Laptop Stand Market Size

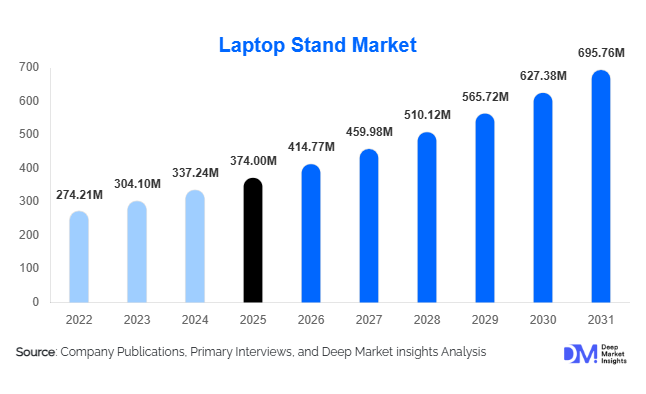

According to Deep Market Insights, the global laptop stand market size was valued at USD 374 million in 2025 and is projected to grow from USD 414.77 million in 2026 to reach USD 695.76 million by 2031, expanding at a CAGR of 10.9% during the forecast period (2026–2031). Market growth is primarily driven by the rapid adoption of hybrid work environments, increasing ergonomic awareness among professionals and students, and rising laptop penetration across education, corporate, and creative industries. Laptop stands are transitioning from optional accessories into essential workspace equipment as organizations prioritize employee wellness and productivity optimization. The shift toward mobile work lifestyles, digital learning ecosystems, and compact workstation setups continues to strengthen global demand.

Key Market Insights

- Hybrid and remote working models are significantly increasing adoption of ergonomic workspace accessories worldwide.

- Adjustable and foldable laptop stands dominate demand, driven by portability and ergonomic customization requirements.

- Asia-Pacific leads global consumption due to rising laptop ownership and expanding digital workforce populations.

- Online retail channels account for the majority of sales, supported by e-commerce expansion and direct-to-consumer brand strategies.

- Premium aluminum stands are gaining traction, reflecting consumer preference for durability and aesthetics.

- Integration of docking hubs, cooling systems, and smart workspace features is reshaping product innovation.

What are the latest trends in the laptop stand market?

Rise of Ergonomic Workstation Culture

Global workplace transformation has accelerated demand for ergonomic accessories, with laptop stands becoming a standard component of modern desk setups. Employers increasingly provide ergonomic allowances for remote employees, encouraging adoption of adjustable stands that improve posture and reduce musculoskeletal strain. Consumers are also investing in optimized home offices as work-from-home arrangements become permanent across many industries. Height-adjustable and multi-angle designs are particularly popular as users seek flexibility for long working hours and multi-device workflows.

Portable and Minimalist Design Innovation

Manufacturers are focusing on lightweight, foldable designs that support mobile productivity. Professionals working from cafés, co-working spaces, and travel locations prefer compact stands that can be easily transported. Minimalist aluminum constructions and ultra-thin collapsible designs are emerging as industry standards. Sustainability trends are also influencing design choices, with recyclable metals and bamboo materials gaining popularity among environmentally conscious buyers.

What are the key drivers in the laptop stand market?

Expansion of Hybrid Work and Digital Lifestyles

The global shift toward hybrid work remains the strongest growth driver. Organizations increasingly equip employees with ergonomic accessories to improve productivity and reduce workplace health risks. Rising freelance employment and digital entrepreneurship further support demand for portable workspace solutions. Laptop stands enhance viewing height and typing posture, making them essential for prolonged device usage across professional environments.

Growing Awareness of Ergonomics and Health Benefits

Increased awareness regarding posture-related injuries has encouraged consumers and enterprises to invest in ergonomic accessories. Occupational health recommendations and corporate wellness initiatives promote laptop elevation solutions that reduce neck and back strain. Educational institutions are also advising students to adopt ergonomic setups during extended online learning sessions, further strengthening adoption.

What are the restraints for the global market?

Price Commoditization in Entry-Level Products

The presence of numerous low-cost manufacturers has intensified price competition, particularly within economy product categories. Basic laptop stands are easy to manufacture, creating downward pressure on pricing and limiting profit margins for premium brands attempting differentiation.

Perception as Non-Essential Accessory in Developing Markets

In price-sensitive regions, consumers often prioritize laptops and primary electronics over accessories. Despite increasing awareness, adoption rates remain lower among first-time buyers who view laptop stands as optional purchases rather than productivity tools.

What are the key opportunities in the laptop stand industry?

Enterprise Ergonomic Procurement Programs

Corporations are integrating ergonomic equipment into workplace standards, creating large-scale procurement opportunities for manufacturers. Bulk purchasing agreements with enterprises and co-working operators provide stable revenue streams and long-term contracts. Vendors offering bundled workspace solutions can benefit significantly from institutional demand.

Smart and Multi-Functional Laptop Stands

Technology integration presents strong growth potential. Premium stands featuring USB hubs, cooling fans, wireless charging, and cable management solutions are gaining popularity among professionals and gamers. These multifunctional products allow manufacturers to move beyond commoditized pricing toward higher-margin offerings.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 374 Million |

| Market Size in 2026 | USD 414.77 Million |

| Market Size in 2031 | USD 695.76 Million |

| CAGR | 10.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global laptop stand market is primarily led by adjustable laptop stands, which account for approximately 38% of total demand. Their dominance is largely attributed to increasing ergonomic awareness and the growing prevalence of hybrid and remote work environments. Adjustable stands allow users to modify height and viewing angles, reducing neck strain and improving posture during prolonged device usage. As organizations and individuals prioritize workplace wellness and productivity optimization, demand for ergonomic accessories continues to rise, reinforcing the leadership of this segment. Additionally, compatibility with multiple device sizes and workspaces enhances their appeal across professional and personal applications.Foldable laptop stands are emerging as the fastest-growing product category, supported by rising mobility needs among students, digital nomads, and traveling professionals. Lightweight construction, compact storage capability, and ease of transport align with evolving work patterns that emphasize flexibility and multi-location productivity.

Cooling stands continue to maintain strong adoption among gaming enthusiasts, programmers, and creative professionals whose high-performance laptops generate substantial heat during intensive workloads. These stands enhance device longevity and maintain performance stability, making them essential for premium users.Fixed laptop stands retain relevance within entry-level price segments and institutional procurement where affordability and basic functionality remain key decision factors. Meanwhile, hybrid docking stands are gaining traction as premium workspace solutions that integrate connectivity ports, cable management, and organizational features. The increasing convergence of ergonomic accessories with productivity-enhancing hardware is expected to accelerate innovation and expand the value proposition of advanced product types over the forecast period.

Material Type Insights

Aluminum and metal alloy laptop stands dominate the material landscape, accounting for nearly 46% of global market share. Their leadership is driven by superior durability, structural stability, and efficient heat dissipation properties that enhance laptop performance during extended usage. The premium aesthetic appeal of metal finishes also aligns with modern workspace design trends, particularly among professionals and corporate buyers seeking long-lasting and visually refined accessories. As consumers increasingly associate workspace equipment with productivity and brand image, demand for high-quality materials continues to strengthen.Plastic and polymer-based stands remain widely adopted within price-sensitive markets due to affordability, lightweight construction, and manufacturing scalability.

These materials enable mass-market penetration, particularly in emerging economies and student-focused segments. Continuous advancements in reinforced polymers and recyclable plastics are further improving durability while maintaining cost advantages.Wooden and bamboo stands are gaining niche momentum, supported by rising environmental awareness and sustainable consumption trends. Eco-conscious consumers and minimalist workspace enthusiasts are increasingly choosing natural-material products that align with sustainability values and home-office aesthetics. Manufacturers are responding by introducing responsibly sourced materials and eco-friendly finishes, contributing to gradual expansion of this segment within premium and lifestyle-oriented categories.

Distribution Channel Insights

Online retail represents the dominant distribution channel, contributing more than 60% of global laptop stand sales. The rapid growth of e-commerce platforms has transformed purchasing behavior by enabling consumers to compare prices, evaluate product reviews, and access a wider range of international brands. Convenience, frequent promotional pricing, and efficient delivery networks have significantly accelerated online adoption, particularly among younger consumers and remote workers purchasing home-office accessories independently.Direct-to-consumer brand websites are expanding steadily as manufacturers focus on improving profit margins and strengthening customer relationships. Through proprietary platforms, companies can offer product customization, bundled accessories, and enhanced after-sales engagement while collecting valuable consumer insights.

This channel also supports brand differentiation in an increasingly competitive marketplace.Offline electronics and specialty retail stores continue to play an important role, particularly for enterprise procurement and bundled laptop accessory purchases. Corporate buyers and institutional customers often prefer physical demonstrations and bulk procurement agreements, sustaining demand through traditional retail channels. Additionally, in-store purchases remain relevant in regions where experiential buying and immediate product availability influence purchasing decisions.

End-Use Insights

Individual consumers constitute the largest end-use segment, accounting for nearly 48% of global market demand. Growth is primarily fueled by remote workers, students, freelancers, and content creators who increasingly invest in ergonomic home-office setups. The shift toward digital learning, flexible employment models, and extended screen time has amplified awareness of posture-related health concerns, driving consistent demand for laptop stands as essential productivity accessories.Corporate offices represent the fastest-growing end-use segment, supported by organizational initiatives aimed at improving employee wellness and workplace efficiency.

Companies are increasingly standardizing ergonomic workstation equipment as part of occupational health programs, particularly within hybrid work frameworks. Employer-sponsored home-office stipends and workspace upgrades are further accelerating adoption across enterprise environments.Educational institutions are emerging as significant buyers as digital classrooms, e-learning platforms, and laptop-based curricula expand globally. Schools and universities are investing in ergonomic infrastructure to support prolonged device usage among students. Meanwhile, gaming enthusiasts and creative professionals represent high-value users who favor adjustable and cooling-enabled premium stands designed to enhance performance, comfort, and device protection during intensive workflows.

Explore more data points, trends and opportunities Download Free Sample Report

Laptop Stand Market Segmentations

By Product Type

- Fixed (Non-Adjustable) Laptop Stands

- Adjustable Laptop Stands

- Foldable/Portable Laptop Stands

- Cooling Laptop Stands

- Docking/Hybrid Laptop Stands

By Material Type

- Aluminum & Metal Alloy Stands

- Plastic & Polymer Stands

- Wood & Bamboo Stands

- Composite/Hybrid Materials

By Distribution Channel

- Online Retail

- Offline Electronics Stores

- B2B/Enterprise Procurement

By End Use

- Individual Consumers

- Corporate Offices & Enterprises

- Education Institutions

- Gaming & Creative Professionals

- IT & Co-working Spaces

Regional Insights

North America

North America accounted for approximately 32% of global laptop stand demand in 2025, led primarily by the United States. Regional growth is strongly supported by widespread remote and hybrid work adoption, high disposable income levels, and strong awareness of ergonomic health standards. Organizations across the region frequently provide workspace stipends, encouraging employees to upgrade home-office equipment and driving replacement demand. Additionally, a mature e-commerce ecosystem and strong presence of premium accessory brands accelerate innovation and consumer adoption. The increasing prevalence of flexible employment models, freelancing culture, and technology-intensive professions continues to sustain long-term market expansion across North America.

Asia-Pacific

Asia-Pacific represents the largest regional market with approximately 35% share, supported by rapid digitalization and expanding laptop penetration across developing economies. China leads both manufacturing output and domestic consumption due to its large electronics ecosystem and strong online retail infrastructure. India is emerging as the fastest-growing market, driven by expanding IT services employment, startup ecosystem growth, and rising participation in digital education and remote work environments. Japan and South Korea contribute through high technology adoption rates, premium consumer preferences, and advanced workspace design trends. Increasing urbanization, rising middle-class income levels, and widespread adoption of mobile computing devices collectively act as major drivers for regional growth.

Europe

Europe demonstrates stable and consistent market growth supported by stringent workplace safety regulations and growing emphasis on employee well-being. Countries such as Germany, the United Kingdom, and France lead regional demand due to strong corporate adoption of ergonomic office standards. Sustainability trends also play a significant role, with consumers increasingly favoring eco-friendly materials such as recycled metals and bamboo-based designs. Government initiatives promoting flexible working arrangements and environmentally responsible manufacturing practices further support market expansion. The region’s mature professional workforce and design-focused consumer preferences continue to drive demand for premium and aesthetically refined laptop stand solutions.

Latin America

Latin America is experiencing gradual yet steady growth, particularly in Brazil and Mexico, where rising laptop ownership and expanding freelance and gig economy participation are increasing demand for productivity accessories. Improvements in internet penetration and logistics infrastructure have strengthened e-commerce accessibility, enabling wider product availability across urban and semi-urban areas. Growing adoption of remote education and cross-border digital employment opportunities also contributes to sustained demand growth. Price-sensitive consumers in the region favor affordable and portable product variants, encouraging manufacturers to introduce competitively priced offerings tailored to regional purchasing power.

Middle East & Africa

The Middle East & Africa laptop stand market is emerging steadily, led by the United Arab Emirates and Saudi Arabia. Regional growth is supported by national digital transformation initiatives, expansion of smart workplaces, and increasing investment in technology infrastructure. The rise of co-working spaces, entrepreneurship ecosystems, and remote work adoption is driving demand for ergonomic accessories among professionals and startups. In Africa, improving connectivity, expanding digital education programs, and increasing availability of affordable laptops are gradually strengthening accessory adoption. As awareness of ergonomic health benefits grows and online retail penetration expands, the region is expected to witness accelerating market development over the forecast period.

Key Players in the Laptop Stand Market

- Rain Design Inc.

- Twelve South LLC

- Nexstand Ltd.

- Roost Laptop Stand

- Ergotron Inc.

- Humanscale Corporation

- Logitech International S.A.

- Kensington Computer Products Group

- 3M Company

- Amazon Basics

- Nulaxy

- Boyata

- MOFT

- Soundance

- Avantree Corporation