Laptop Battery Market Size

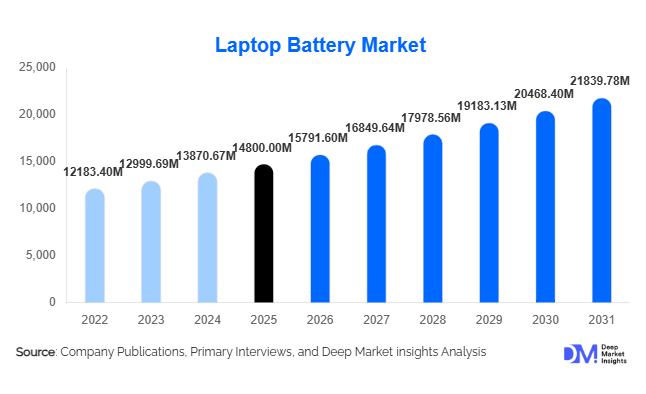

According to Deep Market Insights, the global laptop battery market size was valued at USD 14,800 million in 2025 and is projected to grow from USD 15,791.60 million in 2026 to reach USD 21,839.78 million by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The laptop battery market growth is primarily driven by increasing global laptop penetration, rising demand for high-performance portable computing devices, and the growing adoption of hybrid work and digital education ecosystems worldwide.

Key Market Insights

- Lithium-ion batteries dominate the market, accounting for nearly 68% share due to superior energy density and lifecycle performance.

- OEM channels lead distribution, contributing over 60% of global demand as batteries are integrated during laptop manufacturing.

- Asia-Pacific dominates production and consumption, supported by strong electronics manufacturing ecosystems in China and emerging demand in India.

- Non-removable batteries account for over 70% share, driven by the shift toward slim and lightweight laptop designs.

- Enterprise and corporate usage remains the largest end-use segment, supported by increasing IT infrastructure investments.

- Aftermarket replacement demand is steadily rising, driven by battery lifecycle limitations and growing installed laptop base.

What are the latest trends in the laptop battery market?

Shift Toward High-Energy Density and Fast-Charging Batteries

The market is witnessing a strong shift toward advanced lithium-ion and lithium-polymer batteries with higher energy density and rapid charging capabilities. Consumers and enterprises increasingly demand longer battery life and minimal downtime, pushing manufacturers to innovate in fast-charging technologies and thermal management systems. Integration of intelligent battery management systems is also improving efficiency, safety, and longevity. These advancements are particularly critical in gaming laptops and enterprise-grade devices, where performance demands are significantly higher.

Integration of Sustainable and Recyclable Battery Solutions

Sustainability is becoming a central focus, with manufacturers investing in recyclable materials and circular economy models. Battery recycling initiatives and second-life applications are gaining traction, particularly in Europe and North America, where environmental regulations are stringent. Companies are also exploring reduced cobalt usage and eco-friendly chemistries to minimize environmental impact. This trend is expected to reshape supply chains and create new revenue streams in battery refurbishment and recycling.

What are the key drivers in the laptop battery market?

Growth in Remote Work and Digital Education

The widespread adoption of remote and hybrid work models has significantly increased reliance on laptops, directly boosting demand for high-performance batteries. Similarly, digital education initiatives across emerging economies have expanded laptop usage among students, creating sustained demand for both OEM and replacement batteries. This structural shift toward digital platforms is expected to remain a long-term growth driver.

Rising Demand for High-Performance and Gaming Laptops

The rapid growth of gaming and professional computing has led to increased demand for high-capacity batteries, particularly in the 60–80 Wh and above segments. Gaming laptops and workstations require robust battery solutions capable of supporting power-intensive applications, driving higher revenue per unit and technological advancements in battery design.

What are the restraints for the global market?

Volatility in Raw Material Prices

The laptop battery market is heavily dependent on raw materials such as lithium, cobalt, and nickel. Price volatility and supply chain disruptions can significantly impact manufacturing costs and profit margins. Geopolitical tensions and limited resource availability further exacerbate this challenge, making cost management a critical concern for manufacturers.

Battery Degradation and Safety Concerns

Lithium-based batteries are prone to degradation over time, leading to reduced capacity and performance. Additionally, safety concerns such as overheating and swelling pose risks to users and manufacturers alike. These challenges necessitate continuous innovation and compliance with stringent safety regulations, increasing operational complexity.

What are the key opportunities in the laptop battery industry?

Expansion in Emerging Markets

Emerging economies such as India, Brazil, and Southeast Asian countries present significant growth opportunities due to increasing laptop adoption and government-led digital initiatives. Companies that establish localized production and distribution networks can capitalize on cost advantages and rising demand in these regions.

Growth of the Aftermarket Replacement Segment

The growing installed base of laptops globally is driving demand for replacement batteries. With typical battery lifespans ranging between 2 and 4 years, the aftermarket segment offers recurring revenue opportunities. Online distribution channels are further enabling market expansion by improving accessibility and price transparency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14800 Million |

| Market Size in 2026 | USD 15791.60 Million |

| Market Size in 2031 | USD 21839.78 Million |

| CAGR | 6.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Battery Type Insights

Lithium-ion batteries continue to dominate the global laptop battery market, accounting for approximately 68% of total demand in 2025. This leadership position is primarily driven by their superior energy density, longer lifecycle, lightweight characteristics, and cost efficiency compared to alternative chemistries. The widespread adoption of lithium-ion batteries across consumer, enterprise, and gaming laptops has made them the industry standard, particularly as manufacturers prioritize performance optimization and extended battery life. Additionally, ongoing advancements in lithium-ion technology, such as fast-charging capabilities and improved thermal management, further reinforce their dominance.

Lithium-polymer batteries are increasingly gaining traction, particularly in premium ultrabooks and thin-and-light laptops. Their flexible form factor allows manufacturers to design slimmer and more compact devices, aligning with consumer preferences for portability and aesthetics. Meanwhile, nickel-based batteries, including NiMH and NiCd, have witnessed a sharp decline in adoption due to their lower energy efficiency, memory effect issues, and environmental concerns. Regulatory restrictions and the industry’s shift toward more sustainable and high-performance alternatives have rendered these technologies largely obsolete in modern laptop applications.

Capacity Insights

The 40–60 Wh battery segment leads the market with approximately 34% share in 2025, driven by its optimal balance between performance, cost, and size. This capacity range is widely used in mid-range consumer laptops and enterprise devices, which represent the bulk of global laptop shipments. The segment’s dominance is further supported by increasing demand from remote workers and students, who require reliable battery performance for everyday tasks without significantly increasing device cost.

The 60–80 Wh segment is emerging as the fastest-growing category, fueled by rising adoption of high-performance laptops, including business ultrabooks and gaming devices. These batteries provide extended usage time and support power-intensive applications, making them increasingly popular among professionals and gamers. Meanwhile, batteries above 80 Wh are primarily concentrated in gaming laptops and mobile workstations, where high computational requirements necessitate larger power reserves. However, their adoption is somewhat constrained by size, weight, and regulatory limitations on battery transport.

Distribution Channel Insights

OEM (Original Equipment Manufacturer) channels dominate the laptop battery market, accounting for over 62% of total market share in 2025. This dominance is attributed to the integrated nature of laptop batteries, which are installed during the manufacturing process. Strong partnerships between battery manufacturers and laptop OEMs ensure consistent demand, particularly as global laptop shipments remain robust across consumer and enterprise segments.

However, the aftermarket segment is witnessing steady growth, driven by the finite lifecycle of laptop batteries, typically ranging between 2–4 years. As the global installed base of laptops continues to expand, replacement demand is becoming a significant revenue stream. Online retail channels are playing a crucial role in this growth, offering a wide variety of compatible batteries at competitive prices, along with increased accessibility and convenience. The rise of e-commerce platforms and direct-to-consumer sales models is further accelerating the expansion of the aftermarket segment.

End-Use Insights

The corporate and enterprise segment leads the laptop battery market, contributing approximately 38% of total demand in 2025. This dominance is driven by large-scale procurement, frequent device upgrades, and the critical need for reliable battery performance to ensure uninterrupted productivity. Enterprises are increasingly investing in high-performance laptops equipped with long-lasting batteries to support hybrid work environments and mobile workforces.

The education sector is the fastest-growing end-use segment, supported by government-led digital learning initiatives, increasing adoption of e-learning platforms, and rising laptop penetration among students. Programs aimed at digital inclusion, particularly in emerging economies, are creating sustained demand for both OEM and replacement batteries. Additionally, the gaming industry is contributing significantly to market growth, as gaming laptops require high-capacity batteries to support intensive graphics and processing requirements. This segment is characterized by higher revenue per unit, further enhancing its impact on overall market value.

Form Factor Insights

Non-removable (integrated) batteries dominate the market, accounting for over 70% of the total share in 2025. This trend is primarily driven by the industry’s shift toward slim, lightweight, and aesthetically appealing laptop designs. Integrated batteries enable manufacturers to optimize internal space, improve structural rigidity, and enhance device performance, making them the preferred choice across most modern laptops.

Removable batteries, although declining in popularity, continue to maintain relevance in niche applications such as enterprise-grade and rugged laptops. These batteries offer the advantage of easy replacement and extended device usability, particularly in environments where continuous operation is critical. However, their share is expected to decline further as integrated designs become the standard across all major laptop categories.

Explore more data points, trends and opportunities Download Free Sample Report

Laptop Battery Market Segmentations

By Battery Type

- Lithium-Ion Batteries

- Lithium-Polymer Batteries

- Nickel Metal Hydride (NiMH) Batteries

- Nickel Cadmium (NiCd) Batteries

By Battery Capacity

- Below 40 Wh

- 40–60 Wh

- 60–80 Wh

- Above 80 Wh

By Distribution Channel

- OEM

- Aftermarket – Online Retail

- Aftermarket – Offline Retail & Service Centers

By End-Use Industry

- Personal Use

- Corporate & Enterprise

- Education Sector

- Gaming Industry

- IT & Software Services

By Form Factor

- Non-Removable (Integrated) Batteries

- Removable Batteries

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global laptop battery market, accounting for approximately 42% of the total market share in 2025. The region’s leadership is primarily driven by China, which serves as the world’s largest manufacturing hub for both laptops and batteries. Strong supply chain integration, availability of raw materials, and cost-efficient production capabilities provide a significant competitive advantage. India is emerging as the fastest-growing market, with a projected CAGR exceeding 8%, supported by government initiatives such as digitalization programs and local manufacturing incentives. Japan and South Korea contribute through technological innovation, particularly in advanced battery chemistries and premium product segments. Additionally, rising consumer demand, expanding IT infrastructure, and increasing exports of electronic devices further drive regional growth.

North America

North America holds approximately 25% of the global market share, with the United States as the primary contributor. The region’s growth is driven by high enterprise adoption of laptops, widespread implementation of remote and hybrid work models, and strong demand for premium and high-performance devices. Technological innovation and early adoption of advanced battery solutions, including fast-charging and energy-efficient technologies, further support market expansion. Additionally, the presence of major technology companies and significant investments in R&D contribute to sustained demand for high-quality battery solutions.

Europe

Europe accounts for around 20% of the global market, led by key countries such as Germany, the United Kingdom, and France. The region’s growth is strongly influenced by stringent environmental regulations and a strong focus on sustainability. Initiatives promoting battery recycling, reducing carbon emissions, and eco-friendly manufacturing processes are shaping market dynamics. Furthermore, increasing adoption of laptops in the enterprise and education sectors, coupled with government support for digital transformation, is driving demand. The emphasis on circular economy practices is also encouraging innovation in battery refurbishment and recycling.

Latin America

Latin America represents approximately 7% of the global market, with Brazil and Mexico as the leading contributors. The region’s growth is driven by increasing digital adoption, an expanding middle-class population, and improving economic conditions. Government initiatives aimed at enhancing digital infrastructure and education are boosting laptop penetration, thereby driving battery demand. Additionally, the growing popularity of remote work and online education is further supporting market expansion. However, dependence on imports and currency fluctuations remain key challenge in the region.

Middle East & Africa

The Middle East & Africa region holds around 6% market share, with the UAE and South Africa serving as key markets. Growth in this region is primarily driven by increasing investments in education, IT infrastructure, and smart city initiatives. Governments are actively promoting digital transformation, leading to higher adoption of laptops across the public and private sectors. Additionally, rising demand for consumer electronics and improving internet penetration are contributing to market growth. While the market remains relatively smaller compared to other regions, it presents significant long-term potential due to ongoing economic diversification and infrastructure development.

Key Players in the Laptop Battery Market

- Panasonic Corporation

- LG Energy Solution

- Samsung SDI

- BYD Company

- Sony Corporation

- Simplo Technology

- Dynapack International

- Celxpert Energy

- Desay Battery

- Sunwoda Electronic

- ATL (Amperex Technology Limited)

- EVE Energy

- Tianjin Lishen Battery

- Murata Manufacturing

- Coslight Technology