K-12 Private Education Market Size

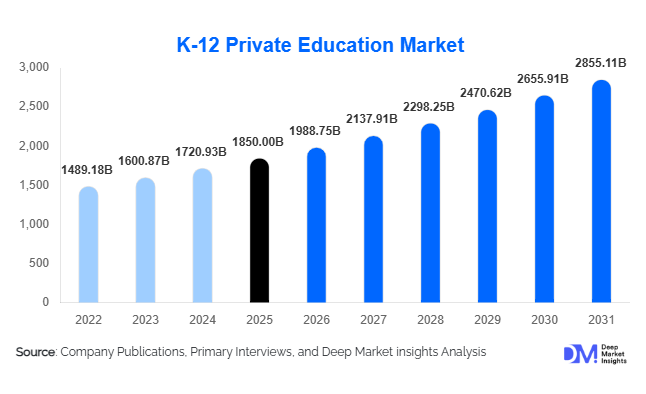

According to Deep Market Insights, the global K-12 private education market size was valued at USD 1,850 billion in 2025 and is projected to grow from USD 1,988.75 billion in 2026 to reach USD 2,855.11 billion by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The K-12 private education market growth is primarily driven by increasing demand for high-quality education, rising middle-class income levels, and the growing preference for international curricula and technology-integrated learning environments.

Key Market Insights

- Urbanization and rising disposable incomes are significantly boosting enrollment in private schools across emerging economies.

- Mid-tier and affordable private schools dominate enrollment volumes, driven by scalability and accessibility.

- Asia-Pacific leads the global market, accounting for nearly 40% of total demand in 2025.

- The Middle East & Africa are the fastest-growing regions, supported by expatriate demand and policy support.

- Digital and blended learning models are transforming traditional education delivery systems.

- International curricula adoption is rising, particularly among premium private schools globally.

What are the latest trends in the K-12 private education market?

Blended and Digital Learning Integration

Private schools are increasingly adopting hybrid learning models that combine traditional classroom teaching with digital tools. Learning management systems, AI-based assessments, and personalized learning platforms are becoming standard across institutions. This trend gained momentum post-pandemic and continues to reshape how education is delivered, improving student engagement and academic outcomes. Schools are investing in smart classrooms, cloud-based content delivery, and real-time performance analytics, creating a more adaptive and data-driven learning environment.

Rising Demand for International Curricula

There is a growing preference for globally recognized curricula such as IB, Cambridge, and American systems, particularly among affluent families. These programs provide global mobility, critical thinking skills, and international exposure. As a result, private schools offering international education are expanding rapidly across Asia-Pacific, the Middle East, and parts of Africa. Partnerships with global accreditation bodies and foreign institutions are further strengthening this trend.

What are the key drivers in the K-12 private education market?

Increasing Demand for Quality Education

One of the primary drivers is the rising dissatisfaction with public education systems in many regions. Issues such as overcrowding, outdated infrastructure, and limited teacher availability are pushing parents toward private schools. These institutions offer better student-teacher ratios, advanced facilities, and enhanced extracurricular opportunities, making them a preferred choice for quality education.

Growth of Middle-Class Population

The expansion of the global middle class, particularly in emerging economies such as India, China, and Brazil, is driving private school enrollment. Families are increasingly willing to invest in education as a long-term asset, allocating a significant portion of household income toward tuition fees and related expenses.

Technological Advancements in Education

Rapid technological adoption is another key growth driver. Private schools are leveraging digital tools such as AI-based tutoring, virtual classrooms, and gamified learning platforms to enhance teaching efficiency. This integration not only improves academic outcomes but also attracts tech-savvy students and parents.

What are the restraints for the global market?

High Tuition Costs and Affordability Issues

Premium private education remains expensive, limiting access for lower-income households. High tuition fees, additional costs for extracurricular activities, and infrastructure expenses restrict market penetration in developing regions.

Regulatory and Policy Constraints

Government regulations related to fee structures, land acquisition, and curriculum standards pose challenges for private school operators. Policy uncertainty and compliance requirements can slow expansion and reduce profitability in certain markets.

What are the key opportunities in the K-12 private education industry?

Expansion of Affordable Private Schools

Emerging markets present significant opportunities for low-cost private education models. Scalable school formats with standardized teaching methods can deliver quality education at lower costs, enabling operators to tap into large underserved populations while maintaining profitability.

EdTech Integration and Digital Services

The integration of EdTech solutions into traditional schooling models offers new revenue streams and operational efficiencies. Subscription-based digital platforms, online tutoring services, and AI-driven learning tools are creating opportunities for both existing players and new entrants.

Global Expansion of International Schools

The rising demand for international curricula is encouraging private school operators to expand globally. Regions such as the Middle East and Southeast Asia offer strong growth potential due to expatriate populations and increasing demand for globally recognized education systems.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1850 Billion |

| Market Size in 2026 | USD 1988.75 Billion |

| Market Size in 2031 | USD 2855.11 Billion |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Education Level Insights

Primary education (Grades 1–5) dominates the K-12 private education market, accounting for approximately 32% of the global share in 2025. This segment continues to lead due to the universal nature of early-stage education and strong enforcement of compulsory schooling policies across most countries. Parents globally prioritize foundational learning years, driving consistent enrollment in private primary schools. Additionally, private institutions at this level often emphasize smaller class sizes, personalized attention, and early skill development (such as language proficiency and digital literacy), which further strengthens demand. The scalability of primary education infrastructure and standardized curriculum delivery also enables operators to expand rapidly, making it a highly attractive and stable revenue-generating segment.

Curriculum Type Insights

National curriculum schools hold the largest share at around 65%, primarily driven by their affordability, regulatory alignment, and widespread acceptance among the general population. These schools cater to the majority of students by offering cost-effective education aligned with local government standards and entrance examination systems. The dominance of this segment is further supported by policy frameworks that favor national curricula in public examinations and higher education pathways. However, international curricula are witnessing accelerated growth, particularly in urban and high-income segments, due to their global recognition, emphasis on critical thinking, and pathways to international universities. The increasing mobility of families and rising aspirations for global careers are key drivers behind this shift toward international education.

School Type Insights

Day schools dominate the market with nearly 70% market share, largely due to their cost efficiency, accessibility, and operational scalability. These institutions cater to the majority of urban and semi-urban populations, where daily commuting is feasible and preferred. The lower infrastructure and operational costs compared to boarding schools allow operators to expand quickly and maintain competitive pricing. Additionally, cultural preferences in many regions favor day schooling, where families remain actively involved in students’ daily lives. Boarding schools, although representing a smaller share, are growing steadily in premium segments, particularly for international students and families seeking immersive academic environments, contributing to higher per-student revenue.

Fee Structure Insights

Mid-tier schools account for approximately 45% of the market, making them the largest segment globally. This segment’s leadership is driven by its ability to balance affordability with quality education, making it highly appealing to the expanding middle-class population. Mid-tier schools typically offer modern infrastructure, qualified faculty, and extracurricular activities at moderate fee levels, positioning them as a preferred choice for value-conscious parents. The rapid growth of urban middle-income households, especially in Asia-Pacific and Latin America, continues to fuel demand for this segment. Additionally, operators in this category benefit from high enrollment volumes, enabling economies of scale and stable profit margins.

Delivery Mode Insights

Traditional offline education continues to dominate with over 80% share, as physical classrooms remain the preferred mode for structured learning, social interaction, and holistic development. The dominance of this segment is reinforced by parental trust in conventional schooling systems and regulatory frameworks that mandate physical attendance in many countries. However, blended learning models are emerging as a significant growth driver, integrating digital tools with classroom teaching. The adoption of smart classrooms, AI-based learning platforms, and online assessments is enhancing the overall learning experience. This hybrid approach is particularly gaining traction in developed markets and urban centers, where digital infrastructure is well established and demand for personalized learning is increasing.

End-Use Insights

Household spending remains the primary end-use driver of the K-12 private education market, supported by rising disposable incomes and increasing awareness of the long-term value of quality education. Parents are allocating a larger share of their income toward education, viewing it as a critical investment in future career opportunities. The fastest-growing segment is affordable private education in emerging economies, with growth rates exceeding 9% CAGR, driven by large underserved populations and gaps in public education systems. Additionally, corporate-sponsored schools are gaining traction as part of employee welfare and CSR initiatives, particularly in industrial hubs. International student demand is also expanding, especially in regions such as the Middle East and Southeast Asia, where expatriate populations seek globally recognized education systems.

Explore more data points, trends and opportunities Download Free Sample Report

K-12 Private Education Market Segmentations

By Education Level

- Pre-Primary Education

- Primary Education

- Middle School Education

- Secondary Education

- Senior Secondary Education

By Curriculum Type

- National Curriculum

- International Curriculum

- Hybrid/Integrated Curriculum

By School Type

- Day Schools

- Boarding Schools

- Day-Boarding Schools

By Fee Structure

- Premium Schools

- Mid-Tier Schools

- Affordable/Low-Cost Private Schools

By Delivery Mode

- Traditional Offline Schools

- Blended Learning Schools

- Fully Online Private Schools

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with approximately 40% share in 2025, making it the largest and most dynamic region. Countries such as India and China dominate regional demand due to their large school-age populations and rapid expansion of private education infrastructure. India alone contributes nearly 15% of global demand, driven by increasing urbanization, rising middle-class income, and strong parental preference for English-medium education. In China, demand is fueled by premium private schools and international curricula adoption. Key growth drivers in the region include population growth, government limitations in public school capacity, rising disposable incomes, and strong emphasis on academic achievement. Additionally, increasing investments in EdTech and private school chains are accelerating market expansion.

North America

North America holds around 25% market share, with the United States being the primary contributor. The region is characterized by a mature private education system, with demand concentrated in premium schools, religious institutions, and specialized learning environments. Key growth drivers include high household income levels, strong demand for personalized and experiential education, and widespread adoption of advanced educational technologies. The presence of well-established private school networks and increasing focus on STEM education, arts, and extracurricular excellence further support market growth. Additionally, demand for alternative education models such as charter-like private institutions and hybrid learning schools is expanding.

Europe

Europe accounts for approximately 20% of the market, with major contributions from the UK, Germany, and France. The region’s growth is driven by increasing demand for international curricula, bilingual education, and specialized private schooling. In the UK, private education is well established, with strong demand for premium institutions. Germany and France are witnessing growth in international schools due to expatriate populations and globalization. Key drivers include rising cross-border mobility, government support for educational diversity, and growing preference for multilingual education. Additionally, European parents increasingly value holistic development, which private schools are well-positioned to provide.

Middle East & Africa

The Middle East & Africa region is the fastest-growing, with a CAGR exceeding 9%. Countries such as the UAE and Saudi Arabia are key markets, driven by large expatriate populations and strong demand for international curricula. In Africa, countries like Nigeria and Kenya are witnessing rapid growth in affordable private schooling due to gaps in public education systems. Key drivers include government encouragement of private sector participation, population growth, and increasing awareness of quality education. In the Middle East, high-income households and demand for premium international schools are major growth contributors, along with strong foreign investments in education infrastructure.

Latin America

Latin America holds around 10% share, with Brazil and Mexico leading demand. The region’s growth is primarily driven by urbanization, rising middle-class income, and increasing dissatisfaction with public education quality. Private schools are expanding rapidly in urban areas to meet growing demand for better academic outcomes and infrastructure. Key drivers include demographic growth, economic development, and increased private sector participation in education. Additionally, governments in several countries are supporting private education through policy reforms and partnerships, further boosting market expansion.

Key Players in the K-12 Private Education Market

- Nord Anglia Education

- GEMS Education

- Cognita Schools

- Inspired Education Group

- Bright Scholar Education

- Maple Leaf Educational Systems

- SEK Education Group

- Orbital Education

- SABIS Network

- Ryan International Group

- Delhi Public School Society

- Aditya Birla Education Trust

- Global Schools Foundation

- Taaleem

- Charterhouse Group