Kitchen Canisters Market Size

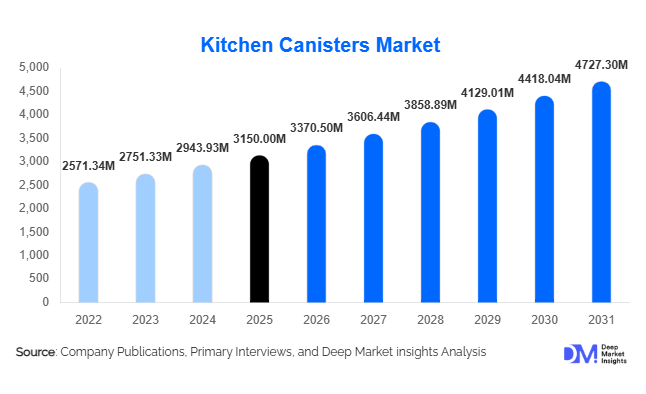

According to Deep Market Insights, the global kitchen canisters market size was valued at USD 2,940 million in 2025 and is projected to grow from USD 3,370.50 million in 2026 to reach USD 4,727.30 million by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). Market growth is primarily driven by increasing consumer focus on organized kitchen spaces, rising adoption of modular kitchens, and growing demand for airtight food storage solutions that enhance food preservation and hygiene. The expansion of e-commerce retail, combined with evolving lifestyle trends emphasizing home cooking and pantry organization, is further accelerating global demand for kitchen canisters across residential and commercial applications.

Key Market Insights

- Glass kitchen canisters dominate material demand due to transparency, durability, and consumer preference for non-reactive food storage solutions.

- Asia-Pacific leads global consumption, supported by rapid urbanization, rising disposable income, and strong manufacturing ecosystems.

- Airtight sealing technology has become a standard feature, driven by consumer demand for extended food shelf life and moisture protection.

- Stackable and modular designs are gaining popularity, particularly in compact urban households with limited storage space.

- E-commerce channels are expanding rapidly, enabling direct-to-consumer kitchenware sales and global brand reach.

- Sustainability trends are reshaping product innovation, encouraging adoption of glass, stainless steel, and bamboo-based materials.

What are the latest trends in the kitchen canisters market?

Shift Toward Modular Kitchen Organization

Modern households increasingly prioritize organized and aesthetically pleasing kitchen environments. Modular kitchen systems are driving strong adoption of coordinated canister sets designed for pantry optimization. Consumers prefer uniform storage solutions that improve accessibility while enhancing visual appeal. Manufacturers are responding by introducing stackable, space-efficient designs compatible with modular cabinetry systems. Transparent labeling, measurement indicators, and interchangeable lids are also becoming common features, allowing households to streamline cooking workflows while maintaining organization standards.

Sustainable and Premium Material Adoption

Environmental awareness is significantly influencing purchasing decisions. Consumers are shifting away from disposable plastic storage toward reusable glass, stainless steel, and bamboo-lid canisters. Premium kitchenware is increasingly positioned as a lifestyle product rather than a purely functional item. Brands are investing in recyclable packaging, BPA-free plastics, and low-carbon manufacturing processes. Sustainability certifications and eco-friendly branding strategies are helping companies attract environmentally conscious buyers, particularly in Europe and North America where regulatory pressure on plastics is increasing.

What are the key drivers in the kitchen canisters market?

Growth of Home Cooking and Pantry Management

The global rise in home cooking has significantly boosted demand for efficient food storage solutions. Consumers preparing meals at home require reliable containers for storing grains, flour, coffee, snacks, and baking ingredients. Kitchen canisters help maintain freshness while supporting bulk purchasing habits, reducing food waste and improving kitchen efficiency. Social media trends focused on pantry organization and meal preparation are further strengthening consumer adoption worldwide.

Urbanization and Compact Living Spaces

Rapid urban development has resulted in smaller residential kitchens, especially in Asia-Pacific and European cities. Space optimization has become essential, encouraging adoption of stackable and modular canisters that maximize vertical storage. Apartment living trends and increasing nuclear households are accelerating demand for compact, multifunctional kitchen storage products.

What are the restraints for the global market?

Price Sensitivity in Emerging Economies

Although premium kitchenware demand is rising, affordability remains a challenge in developing markets. Many consumers continue to rely on low-cost plastic containers rather than higher-priced glass or stainless-steel alternatives. This price sensitivity restricts penetration of premium canister products despite growing awareness of quality storage solutions.

Raw Material Cost Volatility

Fluctuations in prices of glass, polymers, and stainless steel directly impact manufacturing costs. Rising energy and logistics expenses further influence pricing structures, making it challenging for manufacturers to maintain stable margins while remaining competitive in price-sensitive regions.

What are the key opportunities in the kitchen canisters industry?

Smart and Connected Kitchen Storage

The emergence of smart kitchens presents opportunities for technology-integrated canisters featuring inventory tracking, QR labeling, and freshness monitoring. Such innovations align with the broader adoption of connected home ecosystems and appeal to tech-savvy consumers seeking convenience and automation in food management.

Expansion of Direct-to-Consumer Sales Models

E-commerce growth enables manufacturers to bypass traditional retail intermediaries and engage directly with consumers. Subscription-based pantry organization kits and bundled canister sets are emerging as profitable sales strategies. Influencer-led marketing and digital kitchen organization content are also accelerating product discovery and brand differentiation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3150 Million |

| Market Size in 2026 | USD 3370.50 Million |

| Market Size in 2031 | USD 4727.30 Million |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Insights

The kitchen canisters market is segmented by material into glass, stainless steel, ceramic, plastic, and others. Among these, glass kitchen canisters represent the leading material segment, accounting for approximately 38% of the global market share in 2025. The strong market position of glass canisters is primarily driven by increasing consumer preference for hygienic, non-reactive, and visually appealing food storage solutions. Glass offers chemical stability, transparency for easy visibility of contents, resistance to odors and stains, and compatibility with a wide variety of dry food items. Additionally, the growing global focus on sustainability and reduced plastic usage is encouraging consumers to adopt reusable glass storage containers, particularly in developed markets.Glass canisters are widely used for pantry organization as they allow consumers to monitor food quantities while maintaining freshness through airtight sealing mechanisms. The increasing popularity of modular kitchen designs and organized pantry systems further supports the adoption of glass storage solutions.

Stainless steel canisters are gaining traction in both residential and commercial kitchens due to their durability, corrosion resistance, and long service life. These canisters are particularly favored in professional foodservice environments where durability and hygiene standards are critical. Ceramic canisters are increasingly popular in premium kitchen décor segments, offering aesthetic appeal and decorative value alongside functionality.Meanwhile, BPA-free plastic canisters continue to maintain strong demand in price-sensitive markets due to their affordability, lightweight properties, and high impact resistance. Plastic variants are commonly used for bulk storage and in households that prioritize convenience and portability. Ongoing innovations in food-grade plastic materials and improved sealing technologies are further enhancing the performance of plastic canisters.

Application Insights

Based on application, the kitchen canisters market is segmented into dry food storage, snack storage, pantry organization, and other specialized storage applications. Among these, dry food storage remains the largest application segment, contributing nearly 48% of the total market share. The segment's leadership is primarily driven by the widespread need for storing staple pantry items such as flour, rice, sugar, coffee, cereals, pasta, grains, and baking ingredients.The growing global trend toward home cooking, meal preparation, and organized kitchen spaces has significantly increased demand for reliable dry food storage solutions. Kitchen canisters help maintain product freshness, protect ingredients from moisture and pests, and improve pantry management. Airtight lids and stackable designs have become important product features that further enhance their utility.

Snack storage is another growing application segment, supported by increasing consumption of ready-to-eat foods, dried fruits, nuts, biscuits, and packaged snacks. Consumers increasingly rely on canisters to maintain crispness and extend shelf life while maintaining kitchen aesthetics.Multi-purpose pantry applications are expanding steadily as households adopt bulk purchasing behaviors and organized kitchen systems. Additionally, commercial foodservice establishments—including restaurants, cafés, bakeries, and catering services—rely on canisters to maintain ingredient organization, ensure hygiene compliance, and streamline kitchen operations.

Distribution Channel Insights

The kitchen canisters market is distributed through offline retail channels and online platforms. Offline retail channels account for approximately 58% of global sales, maintaining their dominance due to the tactile nature of kitchenware purchases. Consumers often prefer to physically evaluate product quality, sealing mechanisms, durability, and design aesthetics before making a purchase decision.Specialty kitchenware stores, department stores, hypermarkets, and home improvement retailers play a crucial role in product distribution. In-store displays and bundled product sets also encourage impulse purchases and enhance consumer engagement.However, online retail represents the fastest-growing distribution channel. The rapid expansion of e-commerce platforms, increasing smartphone penetration, and improved digital payment infrastructure have significantly boosted online kitchenware sales. Online marketplaces offer consumers greater product variety, competitive pricing, user reviews, and convenient doorstep delivery.Additionally, direct-to-consumer (DTC) brand websites are gaining popularity as manufacturers leverage digital marketing, influencer partnerships, and subscription-based kitchen organization kits to reach modern consumers. Promotional campaigns, customization options, and bundled storage sets are further accelerating online channel growth.

End-Use Insights

The kitchen canisters market is categorized by end use into residential households, commercial foodservice establishments, and institutional kitchens. Residential households dominate demand, contributing nearly 70% of global consumption. This leadership is primarily driven by the growing trend of home cooking, increased awareness of kitchen organization, and rising consumer interest in aesthetically pleasing and functional kitchen storage solutions.Consumers are increasingly investing in modular kitchens and organized pantry systems, which has boosted demand for coordinated canister sets with airtight seals, stackable designs, and transparent containers. Social media influence and home décor trends have also encouraged households to adopt stylish and uniform storage containers.The commercial foodservice sector accounts for approximately 20–22% of market demand. Restaurants, cafés, bakeries, and hospitality establishments rely on durable and hygienic storage solutions to manage ingredients efficiently. Stainless steel and high-capacity plastic canisters are commonly used in these environments due to their durability and ease of maintenance.Institutional kitchens, including those in schools, hospitals, and corporate cafeterias, represent a steadily growing segment. Increasing food safety regulations and hygiene standards are encouraging institutions to implement structured food storage systems, which is supporting demand for standardized kitchen canisters.

Explore more data points, trends and opportunities Download Free Sample Report

Kitchen Canisters Market Segmentations

By Material

- Glass Kitchen Canisters

- Plastic Kitchen Canisters

- Metal Kitchen Canisters

- Ceramic & Stoneware Canisters

- Wood & Bamboo Canisters

- Hybrid Material Canisters

By Closure Type

- Airtight Lock Lid

- Screw-Top Lid

- Clamp Lid / Clip Lock

- Push-Button Vacuum Lid

- Magnetic Seal Lid

- Cork Lid

By Application

- Dry Food Storage

- Snack Storage

- Baking Ingredient Storage

- Spices & Condiments Storage

- Multi-Purpose Kitchen Storage

By End-Use

- Residential / Household

- Commercial Foodservice

- Institutional Kitchens

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Kitchenware Stores

- Department Stores

Regional Insights

Asia-Pacific

Asia-Pacific leads the global kitchen canisters market with approximately 42% share in 2025. The region’s dominance is supported by large population bases, rapid urbanization, and growing disposable incomes in major economies such as China and India. Rising middle-class households and expanding residential construction activity are increasing demand for modern kitchen storage products.China serves as a major manufacturing hub for kitchenware products, offering cost-efficient production and extensive export capabilities. Meanwhile, India’s growing retail sector and increasing penetration of organized kitchenware brands are driving market growth. In developed Asia-Pacific markets such as Japan and South Korea, consumer demand is strongly influenced by premium kitchenware designs, compact storage solutions, and advanced pantry organization systems.Additional growth drivers in the region include the expansion of e-commerce platforms, rising popularity of modular kitchens, and growing awareness of food safety and organized pantry storage.

North America

North America holds around 25% of the global kitchen canisters market share, with the United States representing the largest regional contributor. Consumers in the region prioritize premium kitchen storage products that integrate seamlessly with organized pantry systems and modern kitchen designs.High disposable income levels and strong consumer awareness of food hygiene and sustainability support demand for glass and stainless-steel canisters. The increasing popularity of meal preparation, bulk grocery purchases, and home organization trends further strengthens market demand.Additionally, the strong presence of established kitchenware brands, advanced retail infrastructure, and high e-commerce adoption continue to drive product accessibility and market expansion across the region.

Europe

Europe accounts for nearly 22% of the global kitchen canisters market, with Germany, the United Kingdom, France, and Italy leading regional demand. The market is strongly influenced by strict environmental regulations and increasing consumer preference for sustainable and reusable kitchen products.European consumers often favor eco-friendly materials such as glass and ceramic over single-use plastics. Additionally, the region’s well-established home décor and kitchen design culture encourages investment in aesthetically pleasing and coordinated storage solutions.The expansion of premium kitchenware brands, rising adoption of minimalist kitchen organization trends, and increasing demand for high-quality food storage containers continue to drive growth across the European market.

Latin America

Latin America represents approximately 5% of global demand, with Brazil and Mexico serving as the primary growth markets. Rapid urbanization and the expansion of middle-income households are gradually increasing adoption of modern kitchen storage solutions.The growing influence of international kitchenware brands and the expansion of modern retail formats, including hypermarkets and online marketplaces, are improving product availability. Additionally, rising consumer awareness of food storage hygiene and pantry organization is supporting steady demand growth across the region.

Middle East & Africa

The Middle East & Africa region contributes roughly 6% of global kitchen canisters sales. Market growth is supported by the expansion of the hospitality and tourism sectors, particularly in countries such as the United Arab Emirates and Saudi Arabia.Luxury residential developments and premium kitchenware retail outlets are encouraging demand for high-quality storage solutions in urban households. Additionally, increasing consumer interest in modern kitchen organization and rising disposable incomes in Gulf countries are supporting market expansion.In Africa, gradual improvements in retail infrastructure and growing urban consumer populations are expected to contribute to long-term market development.

Key Players in the Kitchen Canisters Market

- Tupperware Brands Corporation

- Newell Brands (Rubbermaid)

- Lock & Lock Co. Ltd.

- IKEA

- OXO International

- Brabantia

- Anchor Hocking Company

- Libbey Inc.

- Hamilton Housewares

- Corelle Brands

- Meyer Corporation

- World Kitchen LLC

- Zwilling J.A. Henckels

- Joseph Joseph Ltd.

- Felli Group