Kitchen Tools & Accessories Market Size

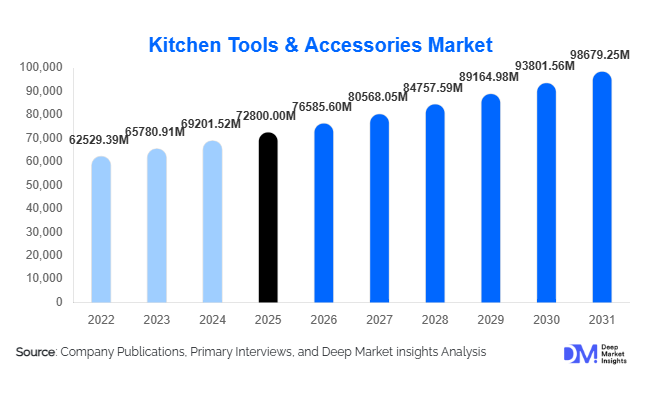

According to Deep Market Insights, the global kitchen tools & accessories market size was valued at USD 72,800 million in 2025 and is projected to grow from USD 76,585.60 million in 2026 to reach USD 98,679.25 million by 2031, expanding at a CAGR of 5.2% during the forecast period (2026–2031). The market growth is primarily driven by rising home cooking trends, rapid urbanization, expansion of organized retail, and increasing demand from commercial foodservice establishments. Consumers are prioritizing durable, ergonomic, and multifunctional kitchen tools, while premiumization trends in developed markets are further supporting revenue expansion.

Key Market Insights

- Food preparation tools account for nearly 34% of total market revenue, driven by consistent replacement cycles and universal usage across residential and commercial kitchens.

- Stainless steel dominates material consumption with over 41% share, supported by hygiene compliance and durability requirements.

- Asia-Pacific leads the global market with approximately 38% share in 2025, driven by China and India’s manufacturing and domestic demand base.

- Online retail channels contribute over 28% of global sales, supported by e-commerce penetration and direct-to-consumer strategies.

- Mid-range products represent the largest pricing segment (46%), balancing affordability and quality for emerging markets.

- The top five manufacturers collectively account for nearly 32% of the global market, indicating moderate fragmentation and strong regional competition.

What are the latest trends in the kitchen tools & accessories market?

Smart & Connected Kitchen Integration

The adoption of IoT-enabled kitchen accessories such as digital thermometers, smart weighing scales, and app-connected measuring tools is gaining traction. Consumers increasingly prefer precision cooking supported by real-time monitoring and mobile connectivity. Smart kitchen accessories are particularly popular in North America and Europe, where smart home ecosystems are expanding. Brands are integrating Bluetooth-enabled temperature sensors and AI-based cooking guidance tools to enhance user convenience and reduce food waste.

Sustainability and Eco-Friendly Materials

Growing environmental awareness has accelerated demand for bamboo, recycled plastics, and reusable stainless-steel products. Governments in Europe and North America are enforcing regulations on single-use plastics, encouraging manufacturers to redesign product lines with biodegradable or recyclable materials. Eco-label certifications and carbon-neutral manufacturing practices are becoming key differentiators in premium markets. Sustainable packaging and minimal-waste production methods are also influencing procurement decisions in institutional and hospitality sectors.

What are the key drivers in the kitchen tools & accessories market?

Growth in Home Cooking and Culinary Content

The rise of cooking shows, digital recipe platforms, and social media food influencers has significantly boosted demand for specialty kitchen tools. Consumers are investing in high-quality knives, baking accessories, and ergonomic utensils to replicate professional culinary standards at home. The residential segment accounts for nearly 68% of total demand, supported by housing expansion and kitchen remodeling activities.

Expansion of the Commercial Foodservice Industry

The global foodservice industry, valued at over USD 4 trillion, continues to expand, driving institutional procurement of kitchen tools. Quick-service restaurants (QSRs), cloud kitchens, and hotel chains require bulk purchases of standardized accessories, supporting steady demand. Recovery in global travel and hospitality has further accelerated procurement cycles in 2023–2025.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in stainless steel, aluminum, and polymer prices directly affect production costs. Manufacturers often face margin compression during commodity price spikes, particularly in price-sensitive regions. Profit margins typically range between 8–18%, depending on the pricing segment and regional competition.

Intense Price Competition from Low-Cost Manufacturers

High competition from low-cost Asian manufacturers creates pricing pressure globally. This restricts premium pricing strategies in developing markets and compels established brands to invest heavily in product differentiation and branding.

What are the key opportunities in the kitchen tools & accessories industry?

Emerging Market Expansion

Rapid urbanization in India, Indonesia, Vietnam, and Brazil presents significant growth opportunities. Rising middle-class populations and government-led manufacturing initiatives such as “Make in India” are encouraging domestic production and local consumption. Establishing regional manufacturing hubs can reduce logistics costs and improve competitiveness.

Premiumization and Design Innovation

Consumers in North America and Europe increasingly prefer premium, aesthetically appealing kitchen tools with ergonomic designs. High-end knife sets, silicone baking tools, and modular storage solutions command higher margins. Brands that combine design innovation with sustainability credentials are likely to capture greater market share.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 72800 Million |

| Market Size in 2026 | USD 76585.60 Million |

| Market Size in 2031 | USD 98679.25 Million |

| CAGR | 5.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Food preparation tools dominate the global kitchen tools & accessories market with a 34% revenue share in 2025, making them the leading product category. This segment includes knives, peelers, graters, choppers, mandolins, and measuring tools, products that are fundamental to daily cooking across residential, commercial, and institutional kitchens. The primary driver for this segment’s leadership is its high replacement frequency compared to other categories. Knives and cutting tools require periodic upgrading due to wear and tear, while evolving culinary trends and professional-style home cooking continue to stimulate premium knife set purchases. Growth in cooking tutorials, food blogging, and chef-inspired home kitchens has further strengthened demand for specialized preparation tools.

Cooking and baking tools account for approximately 26% of the market, supported by the sustained rise in home baking, café culture, and dessert-focused QSR chains globally. The surge in demand for silicone baking molds, whisks, spatulas, and thermometers reflects increasing consumer experimentation with global cuisines. Storage and organization accessories contribute around 22%, driven by urban apartment living, modular kitchen installations, and consumer preference for decluttered spaces. Cleaning and maintenance tools represent 12% share, supported by hygiene awareness and food safety compliance in commercial kitchens. Meanwhile, smart and innovative kitchen accessories hold 6% share but are expanding at over 8% CAGR, fueled by IoT integration, precision cooking demand, and smart home ecosystem compatibility.

Material Insights

Stainless steel leads the material segment with a 41% market share, primarily due to its durability, corrosion resistance, and compliance with global food safety standards. Commercial kitchens, in particular, mandate stainless steel tools because of hygiene regulations and ease of sterilization. Its recyclability also aligns with sustainability goals, strengthening its dominance in both developed and emerging markets.

Plastic accounts for approximately 28% of the market, largely within economy and mass-market segments where affordability is a key purchasing factor. However, regulatory pressure on single-use plastics in Europe and North America is influencing manufacturers to shift toward BPA-free and recyclable polymers. Silicone, with around 12% share, is gaining popularity due to heat resistance, flexibility, and suitability for non-stick cookware. Wood and bamboo represent 10% of market revenue, benefiting from eco-conscious consumer trends and aesthetic appeal in premium kitchens. Aluminum and composite materials collectively account for 9%, mainly used in lightweight and specialty applications.

Distribution Channel Insights

Hypermarkets and supermarkets dominate with a 32% share in 2025, supported by strong consumer preference for physical product inspection before purchase. In-store promotions, bundled discounts, and impulse buying behavior significantly contribute to this segment’s leadership. Large retail chains also offer private-label kitchenware, intensifying competition and improving affordability.

Online retail channels account for approximately 28% of global sales and are the fastest-growing distribution segment. E-commerce platforms provide product comparison, customer reviews, and direct-to-consumer (D2C) brand engagement, which appeal particularly to younger demographics. Specialty kitchenware stores contribute 22%, catering to premium and professional-grade product buyers. Institutional and B2B sales represent 18%, driven by procurement contracts from hotels, hospitals, cloud kitchens, and educational institutions.

End-Use Insights

Residential households represent the largest end-use segment with 68% share, primarily driven by global housing growth, kitchen renovations, and increased home-cooking frequency. Urbanization, rising disposable incomes, and smaller household units have encouraged modular kitchen adoption and compact storage solutions.

The commercial foodservice segment contributes 24% of total revenue and is growing at nearly 6% CAGR. Expansion of QSR chains, cloud kitchens, catering services, and international hotel brands is driving bulk procurement of standardized kitchen tools. Institutional kitchens account for 8%, supported by government investments in healthcare infrastructure, schools, and corporate cafeterias, particularly in Asia-Pacific and the Middle East. Growing public infrastructure spending in these regions further supports long-term institutional demand.

Explore more data points, trends and opportunities Download Free Sample Report

Kitchen Tools & Accessories Market Segmentations

By Product Type

- Food Preparation Tools

- Cooking & Baking Tools

- Storage & Organization Accessories

- Cleaning & Maintenance Tools

- Smart & Innovative Kitchen Accessories

By Material

- Stainless Steel

- Plastic

- Silicone

- Wood & Bamboo

- Aluminum & Composite Materials

By Distribution Channel

- Hypermarkets & Supermarkets

- Online Retail (E-commerce & D2C)

- Specialty Kitchenware Stores

- Institutional & B2B Sales

By End-Use

- Residential Households

- Commercial Foodservice

- Institutional Kitchens

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with a 38% share in 2025, driven by large population bases, strong domestic manufacturing, and rising middle-class consumption. China alone contributes nearly 18% of global revenue, supported by export dominance and extensive production capacity. Government-backed industrial initiatives and integrated supply chains strengthen China’s cost competitiveness globally. India is the fastest-growing major market in the region, expanding at over 7% CAGR due to rapid urban housing construction, rising disposable incomes, and expanding organized retail networks. Japan and South Korea represent mature markets characterized by high product innovation, compact kitchen solutions, and premium stainless-steel adoption.

North America

North America accounts for approximately 26% of global revenue, with the United States contributing nearly 22%. Regional growth is driven by high per capita kitchenware spending, strong home renovation activity, and widespread adoption of premium and smart kitchen tools. Consumer preference for ergonomic design, branded products, and sustainable materials further accelerates value growth. Canada shows stable expansion supported by residential remodeling trends and growing interest in eco-friendly kitchenware.

Europe

Europe holds around 22% market share, led by Germany, France, the UK, and Italy. The region’s growth is driven by strict environmental regulations, high consumer preference for sustainable and high-quality materials, and strong culinary traditions. Premiumization is particularly strong in Western Europe, where consumers favor durable stainless steel and eco-certified wooden accessories. Eastern Europe is witnessing gradual growth supported by retail expansion and rising household incomes.

Latin America

Latin America represents approximately 6% of the global market, with Brazil and Mexico leading regional demand. Growth is primarily supported by expanding supermarket chains, urban middle-class expansion, and increasing participation of women in the workforce, which drives demand for convenient kitchen solutions. Import dependency remains high, particularly for premium products, making currency fluctuations a key influencing factor.

Middle East & Africa

The Middle East & Africa region accounts for roughly 8% of global revenue. The UAE and Saudi Arabia are major growth hubs, supported by hospitality sector investments, tourism-driven foodservice expansion, and rising disposable incomes. Large-scale infrastructure projects and hotel developments linked to economic diversification programs are stimulating commercial kitchen demand. In Africa, South Africa leads consumption, supported by urban retail growth and the gradual expansion of organized foodservice chains.

Key Players in the Kitchen Tools & Accessories Market

- Groupe SEB

- Newell Brands

- ZWILLING J.A. Henckels

- OXO

- Victorinox

- Fiskars Group

- Cuisinart

- KitchenAid

- Tupperware Brands

- Tramontina

- ARCOS

- Kyocera Corporation

- Bradshaw Home

- Joseph Joseph

- Shibazi