- Unscented/Hypoallergenic Laundry Detergent Sheets

- Enzyme-Based Deep Cleaning Sheets

- Fabric Softener–Infused Sheets

- Antibacterial & Specialty Laundry Sheets

By Application

- Household Laundry

- Commercial Laundry (Hotels, Dormitories, Rentals)

- Travel & Outdoor Use

- Institutional Use (Schools, Co-living, Healthcare)

By Distribution Channel

- Online Retail (E-commerce, D2C Brands)

- Supermarkets & Hypermarkets

- Specialty Eco Stores & Zero-Waste Shops

- Wholesale Clubs

- Convenience Stores & Local Retailers

By End User

- Residential

- Commercial (Hospitality, Vacation Rentals)

- Institutional (Education, Co-living, Healthcare)

Regional Insights

North America

North America is the largest market, contributing approximately 38% of the global 2025 demand. High adoption of natural household cleaners, a well-developed e-commerce ecosystem, and a strong presence of D2C eco-brands underpin regional leadership. The U.S. is the dominant country, while Canada’s sustainability-driven consumers support strong per-capita usage. Major retailers such as Walmart, Target, and Costco have expanded their detergent sheet offerings, supporting retail penetration.

Europe

Europe holds around 29% market share, driven by strict environmental regulations, high consumer sustainability awareness, and widespread demand for minimal-waste home-care products. Germany, the U.K., France, and the Nordics lead consumption. EU packaging directives and anti-plastic policies strongly support detergent sheet adoption. European consumers prefer unscented, biodegradable, and plant-based formulations, shaping product development trends.

Asia-Pacific

APAC is the fastest-growing region with a forecast CAGR above 12%. China, Japan, South Korea, and India are driving adoption, fueled by rapid urbanization, expanding e-commerce channels, and rising disposable incomes. South Korea and Japan show particularly high interest due to compact living trends and a culture of innovation-driven home care. India’s market is at an early adoption stage but is expected to grow rapidly with expanding middle-class demand and domestic manufacturing initiatives.

Latin America

Latin America shows steady growth, led by Brazil and Mexico, where sustainability awareness and urban retail expansion are increasing in adoption. Price sensitivity remains a barrier, but the rise of local eco-brands and regional e-commerce platforms is improving accessibility.

Middle East & Africa

MEA is an emerging market with rising adoption in the UAE, Saudi Arabia, and South Africa. High expatriate populations, premium retail chains, and sustainability-led policies are driving demand. The region remains small but is projected to grow significantly through 2031.

Key Players in the Laundry Detergent Sheets Market

- Earth Breeze

- Tru Earth

- Sheets Laundry Club

- Kind Laundry

- Eco Living Club

- Clean People

- Breezeo

- Beyond Laundry

- Biokleen

- Attitude Living

- ECOS

- Blueland

- Dropps

- Everdrop

- Puracy

Recent Developments

- January 2025: Tru Earth launched a commercial-grade sheet detergent line targeting hotels and serviced apartments, aiming for zero-waste laundry operations.

- March 2025: Blueland introduced an enzyme-boosted laundry sheet designed for cold-water stain removal, enhancing energy efficiency during washing.

- July 2025: Earth Breeze expanded production capacity in the U.S. to support rising subscription demand and reduce carbon footprint from imports.