Kitchen Knife Market Size

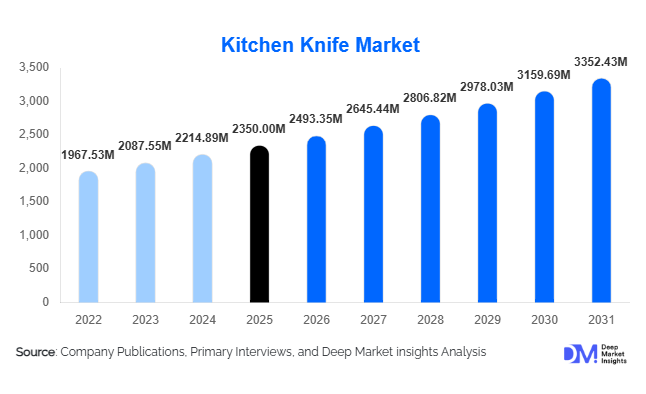

According to Deep Market Insights, the global kitchen knife market size was valued at approximately USD 2,350 million in 2025 and is projected to grow from USD 2,493.35 million in 2026 to reach nearly USD 3,352.43 million by 2031, expanding at a CAGR of 6.1% during the forecast period (2026–2031). The kitchen knife market growth is primarily driven by rising consumer interest in home cooking, rapid expansion of the global foodservice industry, increasing demand for premium culinary tools, and growing penetration of e-commerce platforms enabling global accessibility of branded kitchenware products.

Key Market Insights

- Premiumization is accelerating globally, with rising demand for high-carbon steel, Damascus steel, and ergonomically designed knives.

- Foodservice industry expansion is a core demand driver, particularly from restaurants, hotels, cloud kitchens, and catering services.

- Asia-Pacific dominates production and consumption growth, led by China, Japan, and India.

- E-commerce is transforming distribution dynamics, enabling direct-to-consumer sales and global brand penetration.

- Residential usage remains the dominant application, driven by increasing interest in gourmet cooking and kitchen aesthetics.

- Sustainability and material innovation are emerging trends, including recycled steel blades and eco-friendly packaging solutions.

What are the latest trends in the kitchen knife market?

Premium Craftsmanship and Material Innovation

The kitchen knife market is witnessing a strong shift toward premium and artisanal products. Consumers are increasingly opting for handcrafted knives made from Damascus steel, high-carbon stainless steel, and titanium-based alloys. Manufacturers are focusing on improving blade sharpness retention, corrosion resistance, and ergonomic handle designs. This trend is especially prominent in North America and Europe, where consumers are willing to pay premium prices for durability, aesthetics, and performance. Branding and storytelling around craftsmanship are becoming key differentiators in the market.

E-Commerce and Direct-to-Consumer Expansion

Digital transformation is reshaping how kitchen knives are marketed and sold. Online platforms and D2C websites are enabling manufacturers to bypass traditional retail channels and reach global consumers directly. Influencer marketing, product demonstrations, and culinary content on social media are significantly influencing purchase decisions. Subscription-based sharpening services and bundled knife sets are also gaining traction, creating recurring revenue opportunities for brands. This trend is particularly strong among mid-range and premium knife segments.

What are the key drivers in the kitchen knife market?

Growth of the Global Foodservice Industry

The expansion of restaurants, hotels, cloud kitchens, and catering services is a major driver of the kitchen knife market. Professional kitchens require high-performance, durable knives for efficiency and precision, leading to bulk procurement from commercial buyers. The rise of quick-service restaurants and premium dining establishments is further accelerating demand for specialized knife types such as boning, carving, and chef’s knives.

Rising Home Cooking and Culinary Awareness

Increasing interest in home cooking, driven by digital cooking platforms, social media content, and lifestyle changes, has significantly boosted residential demand. Consumers are investing in better kitchen tools to replicate restaurant-style cooking at home. This shift is particularly strong in urban households across Asia-Pacific and North America, where cooking is increasingly seen as a lifestyle activity rather than a necessity.

Product Innovation and Premiumization

Manufacturers are introducing technologically advanced knives with improved balance, sharper blades, antimicrobial coatings, and ergonomic designs. These innovations enhance user experience and justify higher price points, contributing to overall market expansion. Premium branding and design aesthetics are also influencing consumer purchasing behavior.

What are the restraints for the global market?

Price Sensitivity in Developing Markets

In emerging economies, consumers often prefer low-cost alternatives, limiting the penetration of premium and branded kitchen knives. This restricts revenue growth for high-end manufacturers and creates intense price competition in the entry-level segment.

Raw Material Price Volatility

Fluctuations in steel and alloy prices significantly impact manufacturing costs and profit margins. Smaller manufacturers are particularly affected, as they lack strong hedging mechanisms or economies of scale, leading to pricing instability across the market.

What are the key opportunities in the kitchen knife industry?

Expansion in Emerging Markets

Rapid urbanization and rising disposable incomes in Asia-Pacific, Latin America, and parts of Africa are creating strong demand for modern kitchen tools. Increasing exposure to global cuisines is encouraging consumers to upgrade from basic utensils to premium kitchen knives. Government-led manufacturing initiatives in countries like India and China are also strengthening domestic production capabilities.

Smart and Sustainable Kitchenware Innovation

There is a growing opportunity in integrating sustainability and technology into kitchen knives. Eco-friendly materials, recyclable packaging, and smart storage solutions are gaining traction. Innovations such as antimicrobial coatings and precision-engineered blades offer differentiation in an increasingly competitive market, especially in developed economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2350 Million |

| Market Size in 2026 | USD 2493.35 Million |

| Market Size in 2031 | USD 3352.43 Million |

| CAGR | 6.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chef’s knives continue to dominate the global kitchen knife market, accounting for approximately 28% share in 2025, primarily due to their multifunctionality and widespread usage across both residential and commercial kitchens. Their ability to perform a wide range of cutting, slicing, and chopping tasks makes them the most preferred knife type among both professional chefs and home cooks. This dominance is further supported by increasing culinary awareness and the growing popularity of cooking as a lifestyle activity. Paring and utility knives follow closely, driven by their precision in handling smaller, detailed tasks such as peeling and trimming, making them indispensable in household kitchens. Bread and carving knives maintain stable demand due to their essential role in bakery and meat preparation, particularly in commercial foodservice environments. Meanwhile, specialty knives such as sushi, fillet, and cheese knives are witnessing strong growth in premium segments, supported by rising global exposure to diverse cuisines. Cleavers remain highly significant in Asia-Pacific markets, especially in China and Southeast Asia, where traditional cooking methods require heavy-duty cutting tools for meat and vegetables, reinforcing their regional dominance.

Application Insights

The residential segment leads the market with approximately 65% share, driven by increasing home cooking trends, rising disposable incomes, and growing consumer interest in kitchen aesthetics and functionality. The surge in digital cooking content, including social media and online tutorials, has encouraged consumers to invest in high-quality kitchen tools, particularly in urban households. The commercial segment is expanding steadily, supported by the global growth of restaurants, hotels, cloud kitchens, and catering services. This segment benefits from bulk purchasing requirements and the need for durable, high-performance knives in professional kitchens. Institutional kitchens, including schools, hospitals, and corporate cafeterias, provide consistent baseline demand due to their operational scale and regular usage requirements. Additionally, emerging applications in culinary institutes, food processing training centers, and hospitality education are contributing to incremental demand, as these institutions require standardized and specialized knife sets for training purposes.

Distribution Channel Insights

Offline retail channels continue to dominate the market, accounting for nearly 60% market share, primarily because consumers prefer to physically evaluate factors such as grip, weight, and blade quality before purchase. Supermarkets, specialty kitchen stores, and department stores remain key sales points, especially for mid-range and premium products. However, online retail is rapidly gaining momentum, driven by increasing internet penetration, convenience, and wider product availability. E-commerce platforms enable consumers to compare products, access reviews, and explore global brands, significantly influencing purchasing decisions. Direct-to-consumer (D2C) models are becoming increasingly important, allowing manufacturers to build stronger brand relationships and improve margins. Subscription-based services such as knife sharpening, maintenance kits, and bundled product offerings are also emerging as value-added services. Additionally, influencer marketing and social commerce are playing a critical role in shaping consumer preferences, particularly among younger demographics.

Consumer Type Insights

Commercial buyers, including restaurants, hotels, and catering companies, represent a substantial portion of demand due to bulk procurement and frequent replacement cycles. These buyers prioritize durability, performance, and cost-efficiency, often establishing long-term supplier relationships. Individual consumers dominate the residential segment, with increasing preference for mid-range and premium knives as disposable incomes rise. Professional chefs form a niche but high-value segment, demanding precision-engineered knives with superior balance, sharpness, and longevity. Meanwhile, hobbyist cooks and culinary enthusiasts are emerging as one of the fastest-growing consumer groups, driven by increased exposure to global cuisines and cooking content. This segment is particularly influential in driving premium product adoption and brand engagement through online platforms.

Age Group Insights

The 31–50 age group represents the largest consumer base, supported by higher disposable income levels and a strong inclination toward lifestyle upgrades, including modern kitchen tools. This segment often invests in mid-range to premium knives, balancing quality and value. The 18–30 age group is a key growth driver, particularly in online retail channels, as younger consumers are influenced by digital content and tend to experiment with cooking. They primarily drive demand for affordable and mid-range products. The 51–65 age group contributes significantly to the premium segment, preferring durable, ergonomically designed knives that offer comfort and longevity. Consumers above 65 years represent a niche segment, with demand focused on safety-oriented and easy-to-handle kitchen tools, highlighting the importance of ergonomic innovation in product design.

Explore more data points, trends and opportunities Download Free Sample Report

Kitchen Knife Market Segmentations

By Product Type

- Chef’s Knives

- Paring Knives

- Utility Knives

- Bread Knives

- Santoku Knives

- Carving & Slicing Knives

- Boning Knives

- Cleavers

- Specialty Knives

By Blade Material

- Stainless Steel

- High Carbon Steel

- Damascus Steel

- Ceramic Blades

- Titanium & Hybrid Alloys

By Price Range

- Economy (Below USD 20)

- Mid-Range (USD 20–100)

- Premium (Above USD 100)

By Application

- Residential / Household Use

- Commercial Restaurants

- Hotels & Hospitality

- Catering Services

- Institutional Kitchens

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Kitchen Stores

- Department Stores

Regional Insights

North America

North America accounts for approximately 28% of the global kitchen knife market, with the United States being the largest contributor, followed by Canada. Growth in this region is primarily driven by high consumer purchasing power, a well-established foodservice industry, and strong adoption of premium kitchen tools. The increasing popularity of home cooking, supported by culinary shows and digital content, is significantly boosting residential demand. Additionally, the presence of professional culinary institutes and a large base of professional chefs contributes to sustained demand for high-performance knives. The trend toward premiumization and branded products further strengthens market growth in this region.

Europe

Europe holds around 26% market share, led by Germany, the United Kingdom, and France. The region benefits from a strong heritage of craftsmanship and high-quality knife manufacturing, particularly in Germany. Growth drivers include increasing demand for premium and sustainable products, as well as a well-established culinary culture that values precision tools. Rising environmental awareness is also pushing manufacturers toward eco-friendly materials and production processes. Additionally, Europe’s strong export capabilities support global market expansion, making it a key hub for high-end knife production.

Asia-Pacific

Asia-Pacific dominates the market with approximately 32% share and is also the fastest-growing region. China leads in large-scale manufacturing and exports, while Japan is globally recognized for its premium, handcrafted knives. India is emerging as a high-growth market due to rapid urbanization, rising disposable incomes, and changing food habits. Key growth drivers include expanding middle-class populations, increasing adoption of modern kitchen tools, and strong demand from both residential and commercial sectors. Additionally, traditional cooking practices in countries like China and Southeast Asia continue to drive demand for specific knife types such as cleavers.

Latin America

Latin America accounts for approximately 7% of the global market, with Brazil and Mexico as key contributors. Growth in this region is driven by the expansion of the foodservice industry, increasing urbanization, and rising exposure to international cuisines. The growing middle class is gradually shifting toward better-quality kitchen tools, although price sensitivity remains a limiting factor. Retail expansion and improving e-commerce penetration are also supporting market development.

Middle East & Africa

The Middle East & Africa region holds around 7% market share, with significant demand from countries such as the UAE, Saudi Arabia, and South Africa. Growth is primarily driven by the rapid expansion of the hospitality and tourism sectors, particularly in the Gulf countries, where luxury hotels and restaurants are increasing procurement of premium kitchen tools. Infrastructure development and rising investments in the foodservice industry are further supporting demand. In Africa, gradual urbanization and improving retail networks are contributing to steady market growth, although economic constraints in certain regions may limit rapid expansion.

Key Players in the Kitchen Knife Market

- Victorinox

- Zwilling J.A. Henckels

- Wüsthof

- Global Knives (Yoshikin)

- KAI Corporation (Shun)

- Fiskars Group

- Mercer Culinary

- Cangshan Cutlery

- Dalstrong

- Tramontina

- MAC Knife

- Tojiro

- Robert Welch

- BergHOFF

- Sabatier