Laundry Care Products Market Size

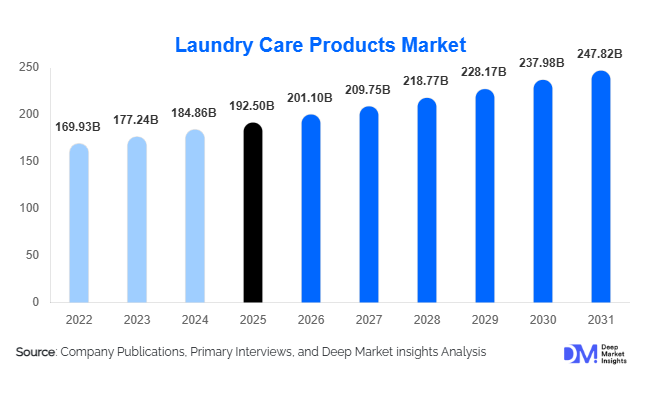

According to Deep Market Insights, the global laundry care products market size was valued at USD 192.5 billion in 2025 and is projected to grow from USD 201.1 billion in 2026 to reach USD 247.82 billion by 2031, expanding at a CAGR of 4.3% during the forecast period (2026–2031). The laundry care products market growth is primarily driven by rising hygiene awareness, increasing washing machine penetration across emerging economies, and strong premiumization trends in developed markets. Innovation in concentrated formulations, eco-friendly detergents, and convenient formats such as pods and capsules is reshaping consumer preferences globally.

Key Market Insights

- Liquid detergents dominate product innovation, supported by growing adoption of automatic and high-efficiency washing machines.

- Asia-Pacific leads global demand, accounting for nearly 36% of the 2025 market share, driven by China and India.

- Mid-range products represent the largest price tier, contributing approximately 49% of global revenue.

- Supermarkets and hypermarkets remain the leading distribution channel, with around 45% share, although e-commerce is expanding rapidly.

- Bio-based and sustainable formulations are growing faster than conventional products, particularly in Europe and North America.

- The top five players account for nearly 58% of global revenue, indicating strong brand concentration and competitive intensity.

What are the latest trends in the laundry care products market?

Sustainable and Bio-Based Formulations Gaining Momentum

Environmental regulations and shifting consumer preferences are accelerating demand for plant-based surfactants, phosphate-free detergents, and recyclable packaging. In Europe and North America, consumers increasingly prefer low-temperature wash detergents that reduce energy consumption. Concentrated formulations requiring smaller packaging volumes are also gaining traction, lowering carbon footprints and transportation costs. Refill packs and waterless detergent sheets are emerging as innovative solutions aimed at minimizing plastic waste.

Premiumization and Convenience-Led Innovation

Consumers are moving beyond basic cleaning functionality toward enhanced fragrance, fabric care, and skin-sensitive formulations. Detergent pods and capsules are witnessing strong uptake due to ease of use and precise dosing. Smart dispensing systems integrated with high-efficiency washing machines are also gaining popularity in developed markets. Subscription-based detergent deliveries through e-commerce platforms are further strengthening brand loyalty and recurring revenue models.

What are the key drivers in the laundry care products market?

Rising Hygiene Awareness and Health Consciousness

Post-pandemic hygiene standards have increased consumer focus on anti-bacterial and odor-eliminating formulations. The healthcare and hospitality industries are also expanding procurement of high-performance laundry chemicals to maintain stringent sanitation protocols. This sustained awareness continues to boost both household and commercial demand.

Urbanization and Washing Machine Penetration

Rapid urbanization in the Asia-Pacific and Africa is driving washing machine ownership growth. Automatic washing machines require specialized detergents, particularly liquid and high-efficiency variants. Countries such as China and India are experiencing steady mid-single-digit growth in appliance adoption, directly supporting detergent sales expansion.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in crude oil-derived surfactants and palm oil-based oleochemicals significantly impact production costs. Manufacturers face margin pressures when unable to fully pass cost increases to consumers in price-sensitive markets.

Regulatory Compliance and Environmental Restrictions

Stringent global regulations on phosphates, microplastics, and packaging waste increase compliance costs. Smaller manufacturers often struggle to meet evolving environmental standards, limiting market entry and expansion.

What are the key opportunities in the laundry care products industry?

Emerging Market Expansion

Rising middle-class populations in India, Indonesia, Nigeria, and Vietnam present significant growth opportunities. Branded detergent penetration remains lower in these regions compared to developed markets, allowing multinational companies to capture incremental market share through affordable packaging and localized marketing strategies.

Smart and Concentrated Product Formats

Ultra-concentrated liquids and pre-measured pods reduce water usage and packaging waste. Integration with IoT-enabled appliances capable of automated detergent dosing presents long-term growth potential. Companies investing in R&D for enzyme-enhanced cleaning at lower wash temperatures are expected to gain a competitive advantage.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 192.5 Billion |

| Market Size in 2026 | USD 201.1 Billion |

| Market Size in 2031 | USD 247.82 Billion |

| CAGR | 4.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Laundry detergents continue to dominate the global market, accounting for approximately 72% of total 2025 revenue, making them the primary revenue engine of the industry. The leadership of this segment is fundamentally driven by the essential nature of detergents in daily household cleaning, combined with rising washing machine penetration globally. Within detergents, liquid detergents represent the leading sub-segment, supported by their compatibility with automatic and high-efficiency (HE) washing machines, superior solubility in cold water, and ability to support concentrated formulations. The shift toward cold-water washing to reduce electricity consumption has further accelerated liquid detergent adoption in North America and Europe.

Detergent pods and capsules are the fastest-growing format within the category, benefiting from convenience, precise dosing, and premium positioning. Meanwhile, fabric softeners and conditioners provide a strong secondary revenue stream, particularly in developed markets where consumers prioritize fragrance longevity and fabric protection. Stain removers and laundry additives are expanding steadily as consumers increasingly demand specialized performance solutions, including enzyme-based stain targeting, color protection, and anti-bacterial enhancements. This performance-driven consumer shift is reinforcing value growth across premium sub-segments globally.

Formulation Type Insights

Conventional synthetic-based detergents account for nearly 68% of the 2025 market share, maintaining leadership due to affordability, strong cleaning efficacy, and well-established supply chains. Price-sensitive emerging markets such as India, Indonesia, Brazil, and parts of Africa continue to rely heavily on conventional formulations, ensuring volume stability. The scalability of petrochemical-based surfactant production and widespread raw material availability further support this segment’s dominance.

However, bio-based and plant-derived formulations are growing at over 6% CAGR, outpacing overall market expansion. Growth drivers include stringent phosphate bans in Europe, microplastic restrictions, carbon-neutral commitments from multinational brands, and increasing consumer willingness to pay a premium for eco-friendly products. North America and Western Europe lead adoption, while Asia-Pacific is gradually increasing demand as regulatory frameworks strengthen. Concentrated and high-efficiency formulations also contribute to growth by reducing packaging waste and logistics costs, aligning sustainability with operational efficiency.

Distribution Channel Insights

Supermarkets and hypermarkets represent around 45% of global sales, retaining leadership due to high foot traffic, private-label competition, and promotional pricing strategies. Large retail chains provide extensive shelf visibility, enabling both multinational brands and regional players to capture impulse purchases and bundle promotions. This channel remains particularly dominant in North America and Europe, where organized retail penetration exceeds 70%.

Online retail has surpassed 16% market share and is the fastest-growing channel, driven by subscription models, doorstep delivery convenience, and price comparison transparency. E-commerce growth is particularly strong in China, the United States, South Korea, and India. Direct-to-consumer (D2C) brand websites are gaining traction for premium and eco-friendly detergents, enabling personalized marketing and recurring revenue streams. Institutional and B2B distribution channels also remain critical, especially in commercial and healthcare applications.

End-Use Insights

The household segment holds approximately 79% of total market demand, reflecting the non-discretionary and recurring nature of laundry care consumption. Growth in this segment is supported by population expansion, urbanization, and rising disposable incomes. Premiumization trends in developed economies are further increasing average selling prices within the residential category.

The commercial segment, including hospitality, healthcare, laundromats, and industrial facilities, is expanding at over 5% CAGR, outpacing household growth. Healthcare infrastructure expansion in Asia-Pacific and the Middle East is significantly increasing institutional detergent demand, particularly for anti-microbial and high-temperature wash formulations. Growth in global tourism and hospitality recovery is also boosting bulk detergent consumption. Export-driven production from China, Germany, and the United States strengthens international supply chains, ensuring consistent availability across regions.

Explore more data points, trends and opportunities Download Free Sample Report

Laundry Care Products Market Segmentations

By Product Type

- Laundry Detergents

- Fabric Softeners & Conditioners

- Stain Removers & Pre-Treatment Agents

- Bleaching Agents

- Laundry Additives

By Formulation Type

- Conventional / Synthetic-Based

- Bio-Based / Plant-Derived

- Concentrated / High-Efficiency (HE)

- Hypoallergenic / Sensitive Skin Formulations

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-Commerce

- Institutional / B2B Supply

- Specialty Stores

By End-Use

- Household / Residential

- Hospitality

- Healthcare

- Laundromats

- Industrial & Manufacturing Facilities

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with nearly 36% share in 2025, making it the largest revenue contributor. China alone accounts for approximately 18% of global revenue, supported by a large urban population, strong domestic manufacturing capacity, and rapid e-commerce penetration. India is the fastest-growing major market, expanding at nearly 6% CAGR, driven by rising middle-class income, expanding rural distribution networks, and increasing washing machine penetration. Southeast Asian countries such as Indonesia and Vietnam are also witnessing steady demand growth due to urbanization and improving retail infrastructure. Local production capacity, lower labor costs, and government initiatives supporting domestic manufacturing further reinforce regional leadership.

North America

North America holds about 24% of the global market share, with the United States contributing over 85% of the regional revenue. Growth drivers include high per-capita detergent consumption, widespread adoption of automatic washing machines, and strong demand for premium, concentrated, and sustainable formulations. The region also benefits from advanced retail infrastructure, well-developed e-commerce ecosystems, and high consumer spending power. Innovation in fragrance technology and enzyme-based cleaning solutions further sustains value growth in this mature market.

Europe

Europe represents around 22% share, led by Germany, the UK, and France. The primary driver in this region is stringent environmental regulation, including phosphate bans and packaging reduction mandates, which accelerate innovation in biodegradable and concentrated detergents. High consumer awareness of sustainability and preference for eco-label-certified products contribute to premium pricing. Eastern European countries are also contributing incremental growth due to rising incomes and improving retail penetration.

Latin America

Latin America accounts for nearly 10% of the market, with Brazil and Mexico as the primary contributors. Growth is driven by economic stabilization, urban population growth, and increasing penetration of branded products over unorganized alternatives. Promotional pricing strategies and smaller packaging formats are widely used to address price sensitivity. Expansion of modern retail and digital commerce platforms is further enhancing market accessibility.

Middle East & Africa

The Middle East & Africa (MEA) region holds approximately 8% share but is the fastest-growing region at about 6.5% CAGR. Saudi Arabia, the UAE, and South Africa are key demand centers, supported by population growth, infrastructure expansion, and rising healthcare investments. Urban development initiatives and increasing hospitality capacity in the Gulf Cooperation Council (GCC) countries are driving commercial detergent consumption. In Sub-Saharan Africa, rising urbanization and improving distribution networks are gradually increasing penetration of branded laundry care products, positioning the region for long-term expansion.

Key Players in the Laundry Care Products Market

- Procter & Gamble

- Unilever

- Henkel

- Reckitt

- Church & Dwight

- Kao Corporation

- Lion Corporation

- Colgate-Palmolive

- SC Johnson

- LG Household & Health Care

- Amway

- Nice Group

- RSPL Group

- Golrang Industrial Group

- Fábrica de Jabón La Corona