Kitchen Furniture and Fixture Market Size

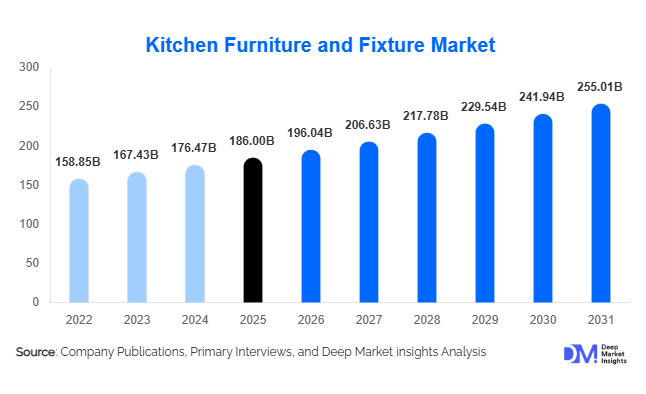

According to Deep Market Insights, the global kitchen furniture and fixture market size was valued at USD 186 billion in 2025 and is projected to grow from USD 196.04 billion in 2026 to reach USD 255.01 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The kitchen furniture and fixture market growth is primarily driven by rapid urbanization, increasing residential construction, and rising consumer investment in modular kitchen solutions and premium home interiors.

Kitchen furniture and fixtures, including cabinets, countertops, islands, sinks, storage systems, and lighting, are essential components of modern residential and commercial kitchen environments. The market has evolved significantly as kitchens have transformed from purely functional spaces into central lifestyle areas within homes. Consumers increasingly seek aesthetically appealing, ergonomic, and technologically integrated kitchen designs that enhance convenience and maximize storage efficiency.

The growing popularity of modular kitchens, smart storage systems, and durable countertop materials such as quartz and engineered stone is reshaping demand patterns across global markets. In developed regions, such as North America and Europe, kitchen renovation and remodeling projects account for a substantial share of demand, while emerging economies across the Asia-Pacific are witnessing a rise in the installation of modular kitchen furniture in new residential developments. Additionally, the expansion of the hospitality and food service sectors is increasing the adoption of durable kitchen fixtures designed for high-usage environments.

Key Market Insights

- Kitchen cabinets represent the largest product segment, accounting for approximately 42% of the global market due to their central role in kitchen storage and layout design.

- Modular kitchens are rapidly replacing traditional kitchen layouts, driven by demand for space optimization, customization, and faster installation in urban housing developments.

- North America dominates the global market, supported by strong residential remodeling activity and high consumer spending on home improvement.

- Asia-Pacific is the fastest-growing region, driven by expanding middle-class populations and large-scale housing construction in China and India.

- Engineered wood materials lead the material segment, representing nearly 46% of the market due to cost efficiency and design flexibility.

- Technological innovation is transforming kitchen fixtures, with smart faucets, integrated lighting, and automated storage systems gaining traction globally.

What are the latest trends in the kitchen furniture and fixture market?

Growing Demand for Modular and Customized Kitchens

The shift toward modular kitchen systems is one of the most prominent trends in the kitchen furniture and fixture market. Urban housing developments often feature limited kitchen space, prompting homeowners to adopt modular designs that maximize storage efficiency and allow flexible configurations. Modular kitchens offer faster installation, standardized components, and customization options that appeal to both homeowners and property developers. Manufacturers are increasingly offering design configurators and modular cabinet systems that can be tailored to different layouts, finishes, and materials. This trend is particularly prominent in rapidly urbanizing markets such as India, China, and Southeast Asia, where apartment living is expanding rapidly.

Adoption of Smart and Technology-Enabled Fixtures

Technological integration is transforming modern kitchen environments. Smart faucets with touchless operation, motion-sensor lighting integrated into cabinets, and automated storage solutions are becoming popular features in premium kitchens. Smart kitchen fixtures are often connected to home automation systems, allowing users to control lighting, appliances, and water usage through mobile applications. Manufacturers are investing in research and development to incorporate advanced features such as LED-integrated cabinetry, voice-activated faucets, and intelligent storage mechanisms that enhance convenience and efficiency. These innovations are particularly appealing to tech-savvy consumers and homeowners adopting smart home ecosystems.

What are the key drivers in the kitchen furniture and fixture market?

Rapid Growth in Residential Construction

Residential construction growth remains a primary driver of the kitchen furniture and fixture market. Governments and private developers worldwide are investing heavily in housing infrastructure to accommodate urban population growth. Each new residential unit requires kitchen installations including cabinets, countertops, sinks, and storage systems, creating substantial demand for kitchen furniture manufacturers. Emerging markets across Asia and the Middle East are witnessing significant housing development projects, while developed economies continue to experience strong demand through renovation and remodeling activities.

Rising Consumer Spending on Home Interiors

Consumers are increasingly prioritizing interior aesthetics and functionality when designing living spaces. Kitchens have evolved into central gathering spaces where families socialize and entertain guests, leading to higher investments in premium furniture and fixtures. Materials such as quartz countertops, designer cabinetry, and high-quality lighting systems are becoming more popular as consumers seek visually appealing and durable kitchen environments. Growing disposable income levels in emerging economies further support increased spending on modern kitchen installations.

What are the restraints for the global market?

Volatility in Raw Material Prices

The kitchen furniture and fixture industry relies heavily on raw materials such as timber, engineered wood panels, stainless steel, and natural stone. Fluctuations in the prices of these materials can significantly impact manufacturing costs and profit margins. Rising timber prices and supply chain disruptions in metal markets can increase production costs for cabinets, countertops, and fixtures, ultimately affecting product pricing and demand in price-sensitive markets.

High Cost of Premium Kitchen Installations

Although demand for luxury kitchen solutions is increasing, the high cost of premium cabinets, stone countertops, and technologically advanced fixtures can limit widespread adoption. Premium kitchen installations can cost significantly more than standard kitchen setups, making them accessible mainly to higher-income consumers. This cost barrier is particularly noticeable in developing markets where affordability remains a critical factor influencing purchasing decisions.

What are the key opportunities in the kitchen furniture and fixture industry?

Expansion of Modular Kitchen Adoption in Emerging Economies

Emerging economies present significant growth opportunities for kitchen furniture manufacturers as modular kitchens gain popularity among urban consumers. Countries such as India, Indonesia, Vietnam, and Brazil are witnessing a rapid expansion of apartment housing, creating strong demand for modular cabinet systems and space-efficient storage solutions. Localized manufacturing and cost-optimized modular designs can help companies capture market share in these rapidly expanding regions.

Growth in Kitchen Renovation and Remodeling Projects

Home renovation and remodeling projects are becoming a major growth driver, particularly in mature housing markets. Homeowners frequently upgrade kitchens to enhance property value and improve functionality. Kitchen remodeling often involves replacing cabinets, countertops, lighting fixtures, and storage systems with modern alternatives. Manufacturers offering retrofit-friendly designs and customizable modular components are well-positioned to benefit from this expanding renovation market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 186 Billion |

| Market Size in 2026 | USD 196.04 Billion |

| Market Size in 2031 | USD 255.01 Billion |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Kitchen cabinets dominate the kitchen furniture and fixture market, accounting for approximately 42% of total revenue in 2025. Cabinets serve as the primary storage and structural component of kitchen layouts, making them essential in both new installations and renovation projects. Countertops represent another significant segment, driven by rising adoption of durable materials such as quartz and engineered stone. Kitchen islands and breakfast counters are gaining popularity as homeowners embrace open-plan kitchen designs that integrate dining and social spaces. Storage systems, including pull-out drawers and modular pantry solutions, are also experiencing rapid adoption due to their ability to maximize kitchen efficiency. Lighting fixtures integrated into cabinets and countertops are becoming increasingly popular as consumers seek both functional illumination and aesthetic appeal.

Application Insights

The residential sector represents the largest application segment for kitchen furniture and fixtures, accounting for nearly 72% of global demand. Residential installations include both new housing construction and renovation projects, which frequently involve upgrading cabinets, countertops, and fixtures to modern standards. The commercial segment, including restaurants, hotels, and institutional kitchens, also contributes significantly to market demand. These environments require durable fixtures designed for intensive usage, including stainless steel countertops and heavy-duty storage systems. Growth in the global hospitality and food service industries is expected to further increase demand for commercial kitchen furniture installations.

Distribution Channel Insights

Specialty kitchen showrooms remain the dominant distribution channel, accounting for nearly 37% of total sales. Consumers often prefer visiting showrooms to evaluate materials, finishes, and design options before making purchasing decisions. Furniture retail chains and home improvement stores also play an important role in distribution, offering a wide range of kitchen furniture products to mainstream consumers. E-commerce platforms are gaining popularity as manufacturers introduce digital kitchen design tools and online configurators that allow customers to visualize layouts and customize products before purchasing. Direct sales to real estate developers and construction companies represent another major channel, particularly for large residential projects.

Explore more data points, trends and opportunities Download Free Sample Report

Kitchen Furniture and Fixture Market Segmentations

By Product Type

- Kitchen Cabinets

- Countertops

- Kitchen Islands & Breakfast Counters

- Kitchen Storage Systems

- Kitchen Sinks & Faucets

- Kitchen Lighting Fixtures

By Material Type

- Solid Wood

- Engineered Wood

- Metal

- Stone & Engineered Stone

- Glass & Composite Materials

By Application

- Residential Kitchens

- Commercial Kitchens

- Hospitality Kitchens

- Institutional Kitchens

By Distribution Channel

- Specialty Kitchen Showrooms

- Home Improvement Retail Chains

- Furniture Retail Stores

- Online/E-commerce Platforms

- Direct Sales to Builders & Real Estate Developers

Regional Insights

North America

North America holds the largest share of the global kitchen furniture and fixture market, accounting for approximately 34% of total revenue in 2025. The United States is the primary contributor due to its strong home renovation and remodeling industry. Homeowners frequently upgrade kitchen interiors to improve property value and functionality. Canada also represents a growing market, supported by expanding residential construction and rising demand for modular kitchen installations.

Europe

Europe accounts for nearly 28% of the global market, with Germany, Italy, the United Kingdom, and France leading regional demand. European consumers prioritize high-quality materials, innovative kitchen designs, and sustainable furniture production. Germany and Italy are also major manufacturing hubs for kitchen furniture exports, supplying premium cabinetry and fixtures to international markets.

Asia-Pacific

Asia-Pacific represents approximately 30% of the global market and is the fastest-growing region. Rapid urbanization, rising disposable incomes, and expanding housing construction in countries such as China, India, Japan, and South Korea are driving strong demand for modular kitchens and modern fixtures. China serves as both a major consumer and exporter of kitchen furniture, while India is witnessing the rapid adoption of modular kitchen solutions in urban housing developments.

Latin America

Latin America accounts for nearly 8% of the global kitchen furniture and fixture market. Brazil and Mexico lead regional demand due to expanding residential construction and rising consumer spending on home interiors. Growing middle-class populations are increasing the adoption of modular kitchen systems across the region.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth driven by rapid infrastructure development and luxury residential projects in countries such as the UAE and Saudi Arabia. High-end residential developments and hospitality projects in Gulf countries frequently feature premium kitchen furniture installations. Increasing urbanization across African economies is also gradually expanding demand for modern kitchen fixtures.

Key Players in the Kitchen Furniture and Fixture Market

- IKEA

- Nobia AB

- Howdens Joinery

- Nobilia

- American Woodmark Corporation

- Masco Corporation

- Häcker Küchen

- SieMatic Möbelwerke

- Poggenpohl

- Snaidero

- Scavolini

- Leicht Küchen

- Oppein Home Group

- Pedini

- Bulthaup